SpaceX Challengers: Can Bezos and China Inc. Catch Up? ---

SpaceX Challengers: Can Bezos and China Catch Up?

In our previous note, we framed the current commercial space cycle around a potential SpaceX listing. Here we focus on reusable launch vehicles and satellite ops, and break down the value chain to assess competition and where investors might find opportunities.

Body:

I. Competitive landscape in reusable rockets

We map key players in reusable launch, then address two questions: what the competitive dynamics look like, and what differs by tech route and operating model across players. We use those differences to infer the core competitive levers and the upstream/downstream segments they touch.

(1) Bezos’ playbook

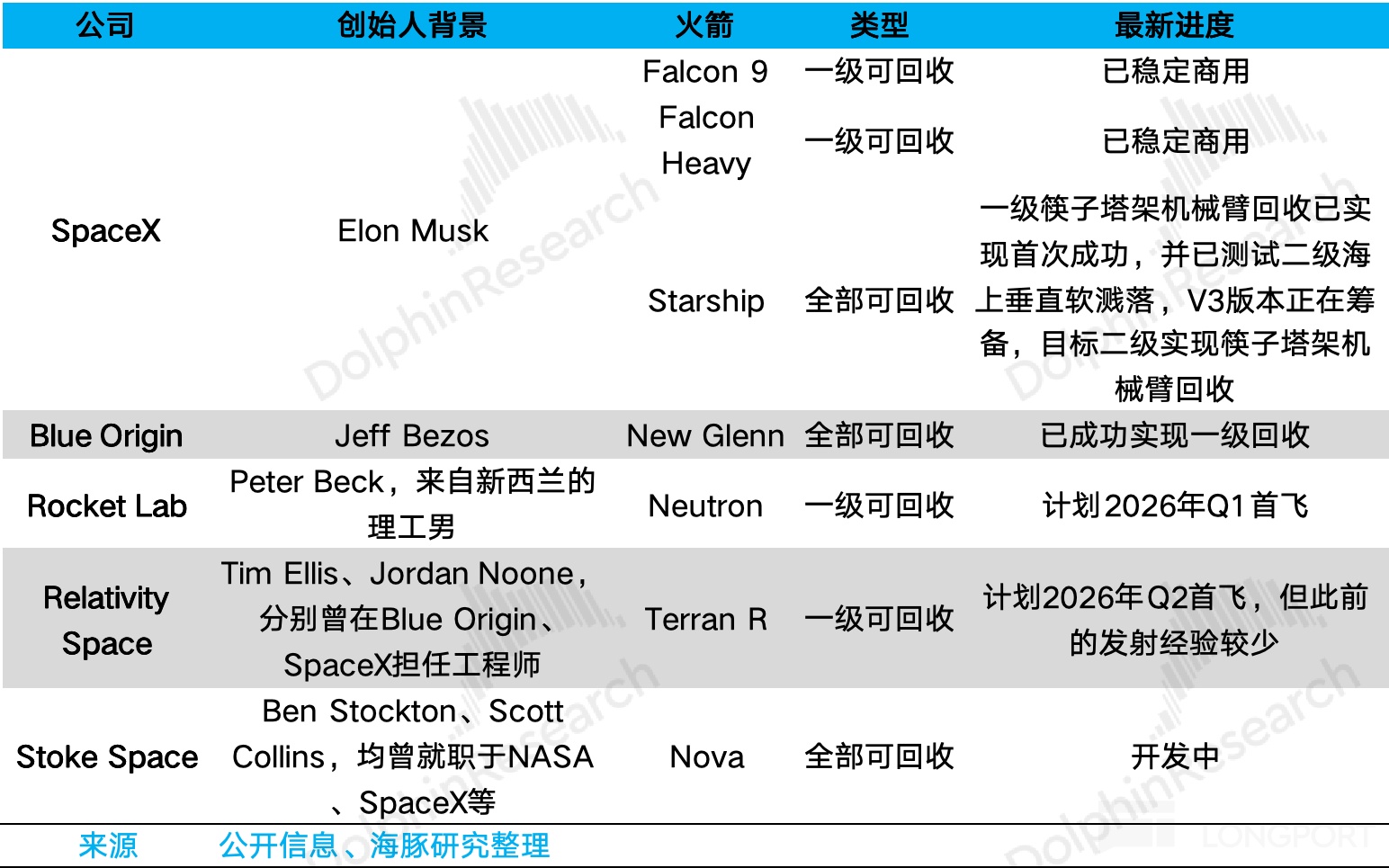

In reusable launch, SpaceX’s most significant rival today is Amazon founder Jeff Bezos. His Blue Origin predates SpaceX, targets lower access costs to space with a similar tech path, and has already mastered parts of reusability.

