DELL (Trans): Demand outpaces supply; biz. pipeline several times backlog

Below is Dolphin Research’s transcript from DELL FY27 Q1 earnings call. For the earnings read-through, see 'Dell: AI Surging, Legacy Warming, Old Timer 'Fully Amped''.

I. Dell Technologies DELL key takeaways

1. Shareholder returns: Returned $2.1bn in Q1 via buybacks and dividends. Repurchased 11mn shares at an Avg. price of $147 and paid a dividend of Approx. $0.63 per share. Management reiterated the existing capital return framework and expects to keep buybacks robust.

2. Q2 guide: Revenue of $44–45bn, ~50% YoY at the midpoint. ISG up ~75% (AI server revenue $15.5bn), CSG up ~20%. OpEx down QoQ by low-single digits, operating profit up ~80%. ISG OPM to improve QoQ, CSG OPM to normalize to ~6%. Diluted share count ~652mn, non-GAAP diluted EPS at $4.80 ± $0.10, implying >100% YoY at the midpoint.

3. FY27 guide (materially raised vs. 90 days ago): Revenue of $165–169bn, nearly +50% YoY at the midpoint. ISG up ~80% (AI server revenue midpoint $60bn, ~2.4x last year), legacy servers up slightly over 60%, storage up mid-single digits, CSG up low teens. OpEx up high-single digits YoY (mainly performance comp), but OpEx/revenue to single digits. Operating profit up >55%; I&O $1.4–1.5bn. Non-GAAP diluted EPS guided to $17.90 ± $0.25, ~+75% YoY at midpoint. Company lifted FY27 revenue and EPS guides by Approx. $27bn and $5, respectively.

