Guming (Trans): Dine-in mix is back to a relatively healthy level

Dolphin Research's notes from Guming's 2H25 earnings call are summarized below. For our earnings take, see Guming: As state subsidies faded, the 'Costco of tea drinks' stays solid.$GUMING(01364.HK)

I. Key takeaways

1. Shareholder returns: Proposed final dividend of HK$0.5 per share, payable in two tranches (HK$0.25 in Aug and HK$0.25 in Dec). After deducting major CapEx and withholding tax, the effective payout is about 40%, in line with the IPO pledge to pay at least 50% of profit after major CapEx.

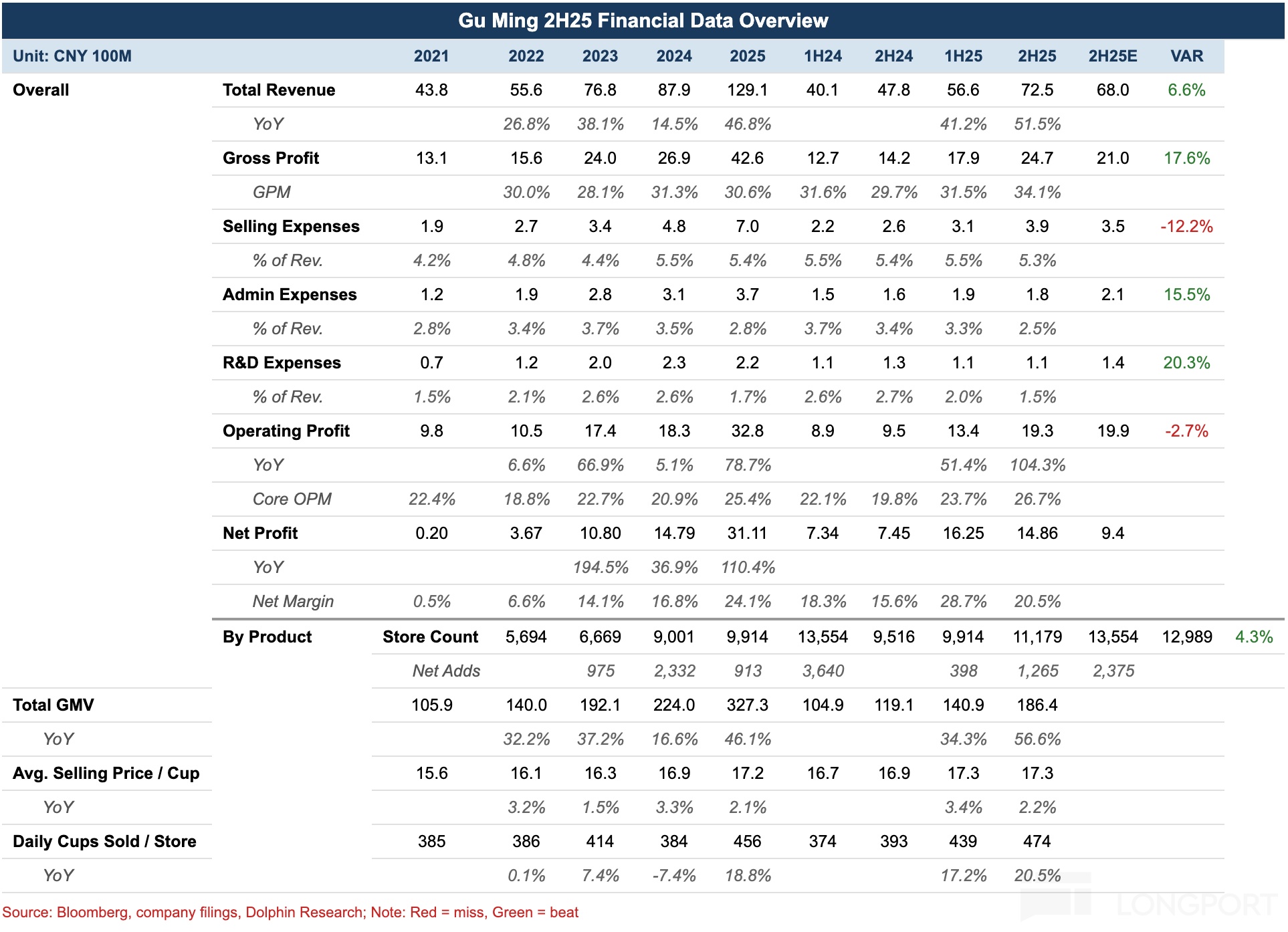

2. GPM: FY25 GPM improved by approx. 250bps vs. FY24. FY24 saw one-offs that dragged margins, which recovered in FY25; H1 was weighed by lower-margin coffee beans and machines, with less drag in H2. Into FY26, GPM should edge up but not swing widely, with FY25 as a reasonable benchmark.