We compare the two:

1) Philosophy

SpaceX’s vision is to make humanity a multi-planet species, e.g., Mars migration. Blue Origin aims to move heavy industry to space to ease Earth’s burden and make the planet more livable. Different narratives, similar premise: Earth is fragile with finite resources, and neither vision is likely to be profitable near term.

So, even with Bezos’ patient capital from selling ~$1 bn of Amazon stock annually, Blue Origin still needs sustainable revenue. Government and defense work, commercial missions, and a Starlink-like play (Project Kuiper, etc.) are natural steps. That puts Blue Origin in direct, full-spectrum competition with SpaceX.

2) Operating model

While targets and footprints are similar, execution differs materially. SpaceX runs rapid iteration and agile dev; Blue Origin is more traditional, long-term, and incremental. Even at a slower cadence, it has made progress.

New Glenn achieved booster recovery in 2025, the world’s second orbital-class rocket with vertical recovery, landing on an autonomous barge at sea. Its LEO payload is up to ~45 tons, well above Falcon 9 and near Falcon Heavy.

Chart: New Glenn stage-1 re-ignition and recovery

Source: Blue Origin, Dolphin Research

3) Philosophy and model drive tech-route differences

(i) Engines: the key determinant of recovery and low-cost reuse

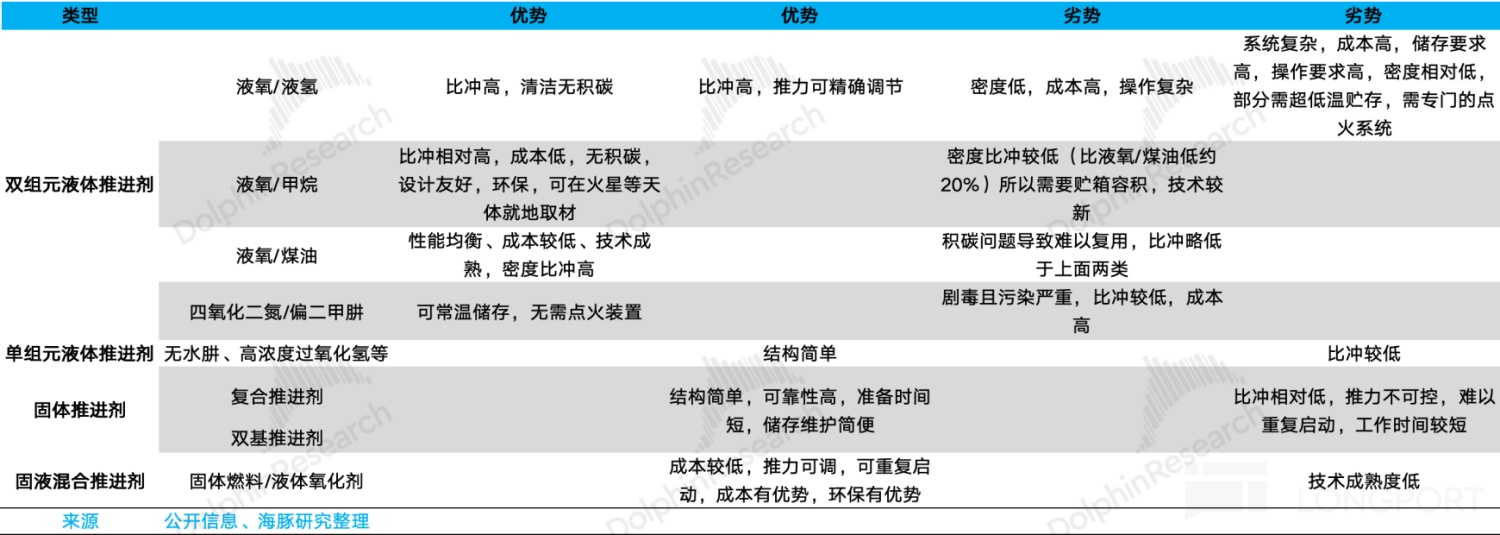

Fuel

Most mainstream propulsion uses bi-propellant liquids, i.e., separate fuel and oxidizer because space lacks oxygen. Blue Origin’s choices reflect an ‘advanced but prudent’ approach. SpaceX uses LOX/kerosene for Falcon and LOX/methane for Starship; LOX/kerosene is mature, reliable, and cheaper, while LOX/methane avoids coking and boosts reuse efficiency, with in-situ resource potential on Mars, but is less mature.

Blue Origin goes straight to LOX/methane, same as Starship. That underscores a step-up approach aimed at long-run reuse.