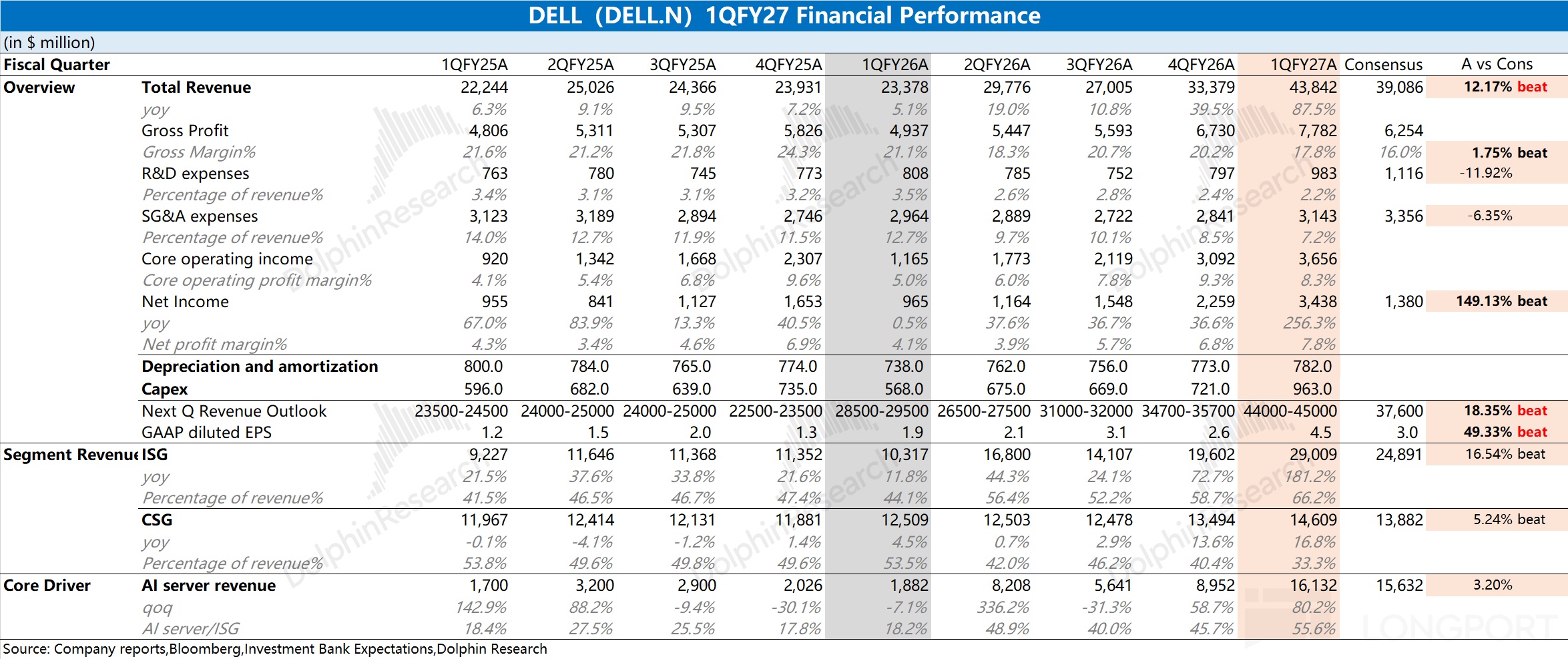

4. Key financials: Q1 revenue $43.8bn (+88%), GP $7.9bn (+57%), GPM 18.1%. Mix headwind from AI servers; excluding AI mix, GPM rose YoY. OpEx $3.7bn (+9%), OpEx/revenue at 8.4% (lowest since 2020). Operating profit $4.2bn (+154%), OPM 9.7%; net income $3.2bn (+194%); EPS $4.86 (+214%), a record. OCF $4.1bn (Q1 record), cash and investments $14.1bn (+$0.8bn QoQ), core leverage 1.2x.

5. AI metrics: Q1 AI orders of $24.4bn, AI server revenue of $16.1bn, record AI backlog of $51.3bn. AI server OPM remains in the mid-single-digit target range. Full-year AI revenue guided to $60bn (vs. prior $50bn), with management expecting to enter next FY with a 'meaningful backlog'.

II. Detailed call notes

2.1 Management remarks

1. AI server biz.

a. Q1 AI orders were $24.4bn; AI server revenue $16.1bn; AI backlog a record $51.3bn. Customer count topped 5,000 (+50% over 6 months), spanning neocloud, sovereigns and enterprises.

b. AI opportunity is exceptionally strong, broad-based and durable. Pipeline continued to expand QoQ and remains several times the backlog. Demand still outstrips supply, with DRAM/NAND the key bottlenecks, and we expect to enter next year with meaningful backlog.

c. Announced new infrastructure at GTC on NVIDIA Vera Rubin rack-scale platform, the Rubin GPU architecture and RTX GPUs. Launched the first OEM desktop workstation with GB300, Dell Pro MAX. Unveiled deskside genic AI solutions at Dell Technologies World to run production-grade AI locally for coding, research and private-assistant use cases.

d. Rolled out Dell Power Rack, a one-stop, factory-integrated rack-scale solution; Dell leads in rack-scale infrastructure. The AI factory ecosystem keeps expanding with partners such as NVIDIA, Google Cloud, OpenAI, SpaceX AI, ServiceNow, Palantir, Mistral, CrowdStrike. Worked with Google Distributed Cloud to bring Gemini models on-prem for data residency and sovereignty.

e. Customers are buying integrated, production-ready, controllable stacks with performance/security/data foundations, not mere components. Dell’s engineering, large-scale deployment, services/support and flexible financing are the core differentiators.

2. Legacy servers & networking

a. Revenue $8.5bn, +92% YoY. Strength was broad-based across regions, and demand materially exceeded supply.

b. Large enterprises led the upcycle, refreshing compute and expanding capacity for workload growth. Customers prioritized availability to drive modernization and growth.

c. Customers increasingly care about infrastructure density, seeking optimization within existing DC footprints via higher compute density/efficiency/integration (the new 18G servers enable 13:1 consolidation).

d. Legacy servers are seeing incremental demand from AI inference workloads. Installed base remains largely 14G or older, leaving ample upgrade runway.

e. Memory supply uncertainty is pushing customers to lock in infrastructure across legacy/AI workloads for longer terms. The company continues Q4’s pricing and margin discipline.

