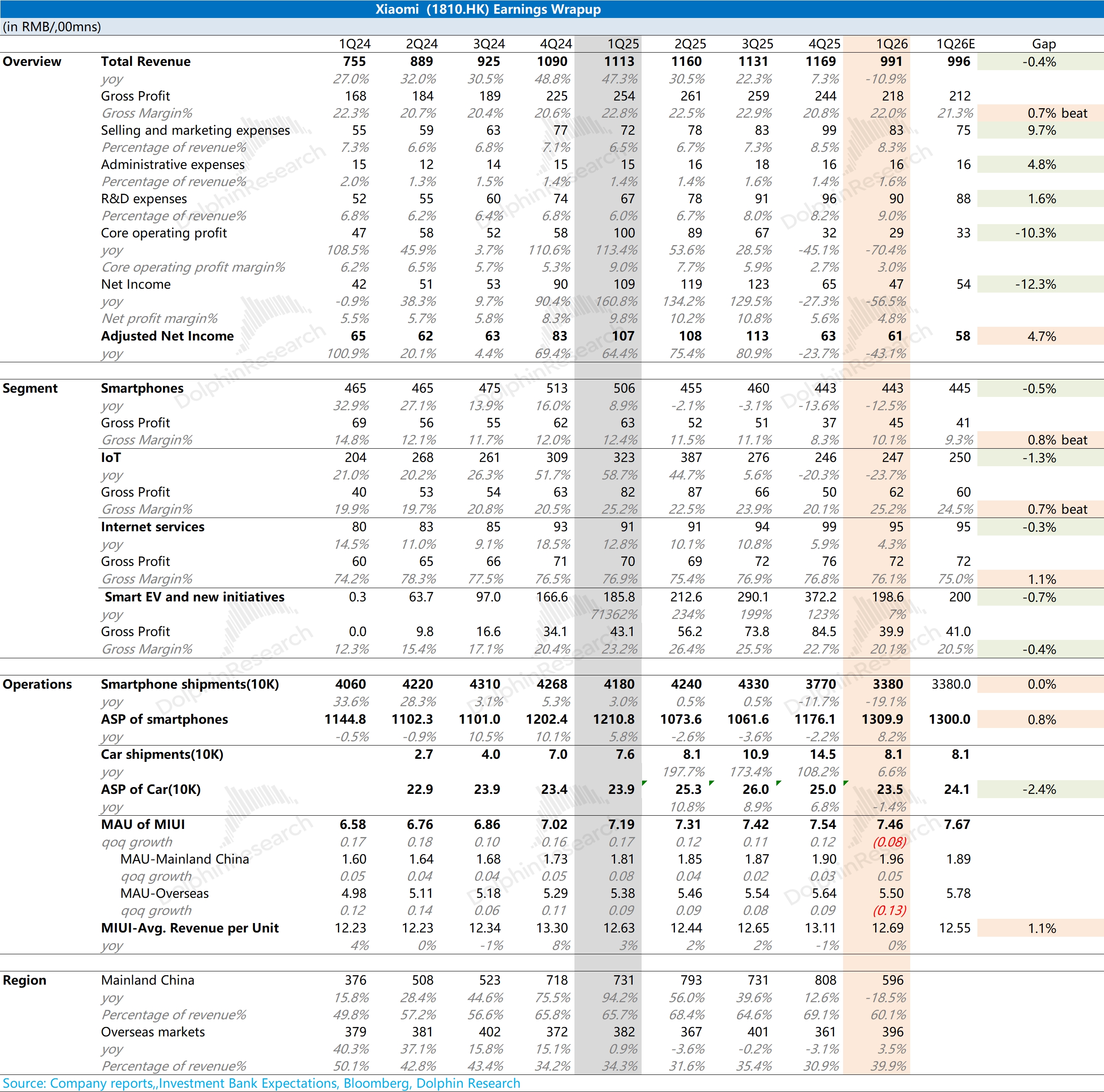

Xiaomi 1Q26 First Take: Results were broadly in line with market expectations. The YoY revenue decline was driven mainly by legacy segments, namely smartphones and IoT.

Data this quarter indicate Xiaomi still faces meaningful operating pressure. Smartphones and IoT posted double-digit YoY declines, and the auto biz saw a clear slowdown in growth and GPM.

From a share-price lens, the drop from HK$60 to around HK$30 has largely priced in memory shortages, weak smartphones, and cooling sentiment on Xiaomi Auto. From this print, the focus should be on what held up better.

① Smartphones and IoT saw a notable QoQ rebound in GPM. The improvement was clear this quarter.

② The decline in auto ASP and GPM this quarter was mainly a one-off effect from purchase-tax subsidies. Dolphin Research believes memory shortages persist, but Xiaomi prioritized allocation to higher-ASP products, stabilizing margins on legacy hardware. Once the YU7 order pool is digested, the subsidy-driven erosion of ASP and GPM should abate.

Overall, Xiaomi still faces memory-related constraints, and legacy segments are unlikely to shine near term, but hardware GPM has held. The main swing factor is autos: management previously guided for 550k units for the full year (~+33% YoY). Relying on the current YU7 and SU7 alone makes that target challenging, so stronger new launches will be needed. More to come in Dolphin Research's follow-up take and Trans. $XIAOMI-W(01810.HK) $Xiaomi Corporation(XIACY.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.