Cycle

Blue Origin uses oxygen-rich staged combustion. SpaceX’s Merlin (Falcon) runs a gas-generator cycle; Raptor (Starship) uses full-flow staged combustion.

Cycles describe how propellants reach and burn in the chamber to produce thrust, with the core difference being how the turbopump is driven. The turbopump, effectively the rocket’s heart, pressurizes and feeds propellant to the chamber.

In short, oxygen-rich staged combustion offers higher efficiency without coking, and has design/manufacturing maturity. Merlin’s gas-generator is simpler and cheaper, mature but less efficient and less reuse-friendly, while full-flow is the ideal on efficiency, safety and life, yet extremely hard to design and build. This mirrors each firm’s operating philosophy.

3D printing

Rocket engines have complex geometries, iterate fast, and are low-volume, making AM (3D printing) compelling, though reliability and performance constraints remain. SpaceX is aggressive with AM, especially on Raptor. Blue Origin focuses AM on key engine components.

Bottom line: Blue Origin targets advanced-yet-prudent solutions up front, trading time and higher R&D for staged success — real competitive pressure for SpaceX.

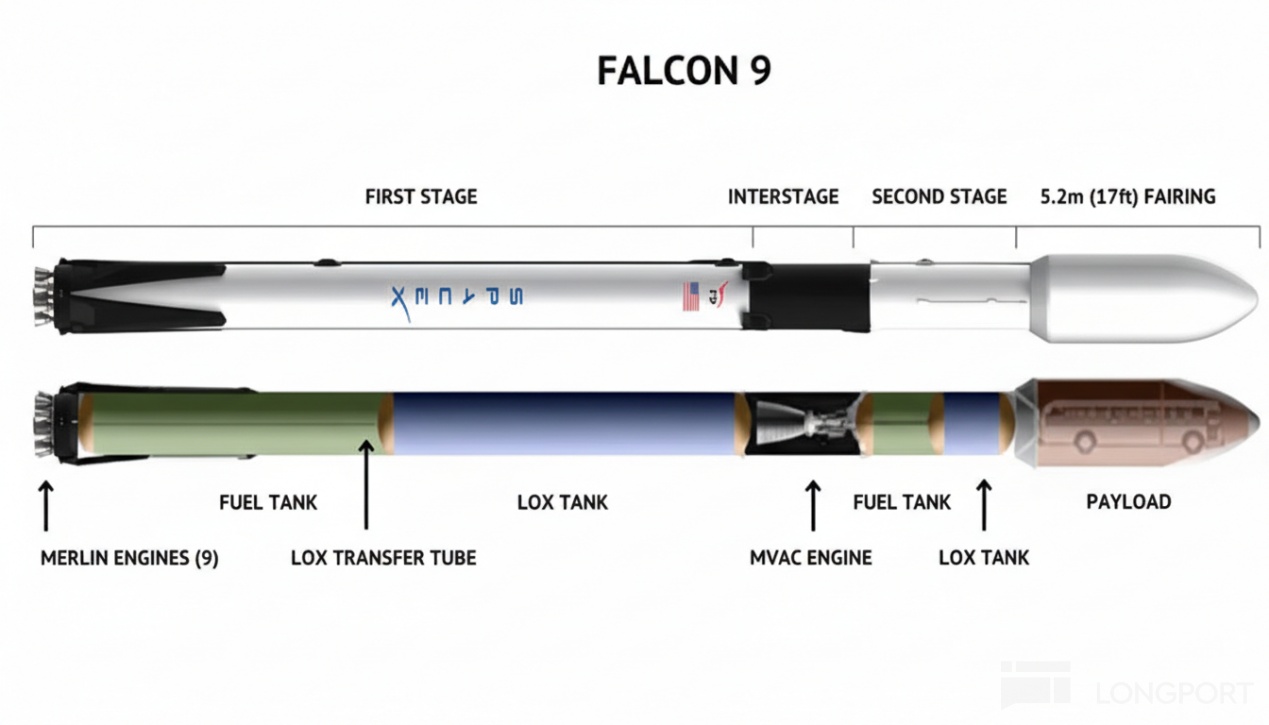

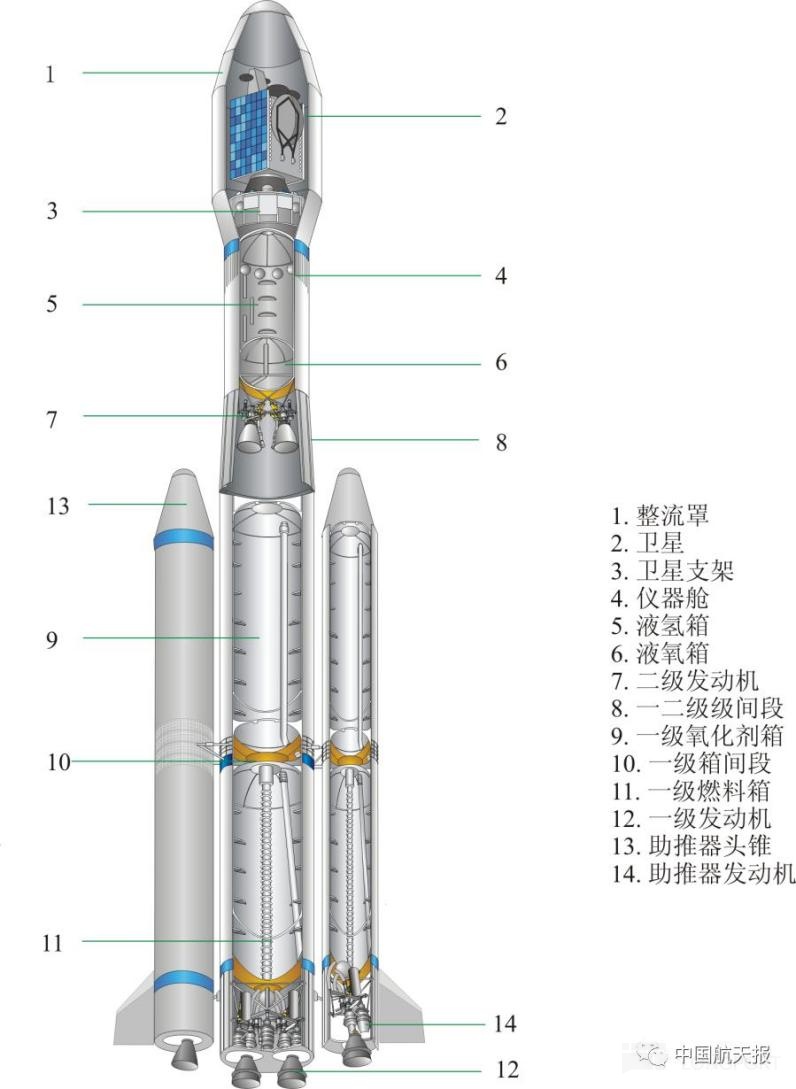

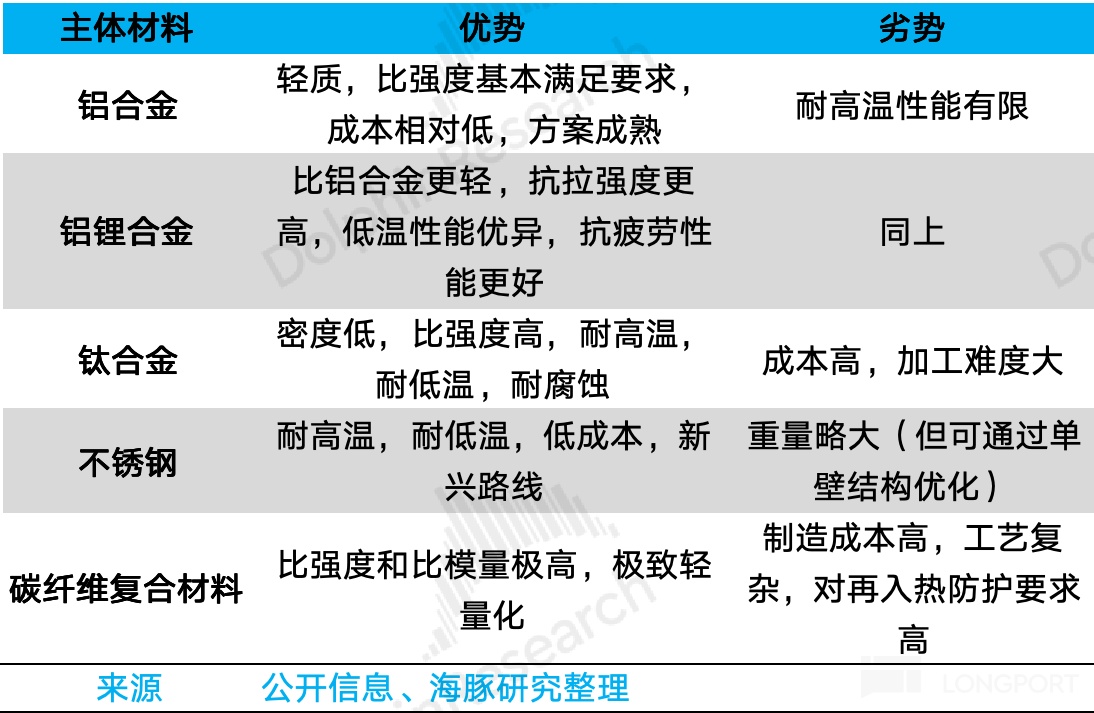

(ii) Structures are the No.2 cost bucket, so materials matter

Excluding R&D and ground-facility D&A, engines are ~40–50% of rocket cost. Structures (airframe) are ~25%, GNC ~15%, and propellant <3%.