3. Storage

a. Revenue $4.3bn, +8% YoY. Dell IP storage outperformed the market for the 5th straight quarter and posted a record demand growth quarter.

b. In primary storage, PowerMax and PowerStore outperformed; PowerStore has delivered double-digit demand growth for 8 consecutive quarters. Unstructured storage (PowerScale, ObjectScale) grew for 3 straight quarters, double digits in the last two.

c. PowerStore Elite offers up to 3x performance/density vs. prior gen with a 6:1 data reduction guarantee, leading the industry. ObjectScale improved object storage density. PowerFlex introduced a unified block/file/object exascale architecture.

d. Dell IP storage carries higher margins and is gaining mix, lifting ISG profitability. Lightning, a parallel file system for AI, achieved NVIDIA full-stack certification.

4. CSG (PC)

a. Revenue $14.6bn (+17%), with share gains for the 2nd straight quarter. Commercial $13.0bn (+18%, up for 7 straight quarters; demand up for 9), consumer $1.6bn (+9%, demand up for 3; gaming PCs strong).

b. Large enterprises drove double-digit growth across regions. About one-third of the installed base is 4+ years old, leaving refresh upside.

c. The company used the Windows 11 window to catch up prior delays. CSG OP was $1.2bn (8% OPM), helped by scale, higher peripherals/services attach and improved consumer profitability.

d. AI is extending to deskside: Dell Pro MAX with GB10/GB300 brings the AI factory to deskside. GenTech workloads are moving to the edge, lifting the performance premium of PCs.

5. Operating model & strategy

a. The model proved resilient amid tight supply/inflation as customers favored Dell as a 'reliable supplier' across PCs, servers and storage.

b. Modernization (simplify, standardize, automate, AI-augmented ops) drove operating leverage. Full-year OpEx/revenue will remain in single digits.

c. The company expects ongoing tightness in DRAM, NAND, CPUs and HDDs, with repricing 'almost daily'. Mature-node utilization is rising, while advanced nodes are fully allocated with lead times up to 1 year.

2.2 Q&A

Q: Results far beat. How much was price and restocking pull-forward by segment, and why raise 2H guidance?

A: (Jeff) Today’s demand is structurally different and multi-factor. First, there is pull-forward as customers fear price hikes and pre-order to lock supply. Second, the installed base is massive: on PCs, ~1/3 devices are 4+ years and Windows 11 catch-up helped this quarter; on servers, a large 14G base is ready to upgrade. Third, edge and infrastructure upgrades are accelerating, with 18G servers a great vehicle (13:1 consolidation). Fourth, brand-new AI demand is creating markets we have never seen for legacy servers via training drag, inference and agentic AI. Fifth, Dell is gaining share across PCs, servers, storage and AI servers. Finally, customers pick Dell as a stable partner amid supply noise. The forward pipeline is healthier and faster-growing than history, giving confidence to raise FY revenue by ~$27bn.

Q: Legacy server outperformance — volume vs. price mix, and can momentum last beyond 1–2 quarters into next year?

A: (Jeff) On PCs, both consumer and commercial units rose last quarter with share gains. Inflation supported higher pricing, especially at the premium end, and Dell leads premium where price tailwinds widen our advantage. Peripherals/services attach is very healthy and scales with base growth, driving more revenue per unit.

On servers, absolute units grew sharply; per-box configs rose YoY — more cores, DRAM and NAND per server — and component inflation lifted ASPs. Modernization/consolidation is another upgrade driver. AI drag is key too — inference and agentic workloads are moving to legacy servers, especially high-density into neocloud and top-end enterprises (e.g., semi and big tech).

Q: Despite a higher 2H guide, you remain 'appropriately cautious.' 2H is ~48% of FY (vs. ~52% historical). Is this pull-forward or conservatism tied to components?

