The three major cloud giants are all releasing their earnings reports today

Just to give the market a bit of an AI shock💪

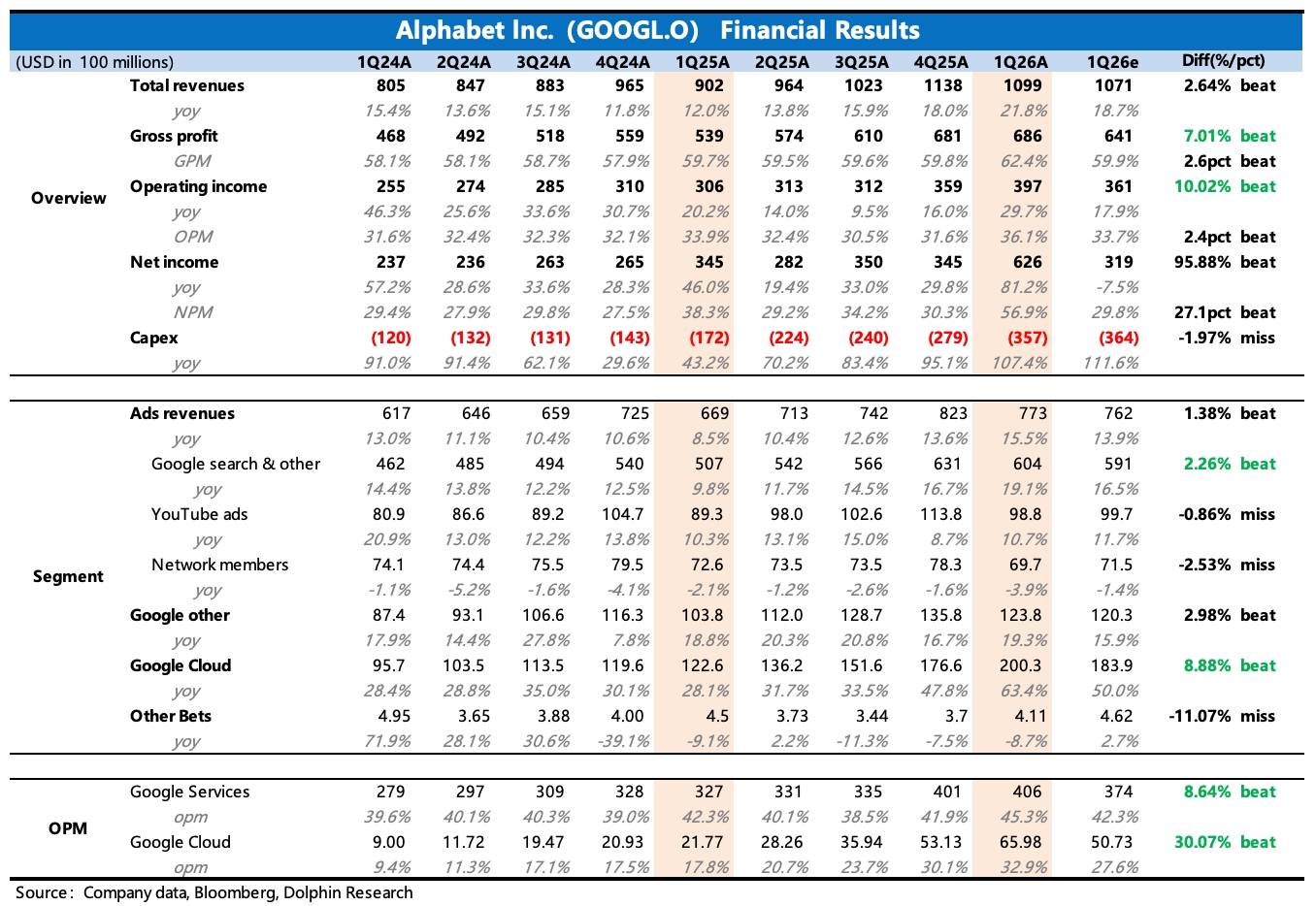

Alphabet 1Q26 First Take: most headline metrics beat, with the exception of muted YouTube ads and continued pressure in Network ads. The standout was Cloud, which not only met buy-side revenue expectations and beat on margins, but also delivered an extraordinary surge in backlog. Backlog nearly doubled QoQ, underscoring surging enterprise AI demand and Alphabet’s full-stack advantage.

1) Cloud blew out again: segment revenue reached 20bn (+63%), a small upside vs. more bullish buy-side views (~+60%) and well ahead of peers. Backlog rose to 462bn vs. 240bn at year-end, nearly doubling QoQ, driven largely by cloud contracts with a smaller portion from direct TPU hardware sales for customer-built data centers. Net adds of 220bn were likely led by Anthropic and Meta, with multiple billion-dollar new wins.

A deep order book, the newly launched 8th-gen TPU, and a more complete AI infrastructure stack de-risk high growth for at least 1–2 years. Roughly half of the backlog is expected to be recognized as revenue within two years.

Quality is high as well: Cloud OPM improved to 33%, ahead of market expectations. Beyond confirming current AI supply shortages, this reflects cost advantages from Alphabet’s full-stack tech chain. It also shows the shift from selling compute to selling solutions is expanding monetization on the enterprise AI side.

Management highlighted strong Q1 momentum for Gemini Enterprise launched in Q4. Monthly active paying users rose 40% QoQ. Token throughput via direct customer API calls jumped from 10bn per minute at year-end to 16bn.

2) Search remained solid: revenue grew 19%. Even allowing for up to ~200bps of FX tailwind, there was no QoQ slowdown vs. last quarter. This suggests limited near-term AI cannibalization, with AI still lifting search volumes and conversion, and also reflects a firm U.S. macro backdrop and Olympic-driven brand marketing in Q1.

3) YouTube ads are recovering slowly: ad revenue missed consensus again, consistent with an adjustment phase as Shorts is integrated into the long-form ecosystem amid industry transition. Competition in long-form instream ads has intensified as Netflix, Disney and Amazon Prime push ad-supported tiers. Shorts, facing stronger short-video rivals like Reels and TikTok, is helping fill the near-term gap left by slower long-form growth.

4) Other paid subscriptions rebounded: Other revenue grew 19%, moving past last quarter’s Pixel cycle noise. Management said YouTube and Google One drove total subscriptions to 350mn, with a net add of 25mn QoQ.

5) Capex guide unchanged: management kept 2026 Capex at 175–185bn, implying a YoY double. Q1 Capex was 35.7bn (+107% YoY), slightly below the 36.4bn consensus.

6) Margin tailwind window: Q1 OPM climbed to 36%, up 200bps YoY, driven by GPM expansion, while the OpEx ratio ticked up ~50bps YoY.

In the near term, AI demand is already materializing and quickly becoming a more important growth driver. At the same time, Capex that re-accelerated in 2H last year and is set to double this year will flow into depreciation quarter by quarter. Given today’s tight supply-demand balance, this creates a short-term window for margin expansion.

Conversely, from 2H onward, heavy investment will start to weigh on further margin improvement. Unless the current upcycle and supply-demand gap extend, giving cloud providers more pricing power, the drag will become more visible.

7) Buybacks paused, dividend slightly higher: to preserve cash for flexible deployment amid heavy investment (including internal and external), buybacks were paused in Q1 and the company issued debt. The dividend was raised by 5% YoY starting this year, but the yield remains minimal. $Alphabet(GOOGL.US) $Alphabet - C(GOOG.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.