Chart: Falcon 9 architecture

Source: Orbital Today, Dolphin Research

Chart: Generic rocket structure

Source: China Aerospace News, Dolphin Research

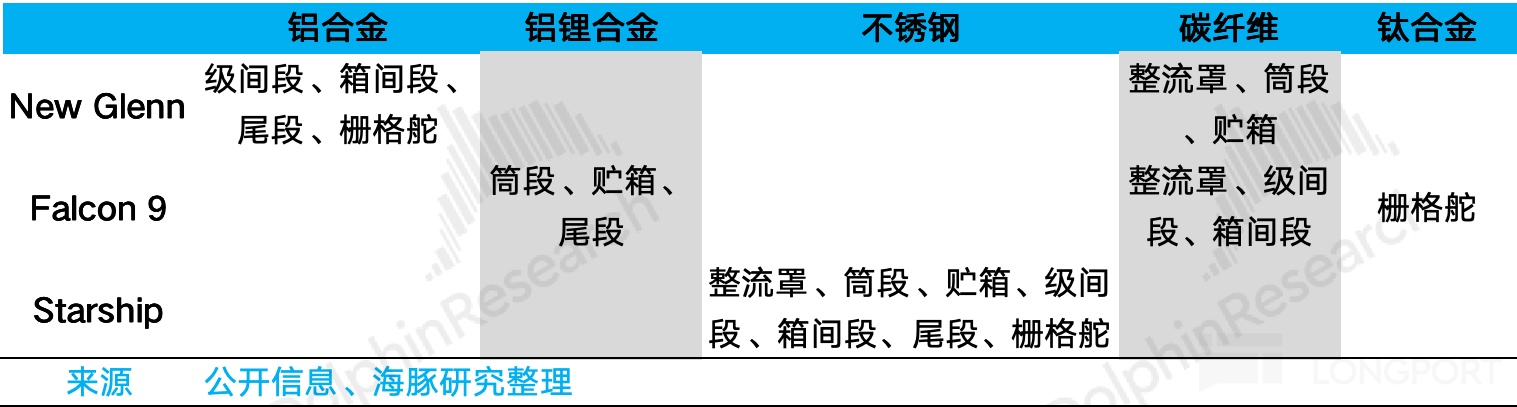

Structures include fairings, cylindrical segments, tanks (propellant storage), interstages, intertank segments, and aft sections. Material choices differ by program.

New Glenn primarily uses aluminum alloys and carbon fiber; Falcon 9 uses Al-Li extensively; Starship is almost entirely stainless steel. Blue Origin favors balanced performance/cost and maturity with optimization, while Starship drives extreme cost-down.

(iii) GNC

GNC covers guidance, navigation, and control. For landing, SpaceX uses ‘hover-slam’: aim directly at the target and fine-tune angle and position en route, maximizing efficiency and saving propellant. Blue Origin uses a ‘drift-in’ approach: aim for a safe point off-platform, confirm nominal, then translate laterally into center, maximizing safety margin.

(2) China’s progress

Most activity is in the U.S. and China, with fewer players elsewhere and slower progress. In Part I, we compared launch costs: while China hasn’t achieved reuse yet, its costs vs. Falcon 9 aren’t an order of magnitude different. If China masters reuse, it could gain cost advantage.

Given China’s manufacturing depth and cost edge, Musk has learned on Tesla autos and Optimus humanoids to abandon fully in-house manufacturing and lean on China’s supply chain. SpaceX is one of the few Musk businesses that can manufacture domestically in the U.S. by disrupting launch economics. If China achieves reuse, SpaceX’s position could be materially impacted.

China remains a fast follower in reusability. Copycat execution isn’t glamorous, but it fits China’s engineering capacity and scale economics.

We outline several faster-moving names:

i) LandSpace

Founded in 2015 by Changwu Zhang (finance background, ex-HSBC) with co-founder Jianmeng Wang (space systems background, ex-CASC launch & telemetry; also Zhang’s father-in-law). Versus SpaceX’s timeline, LandSpace is moving fast.

Its reusable Zhuque-3 was greenlit in 2023 and reached orbit in Dec-2025, just over two years. Falcon 9 took ~5 years from concept (2005) to first successful flight (2010).