A: (Jeff) This is a supply issue, not a demand issue. We will be supply-constrained in 2H. (David) Demand exceeds supply broadly — beyond GPUs, also CPU-side AI, legacy servers and PCs. Designs are complex, and supply chain, sales and product teams will keep optimizing supply vs. demand formation. We will chase more supply into 2H with a healthy pipeline.

Q: With customers prioritizing supply all year, how volatile are IT budgets? Any pull-ahead from next year? And will agentic AI on legacy servers drive real Tier-2 CSP demand?

A: (Jeff) I can’t speak to next year’s budgets, but we see longer-term dialogues — 3–5 years — on locking supply to support growth and infra upgrades. The focus is supply access, as we can’t guarantee tomorrow’s price. Pipeline shows this trend persists, and unusually, both in-quarter and next-2-quarter pipelines are growing faster than history as more customers want tech earlier. We see budget expansion and reallocation, but it’s only one quarter in, so we remain prudent on 2H.

(David) Because demand exceeds supply, we expect to enter next FY with meaningful backlog. DFS financing is another advantage, with even typically non-financed customers using our capacity to deploy more quickly under budget limits. Origination grew double digits in CSG, legacy servers, storage and AI.

Q: AI servers guide raised to $60bn. Where does the extra $10bn come from, and what’s your server ODM capacity ceiling?

A: (David) A strong start — Q1 shipments of $16.1bn, orders $24.4bn, backlog $51.3bn — let us raise the full-year by $10bn after just 90 days. These are complex designs as we prep for Vera Rubin transitions and coordinate DC readiness and intake with customers. Coverage is broad — neocloud, sovereigns and enterprises are all expanding, with 5,000 customers up >50% in 6 months. We have high conviction in the 5-quarter pipeline, the pipeline is multiples of backlog and growing across every vertical (neocloud/sovereign/enterprise) and region. (Jeff) No capacity ceiling on system build; the constraint is components.

Q: You said FY GPM outlook is better vs. 90 days ago. Is it pricing, product mix, or customer mix?

A: (David) Start with Dell IP storage. We raised Q2 and 2H revenue, and the IP mix (unstructured and midrange PowerStore) is resonating and lifting margins. On CSG and legacy servers, we committed to hold margins and see a path to do so while growing. All-in, this supports higher consolidated margins.

Q: With 5,000 AI server customers, how are storage/services attach rates trending? Is Dell IP storage strength tied to AI attach? Do you still target mid-single-digit OPM for AI servers?

A: (Jeff) We are selling more storage and services to AI customers. At DTW, Michael showcased our unstructured data solutions winning marquee accounts, signaling a shift in market recognition. Across neocloud, sovereigns, HFTs, big tech and semis, we sold more storage — exclusively Dell IP storage. Unstructured had a record demand quarter because unstructured data is AI’s 'feed'. This is our fastest-growing area. The whole portfolio has momentum — Dell IP up 5 straight quarters, PowerMax 5, PowerStore 9, PowerScale 4, ObjectScale 3, and data protection 2. Competitiveness is meaningfully better, with many products built for AI — e.g., Lightning, a parallel file system for the AI era with NVIDIA full-stack certification, and deep joint engineering on data ingest/management.

Architecture matters more than ever. PowerStore Elite is 3x faster with 1.5M IOPS and 6:1 reduction — buy 1PB raw to store 6PB effective, with 70% faster REIT and 4x throughput. Exascale storage targets these customers; rack-scale integrates storage/network/compute for higher performance. In data protection, 75:1 compression again proves the architecture point. Our core architecture can store the same data with fewer servers and SSDs. We package this for all segments, especially AI (sovereign/neocloud/enterprise). We are not declaring victory, but we are optimistic — DTW’s storage payload was our largest ever, with more to come. R&D uses AI internally to deliver a larger portfolio faster, with storage at the forefront. Services deployment, operations and availability advantages are also resonating, and we will keep investing across customer segments.

Q: Relative to the Oct Analyst Day LT targets (7%–9% revenue, 15%+ EPS CAGR), how do agentic AI use cases and share gains change your LT view?