3. Balance sheet: Restricted cash rose to around RMB 6bn, matched by interest-bearing bank loans, driven by an offshore HKD loan + USD time deposit carry (capturing FX and rate spreads). The position is expected to unwind upon maturity in Jun 2026.

4. CapEx: In FY25 the company purchased a land parcel in Xiaoshan, Hangzhou (~RMB 400mn) to build its HQ. Routine maintenance CapEx is about RMB 100mn per year, HQ construction c.RMB 200mn per year, and the asset-light model remains unchanged.

II. Details from the earnings call

2.1 Management remarks

1. GMV and store footprint

a. FY25 GMV reached RMB 32.7bn on a delivery-fee-inclusive basis, consistent with the IPO definition. In the backdrop of delivery-platform promotions, growth including delivery fees diverged from underlying merchandise GMV growth.

b. Average daily GMV per store rose 21% YoY, outpacing merchandise-only GMV, and management flagged the definitional gap. c. Year-end store count exceeded 13,500, with mix broadly unchanged vs. last year and slightly higher exposure to lower-tier cities and franchisees. d. Absolute closures were similar to FY24, while the closure rate declined notably vs. FY24. e. Over 12,000 stores are equipped with coffee machines, essentially achieving full coverage.

2. Accounting standards and profit adjustments (MPM)

a. Early adoption of IFRS 18 MPM (Management-Defined Performance Measures), with clear definitions of adjustments. b. The largest adjustment was the fair value change of pre-IPO preference shares (just over RMB 500mn in FY25), due to the Dec-24 valuation exceeding the Feb-25 IPO valuation; this will not recur. c. Listing expenses are one-off; the withholding tax adjustment on onshore-to-offshore dividends is to improve comparability with companies that do not pay dividends. d. Added an FX translation gain/loss adjustment — roughly HK$2bn raised in the IPO was not converted into RMB, and a ~5% depreciation of HKD/USD vs. RMB led to a loss of about RMB 100mn; this is non-recurring, and different accounting treatments (P&L vs. OCI) can create differences.

3. Shareholder returns and capital allocation

a. Rationale for buying land and building HQ: currently low construction and land costs, talent stability (avoid relocation-driven attrition), and structurally rising rental costs. b. The company remains asset-light, with no ongoing increase in heavy assets beyond HQ. c. Any new large-scale investments will be communicated promptly to investors.

4. Response to market sentiment

a. The long-term focus is on the interests of shareholders and franchisees, without managing short-term expectations up or down. b. Management cautioned against linear extrapolation — profit rose only 5% from FY23 to FY24, then handily beat expectations from FY24 to FY25. c. Investors are encouraged to do deeper fundamental work and take a longer view of the trajectory.

2.2 Q&A

Q: How does the ebbing delivery war affect store profitability and this year's same-store performance?

A: The delivery war affected store revenue more than the company's revenue. Its peak was in Jul–Aug, with a smaller spike in May, and it did not run through the full year; the full-year headwind was a bit above 5% but below 10%. The bigger impact as delivery fades is the higher delivery mix compressing franchisee profitability.

We started preparing in 2023. Across 2024–2025 we made extensive changes, lifting our effective take rate on delivery by nearly 10ppts vs. early 2024, chiefly by pricing delivery orders RMB 3–4 above dine-in. This gave us flexibility — as delivery normalizes, we can adjust prices to keep stores healthy.

The delivery mix has come down from a near-60% peak to around 50%, bringing dine-in back to a healthier level. Our realized take rate on delivery is about 78%, well above the industry’s typical 55%–65%. We also provide the least product subsidies on delivery among peers.

Overall, the delivery slowdown has a minimal impact on HQ revenue. We have several levers to offset it. If forced to choose, we would sacrifice some near-term HQ margin to protect store profits, but we do not yet see a pressing need.

Q: What is the store opening outlook this year, and how is franchisee appetite?

A: We will focus on three areas: new openings, relocating stores within trade areas, and remodels. Total openings will be around the FY25 level, with a +/-500 range; following the positive profit impact from the new store image last year, we will emphasize remodels and site optimization this year, lifting Gen-6 stores from 4,000 to about 10,000.

We encourage franchisees to complete remodels and openings ahead of the summer peak, as a one-week shutdown during peak season is costly. This is one reason we rolled out franchise subsidies early in the year.

Q: A peer is pushing a 'fresh ingredients' strategy. How do you view competition this year?

A: The push for fresher inputs is longstanding and not unique to one brand. The challenge is the long build cycle, spanning the move from factory-processed goods to agri semi-finished products, deep processing, and process technology, which requires reconstructing the end-to-end supply chain; it is not just logistics and warehousing, but end-to-end alignment from product to supply chain to in-store ops, and cannot be iterated within one to two years.