Chart: Zhuque-3

Source: LandSpace, Dolphin Research

In the Dec-2025 recovery, Zhuque-3 achieved high-altitude attitude control, re-entry ignition, supersonic glide, and high-precision guidance. It crashed after a late-stage braking failure, but the miss distance was only ~40 meters. Falcon 9 hit similar milestones around 2012–2014, 7–9 years after program start.

ii) SAST (CASC 8th Academy)

Long March 12A was approved in 2021, also on LOX/methane. Shortly after Zhuque-3, it reached orbit in Dec-2025, but recovery failed. Its recovery progress appears slower than Zhuque-3.

iii) CALT (CASC 1st Academy)

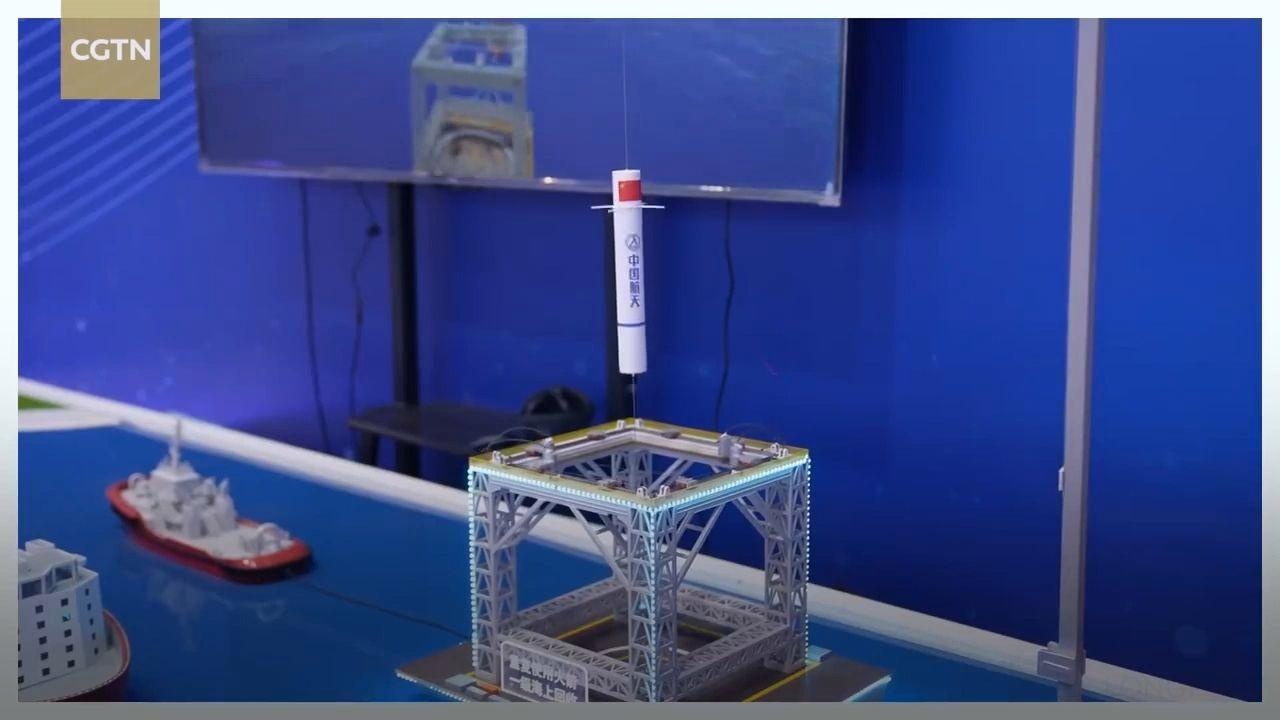

Long March 10A was first disclosed in 2024. In Feb-2026, it completed a dual-test mission, with stage-1 return and a controlled ocean splashdown.

CALT’s recovery differs slightly from SpaceX: a net-capture system. Beyond grid fins and brief retro-propulsive burns near terminal to slow descent, the final capture uses a net device, potentially superior on engineering reliability and cost.

Chart: Long March 10A ocean splashdown

Source: CASC, Dolphin research

Chart: Long March 10A and ocean net-recovery platform models

Source: CGTN, Dolphin Research

iv) Space Pioneer

Founded in 2019 by Yonglai Kang, ex-CTO of LandSpace who left after its solid-fuel route setbacks; previously at CALT. Space Pioneer bet LOX/methane from inception; its reusable Tianlong-3 was launched as a program in 2022, with core ground validation largely complete and first flight imminent.

(3) Rocket Lab

If China’s reusability matures, the first share to lose would be SpaceX’s commercial orders, which are relatively less critical for SpaceX. For U.S. gov. and defense, besides Blue Origin, other credible rivals will also take share.