A: (David) We won’t redo a 5-year plan on a Q1 call. What we see is real, durable, accelerating, broad-based growth (beyond GPUs), supporting our decision to raise Q2 (essentially a mirror of Q1) and lift every business (PC, servers, storage, AI) into 2H. We usually have high conviction on 2–2.5 quarters of pipeline, and for AI, the next 5 quarters of pipeline are multiples of backlog. All signs point to broader demand. Our goal remains to exit the year with meaningful backlog.

(Jeff) Historical models no longer fit. The question is: what is the value of embedding intelligence in every workflow, decision, product and customer interaction? It is very high. That’s the agentic shift since Oct — the 3 CPU leaders all talk about CPU TAM expansion driven by agentic. Agents move AI from 'advisor' to 'operator'. The 'harness' that supports agents — I/O, branching, retries, state — is sequential and CPU-led. CPUs run the harness, manage memory and sit in every agent loop — a new market we didn’t grasp in Oct, driven by embedding intelligence in knowledge work. We are early.

Another way to say it: compute premiums — edge PCs/phones, harness servers, and GPUs doing the 'magic' — are rising at unprecedented speed and lifting the ecosystem. All of this requires storage, with high-performance storage to log agent actions for audit/remediation. I couldn’t have forecast that in Oct. I still can’t size TAM today, but it is bigger, growing and early.

Q: CSG OPM hit one of the best in PCs (8%). What drove it — pricing, low-cost inventory, or other? Will PC margins revert to Investor Day range or move higher?

A: (Jeff) Scale led the quarter — OpEx/revenue down ~600bps YoY and ~300bps QoQ, a strong lever for PCs. In Q4 we delayed pricing actions to drive volume and gained share; in Q1 we pulled pricing forward to prep for Q2 cost up, which in hindsight may have been 'a bit early'. That tempered transactional demand (consumer/SMB), reflected in our new PC OP guidance. Beyond scale, TRU (component cost uplift) helped, and peripherals/services attach also supported profits. We are not at COVID-era highs; COVID PC margins were similar or even slightly better. We keep pricing discipline, seeking the optimal balance in transactional segments, while large deals are one-by-one priced. The cadence isn’t perfect, but we are optimistic.

Q: Legacy servers guided +60% for the year, storage mid-single digits — can storage have a longer tail? If prices rise again in coming months, will pass-through get harder?

A: (David) 2H guidance is still capped by supply we can secure; demand is ample, and the demand> supply setup spans ISG. Also, the bridge from third-party storage to Dell IP is still in motion and largely completes by year-end. From there, storage can grow more consistently off a higher base, to our P&L’s benefit.

(Jeff) On pricing — we are repricing almost daily, and customers feel pressure. But in the near term nothing changes — fuel, raws, DRAM, NAND, CPUs are inflating at a rare pace. Some customers pause and wait, which we do see; others accelerate multi-year supply agreements, expecting tighter markets later.

Q: Beyond memory, what else constrains supply? Are PCBs a cap?

A: (Jeff) The big three are NAND, DRAM and CPUs; then HDDs; and many others after that. Mature-node fab utilization is climbing fast, advanced-node capacity is fully allocated with ~1-year lead times. Pressure is broad, but the heaviest remains DRAM, NAND, CPUs, then HDDs and surrounding components. Our supply chain teams have worked these issues for years — we do not stock out. Sales demand and pipeline are inspiring, and teams are digging out more supply — every bit and every processor matters.

Q: In legacy servers, what is x86 vs. ARM mix and margin delta between them?

A: (Jeff) Legacy servers today are x86; we are excited about NVIDIA Vera because advanced workloads (CPU scaffolding around each GPU call) need stronger CPU performance, creating more choice and opportunity, so we need more CPU supply. On GPU servers, the mix tilts to ARM — GB200, GB300 and future Vera are ARM-heavy in large DLC deployments, while enterprise air-cooled (B200, B300, RTX-6000 Pro) are mostly x86.

<End>

Risk disclosure and statements:Dolphin Research disclaimer and general disclosures