In cold-chain, there are deep- and shallow-water zones. Many brands use frozen inputs, including juices; the cold-fresh part is much harder, starting with basics like citrus and milk and getting tougher beyond that; achieving stable quality at controllable cost requires long-term tuning. Peers moving toward freshness validates our long-term direction, but the challenges are significant; we ourselves are only halfway there, with much more to dig into.

Q: How do you think about the future dividend payout ratio?

A: Our IPO pledge is to pay not less than 50% of profit after major CapEx. If you use adj. core profit of RMB 2.8bn as the denominator, the headline payout looks about 38%; but the onshore-to-offshore dividend withholding tax, though accrued in accounting, is a real cash outflow — backing that out, the denominator is about RMB 2.6–2.7bn, and the effective payout is around 40%.

On CapEx, investors chose us for an asset-light model, which will not change. Buying land and building the HQ is largely a one-off, with annual build costs of roughly RMB 200mn. Routine maintenance CapEx (vehicles, servers, etc.) is about RMB 100mn per year, a modest outlay relative to operating profit.

Q: How should we think about FY26 GPM? Why did per-cup GMV rise only 1–2% last year?

A: The uplift in per-cup GMV mainly reflects the 'foam' from including delivery fees. With a higher delivery mix, GMV includes delivery fees, while actual store pricing barely changed. Ex-delivery, per-cup price even dipped slightly due to mix — coffee is priced a bit lower on average, and summer introduced relatively lower-priced items like lemonades.

Store pricing determines company sales, which saw little change this year and likely won’t next year. GMV on a delivery-fee-inclusive basis may fall as delivery normalizes, but this does not affect true GP.

On GPM, FY25 improved by about 250bps, partly because some transport costs are booked in cost of revenue and because more new stores opened in mature regions, lowering marginal warehousing and delivery costs. Looking to FY26, GPM should rise modestly without large swings, with FY25 as the more appropriate benchmark. Over a 3–5 year horizon we aim for stability, with normal +/-100–200bps moves each year, while keeping franchisee and system-level gross margins healthy.

Q: What opportunities did the delivery war create for Guming?

A: New users acquired via platforms effectively gave us low-cost customer acquisition; we focus on repeat and retention and are confident in conversion after acquisition.

More importantly, there are strategic opportunities. The delivery war brings orders but can harm single-store economics; we chose not to chase short-term financial income from delivery because we saw that the war makes it harder for standalone franchisees to survive, strengthening industry leaders. When the tide recedes, healthier stores mean a stronger base and higher market share.

Our FY25 strategy was to prioritize store health over top-line speed. When some stores in the market were loss-making, our store profitability improved, which is positive for share gains.

Q: How is brand building progressing this year?

A: The brand image will change significantly this year. A new logo has started to roll out, and the overall visual identity is undergoing a major iteration. On store design, Gen-7 will launch in H2, and Gen-6 will reach about 10,000 by year-end; in products, we aim to shift the track from milk tea to 'tea + coffee'.

Key strategies last year only reached about 50% execution. For example, daily coffee sales are now in the 80+ cup range, with a full-year target of 120+ cups per store. We will also launch more differentiated coffee — last year focused on basics to build a value-for-money quality perception; this year we will answer 'who we are', with products like 'Ku Jin Gan Lai' as a first attempt; leveraging our strength in fruit, fruit-coffee and other accumulated products will see a concentrated push this year. Foundational coffee will also keep iterating as the long-term core, while other new strategic projects are underway but not yet ready for disclosure.

Q: What are the levers for same-store growth this year?

A: In FY26, the main SSSG headwind is the unwind of the delivery war, which we estimate at over 5ppts; however, several tailwinds exist.

First, coffee will contribute meaningfully to SSSG. Coffee only started to scale from late Sep and Nov last year, with 70–80 daily cups only from year-end, affecting only about three months of FY25; in FY26 coffee contributes for the full year, and growth remains strong.

Second, Gen-6 stores materially outperform Gen-5. Gen-6 will increase from 4,000 to about 10,000 stores, averaging roughly 8,000 for the year, which should lift SSSG.

In addition, breakfast and the new brand image have yet to be fully realized. In Q1, on our internal standard flow metric that excludes delivery fees, same-store growth was double-digit; SSS is the hardest metric to control and takes time to show, with many external factors. We are confident at least not to see SSS decline; the exact uplift is not our guidance, though Q1 improved clearly both QoQ and YoY.

Q: How was franchisee profitability in FY25 and what is the trend? Any gap between new and old franchisees?

A: Franchisee store profits rose significantly in FY25 to a record high. In Q4, even as delivery faded and peers saw revenue without profit, franchisee net profit still grew double-digit YoY; in FY26 Q1, excluding special events, per-store profit was still meaningfully higher vs. FY25 Q1. Not every franchisee grew, and we provide targeted support to underperformers.