We focus on $Rocket Lab(RKLB.US). Rocket Lab took a different path.

Founded by Peter Beck in 2006 in New Zealand, it soon partnered with DARPA. It later set up U.S. HQ in California while keeping core R&D and launch in NZ.

In 2018, the small commercial Electron reached orbit. In 2021, Rocket Lab unveiled Neutron (Falcon 9 peer) and listed on Nasdaq the same year.

Why did Rocket Lab break out? We see several reasons:

1) Differentiated positioning

Chart: Rocket size comparison

Source: Spacenews, Dolphin Research

Falcon 9 can rideshare many satellites in one go, driving unit economics, but each payload must fit the mission, reducing flexibility. Electron is purpose-built for smallsat dedicated orbit insertion, a differentiated niche vs. Falcon 9 that fills a market gap. If Falcon 9 is the bus, Electron is the taxi.

2) U.S. gov./defense security needs

Demand exists for frequent, reliable launch capacity. But regulators won’t tolerate single-supplier monopoly risk, so they support second/third sources. That’s why Rocket Lab got early DoD partnership.

3) Unique builder culture, high vertical integration, extreme cost-down

Founder Peter Beck lacks a college degree, but has deep practical manufacturing experience across yachts, appliances, etc. Highly pragmatic, he saw U.S. space suffering from low innovation and high costs and set out to build low-cost rockets. He stays deeply technical and pivots quickly, e.g., reversing on reusability after SpaceX’s success.

