Gu Ming: Subsidies Fade, Tea's 'Costco' Stays Solid!

On the evening of Mar 25 Beijing time, $GUMING(01364.HK) reported H2 2025 results. Overall, the second-half print was solid, and vs. BBG consensus, most core operating metrics were in beat territory except for a temporary overshoot in marketing spend tied to the coffee category rollout. The stock opened higher but faded intraday on the following day; per Dolphin Research’s checks, the pullback likely reflected profit-taking after the company had briefed some institutions earlier in small-group meetings.

Key takeaways:

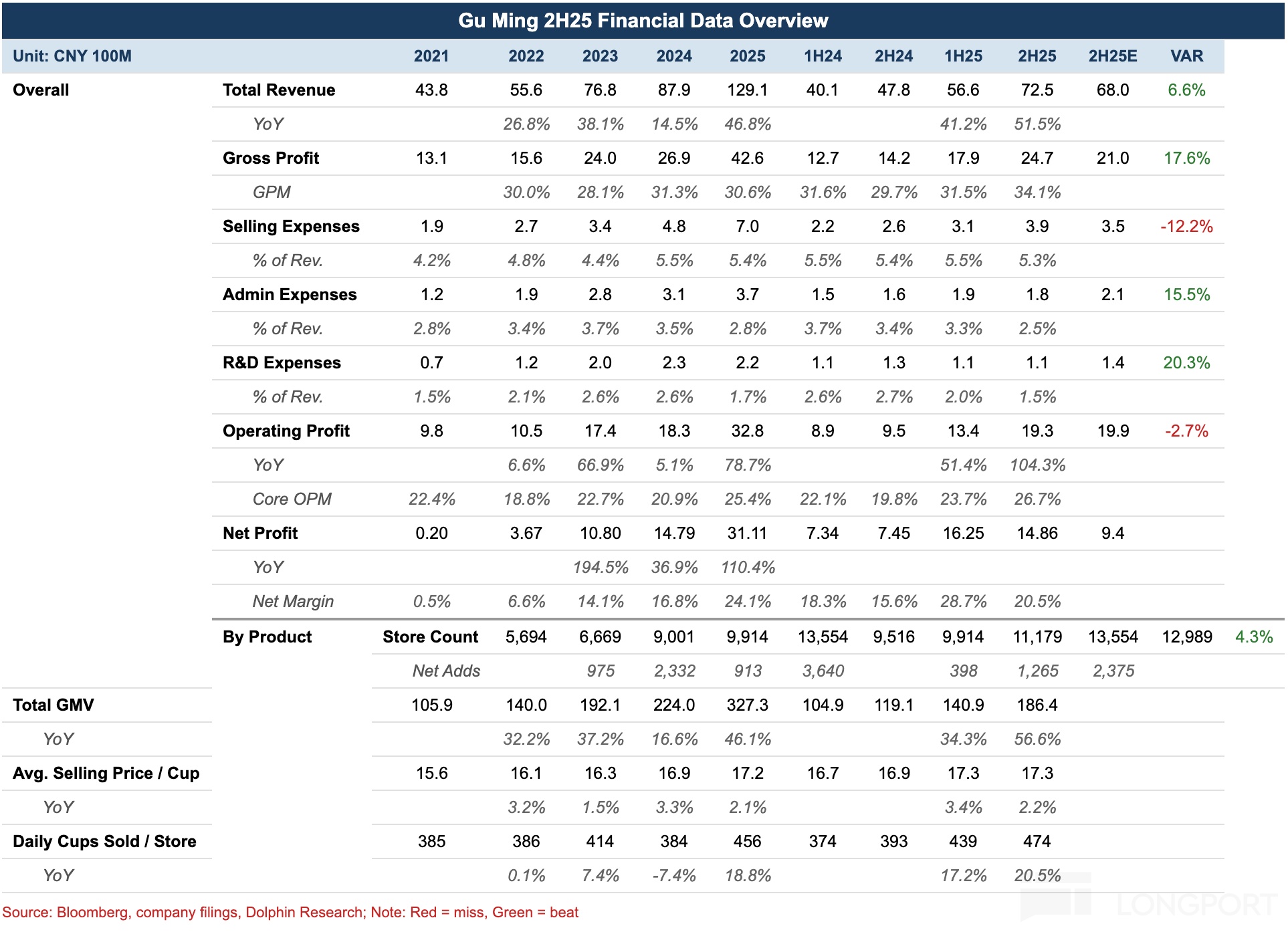

1) New and mature stores both contributed; revenue stayed on a fast track. Benefiting from denser store openings, delivery subsidies, and the newly launched coffee offering lifting same-store sales, $GUMING(1364.HK) delivered H2 revenue of RMB 7.25bn (+52% YoY). Unlike Mixue, whose revenue growth is largely store-add driven, channel checks suggest $GUMING(1364.HK) saw close to 20% SSS growth in H2, implying higher-quality growth than Mixue’s.

2) Store expansion shifted into high gear. Boosted by the coffee category’s breakout and upgraded franchise support, net adds reached 2,375 stores in H2, roughly double H1. By region, the company focused on densifying markets that have yet to reach critical mass, with most openings coming from existing franchisees adding second or multiple stores. Structurally, new stores skewed further toward lower-tier markets, and the share of stores in Tier-3/4 cities rose another 80bps HoH to 58%.

3) Record cups per store. On store operations, Dolphin Research estimates Avg. GMV per franchised store reached RMB 1.507mn in H2 (+23.6% YoY). Daily cups per store averaged 474 (+20.5% YoY), the key driver; beyond delivery subsidies, the large-scale coffee rollout and expanded morning hours also materially lifted traffic. On pricing, while the company did not disclose details, we estimate ASP at RMB 17.3 per cup, roughly flat vs. H1.