Regarding new vs. old, new stores opened in H2 FY25 outperformed older stores on dine-in, a first in over a decade; in H1 FY26, dine-in for new stores (Jan–Jun) is also ahead of older stores. This stems from a much finer-grained site selection process in FY25 and tighter management; moreover, delivery is not fully ramped at new stores, with some not yet live on delivery channels. Overall, new franchisee quality is improving, and interviews will become more rigorous.

Q: What is the logic behind the franchise subsidy policy? Will it cannibalize older stores?

A: We budget subsidies every year, with a different focus this year around three objectives.

First, encourage remodels and new-store fit-outs before the summer peak, as a one-week shutdown in Jul–Aug is uneconomic. Second, prioritize support for small franchisees with one to two stores and discourage rapid expansion by large franchisees, who tend to over-expand and suffer weaker management efficiency; we want them to optimize existing stores first. Third, support relocating older stores to better sites where trade areas have degraded or original sites were suboptimal. Subsidies are not incremental spend but targeted use of the normal budget; with higher HQ profits and better franchisee intake, we have more resources for such transfers, but we will be precise — targeting operators with strong effort, QC, and key locations, not blanket subsidies.

In some trade areas, new stores may partially cannibalize old ones, which is why optimizing locations is a focus this year. We remain vigilant and proactive about these issues.

Q: How are FY26 openings allocated by region and city tier? Will you enter tier-1 cities?

A: We have no concrete plan for quasi-tier-1 cities this year, and Shanghai and Beijing are not priorities. Tier-1 cities have higher delivery mix, labor, and rent, but pricing cannot be 1.5x–2x that of tier-2; all milk tea brands struggle to make strong profits in tier-1, and franchisee margins are low, with intense mall clustering and tough competition. Given finite resources, they are not top priority.

The split between cities and towns will be similar to previous years. This year's focus includes Guangxi/Guangdong already surpassing Zhejiang, and Yunnan/Guizhou/Sichuan, where Guizhou also surpassed Zhejiang, so we will prioritize less dense regions; in North China, Shandong's Avg. performance has recovered to within RMB 100 of Jiangxi, and new stores in Shaanxi and Hebei are doing well, but we will pace prudently rather than open aggressively. We advance by region in phases: new → semi-mature → mature → tail.

Q: Why did Guming respond best to the delivery war, and is this sustainable?

A: The core is separating HQ macro control from frontline execution. When the delivery war hits, frontline staff and franchisees naturally chase short-term volume, but they are hurt first when it unwinds; our approach is to control pricing centrally at HQ.

For example, if dine-in is RMB 15, delivery is set at RMB 18–19 including packaging, leaving franchisees with over RMB 14 per cup and healthy margins; many brands only lift to RMB 16, and after platform take rate, franchisees pocket about RMB 11 with large profit erosion.

This means we could have pushed delivery volume higher in FY25 but chose not to maximize it. As delivery normalizes, we do not need extra subsidies to hold sales — trimming delivery from RMB 19 to 18 still leaves franchisees with RMB 14–15, protecting profit while maintaining volume.

Our delivery team, from management to ops, is adept at A/B testing on parameters like delivery fees and pricing; often it is simply a matter of choice — when delivery orders can go from 4,000 to 5,000, do you take 4,500 or 5,000? Choosing to sacrifice some volume makes the unwind less painful.

Ultimately, agility matters. Dine-in is the healthier revenue stream — rough math shows RMB 3,000 of delivery contributes less net profit to a store than RMB 1,000 of dine-in, so we channel most promotions and traffic to dine-in to avoid an unhealthy delivery mix.

Q: Does the larger footprint of Gen-6 stores extend payback? How do you convey the differentiated 'fresh' proposition to consumers?

A: At equal area, Gen-6 fit-out cost is actually lower than Gen-5 due to process optimizations; average area is about ten-plus square meters larger, so total cost is higher, adding roughly RMB 10,000 per year assuming four-year depreciation. ROI has not declined, helped by the significant uplift in store profits in FY25; the share of unhealthy stores did not rise and actually fell.

The top three drivers of store profit pressure are ranked as follows: (1) overly rapid franchisee expansion leading to management inefficiency (e.g., jumping from 5 to 10 stores); (2) higher delivery mix causing revenue without profit (the biggest headwind for most brands); (3) higher fit-out and equipment costs, which are far less impactful than the first two.

Introducing coffee machines (RMB 70–80k per unit) was a bigger shock than enlarging Gen-6 footprints — previously, all store equipment might total RMB 100k, so adding an RMB 80k machine was almost unthinkable; it proved right in hindsight. In FY25 we also offered installment plans for equipment and franchise fees, with zero down payment in year one, and set up a used equipment buyback unit to reduce losses and the psychological burden if a franchisee exits.

Risk disclosure and statement: Dolphin Research disclaimer and general disclosures