4) GPM hit a new high. Gross margin expanded sharply, as $GUMING(1364.HK) tapered its earlier raw-material concessions to franchisees and drove supply-chain efficiencies and cost-outs. H2 GPM rose 440bps to a record 34.1%.

5) Operating leverage unlocked profitability. On opex, to support coffee promotion, the company stepped up brand investments including celebrity partnerships and ad spend, keeping the S&M ratio roughly flat. Meanwhile, the G&A ratio fell 90bps to 2.5% on better operating efficiency, taking OPM to a record 26.7%.

6) Financial snapshot:

Dolphin Research’s take:

Purely on H2 performance, we see no red flags: with both SSS and new-store growth running fast, operating leverage pulled down expense ratios. While 2026 faces a tough comp as subsidies fade against a high 2025 base, much depends on how many new customers acquired during the delivery subsidy battle can be retained for repeat purchases. On this, we are confident in $GUMING(1364.HK)’s product strength.

Channel checks indicate that even in its most competitive and densest home market, Zhejiang, SSS has grown every year except 2024, when the industry was in an extreme price war. This suggests high store density does not necessarily imply SSS erosion; rather, density can amplify supply-chain efficiency, per-drop delivery cost, and brand mindshare. In our view, the real swing factor for sustained SSS growth is whether $GUMING(1364.HK) can consistently hit mass tastes while keeping strong value-for-money and freshness.

From a valuation angle, although slower delivery subsidies in 2026 may pressure cup volumes, we assume rising coffee penetration can offset this, keeping cups stable, and 2026 earnings fully store-add driven (3,000 net new stores). That implies net profit of RMB 3.5bn at roughly 15x, which is not demanding vs. our 3-yr EPS CAGR est. of 18%+. With the medium-to-long-term thesis intact, we see limited downside at current levels and ~20% upside on a re-rate to 18x.

Detailed earnings analysis below:

I. New and mature stores both contributed; revenue stayed on a fast track

From an overall perspective, denser openings, delivery subsidies, and the coffee launch improved SSS, taking H2 revenue to RMB 7.25bn (+52% YoY), an acceleration vs. H1. Unlike Mixue (low single-digit SSS), our checks indicate H2 growth for $GUMING(1364.HK) was driven by roughly 30% store growth and 20% SSS growth, underscoring higher growth quality than Mixue.

II. Deeper into lower tiers; faster store openings

On expansion, fueled by coffee’s breakout and stronger franchise support, net adds reached 2,375 in H2, roughly doubling H1, bringing total stores to 13,554. Across the tea & coffee space, the Matthew effect intensified in H2: per Tea & Coffee Watch, the top 10 brands drove >90% of net openings, while many small/mid brands saw net closures.

By region, $GUMING(1364.HK) focused on densifying Tier-3/4 cities and townships within eight core provinces (Zhejiang, Fujian, Jiangxi, Guangdong, Hunan, Hubei, Jiangsu, Anhui), with township store mix rising from 41% to 44%. Channel checks show >50% of H2 adds came from existing franchisees opening second or multiple stores, signaling strong loyalty. In higher-tier (Tier-2+) markets, the company prioritized store upgrades: bigger facades, improved image, and expanded outdoor seating.

On the earnings call, management guided 2026 net adds not below 2025 levels. This implies another year of rapid footprint expansion in 2026.

III. 'Shovel-selling' revenue mix ticked up

On mix, sales of goods and equipment reached RMB 5.77bn in H2 (+50% YoY), with segment contribution up 20bps vs. H1. Based on our checks, we think this reflects a pullback in raw-material concessions to franchisees in H2.

IV. Record cups per store

On store-level throughput, H2 GMV reached RMB 18.6bn (+56.6% YoY). While the company did not disclose SSS, channel checks suggest H2 SSS approached +20%.

Breaking it down, daily cups per store averaged 474 (+20.5% YoY), the core driver; beyond delivery subsidies, the large-scale coffee rollout in H1 continued to lift cups in H2. Coffee’s revenue mix jumped from <10% in H1 to roughly 15–20% in H2. With coffee, many stores moved opening time forward from 10:00 to ~7:30–8:00 and launched 'morning coffee + breakfast' bundles, filling the breakfast gap; per prior company comms, cross-selling is meaningful, with ~65% of consumers buying both coffee and milk tea. On pricing, though undisclosed, we estimate H2 ASP at RMB 17.3 per cup, flat vs. H1.

For more on the coffee strategy, see Gu Ming: Riding delivery on one side and coffee on the other—Is the 'Costco of tea' smiling again?, not repeated here.

V. GPM at a new high

GPM rose sharply as raw-material concessions to franchisees were tightened and supply-chain efficiency improved, taking H2 GPM up 440bps to 34.1%, a record high.

V. Operating leverage unlocking profitability

On opex, the company increased brand-building for coffee through celebrity tie-ups and advertising, keeping the S&M ratio broadly flat. With operating efficiency gains, the G&A ratio fell 90bps to 2.5%, taking OPM to 26.7%, a new high.

Longbridge Dolphin Research on '$GUMING(1364.HK)': prior pieces

Deep dives

Jul 4, 2025: 'Gu Ming: Slow is fast! A 'Costco' in tea?'

Jul 8, 2025: 'Gu Ming: Offense and defense—Can the 'Costco of tea' have the last laugh?'

Commentary

Aug 27, 2025: 'Gu Ming: Riding delivery on one side and coffee on the other—Is the 'Costco of tea' smiling again?'

Risk disclosure and disclaimer: Dolphin Research disclaimer and general disclosures

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.