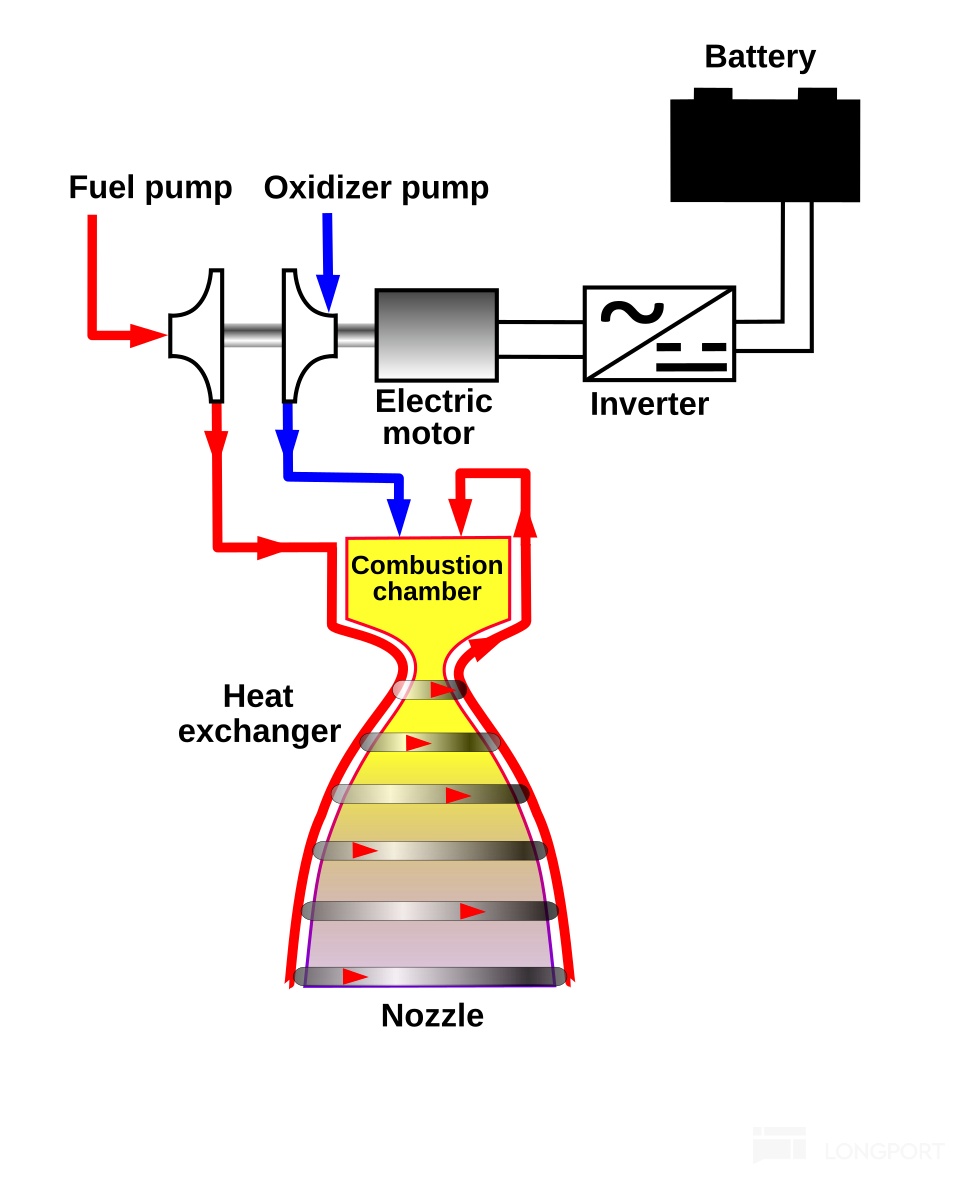

Electron’s tech route, aligned to its niche, differs from SpaceX: Rutherford engines use an electric pump-fed cycle, with Li-ion batteries driving motors that power the turbopump, ideal for small launchers. Rutherford’s major engine parts are produced via AM, even more extensively than SpaceX.

Chart: Electric pump-fed cycle

Source: Wikipedia, Dolphin Research

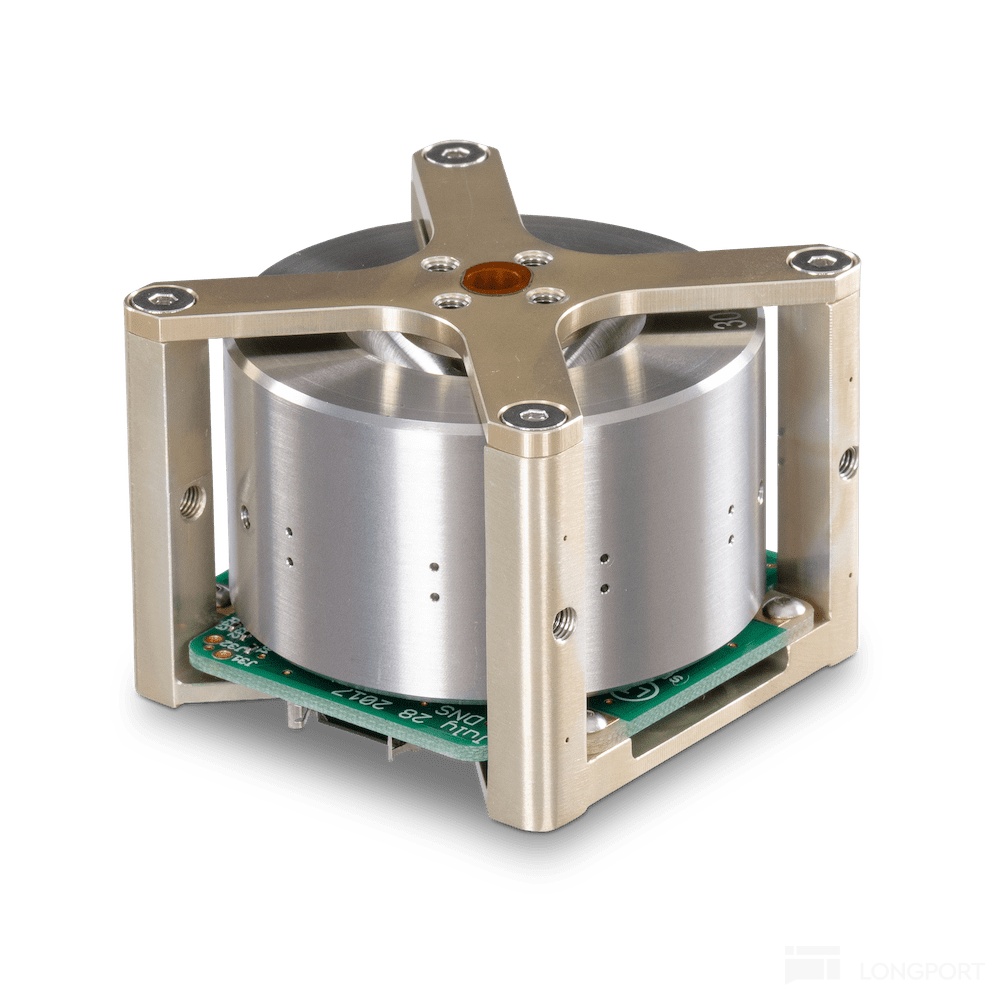

Chart: Rocket Lab’s carbon-fiber 3D printer

Source: Rocket Lab, Dolphin Research

Rocket Lab executed Electron with just ~$100 mn, then rapidly built cross-hemisphere launch, manufacturing, and R&D hubs. It has strong vertical integration.

Chart: Launch sites in NZ and Wallops, VA

Source: Rocket Lab, Dolphin Research

Beyond rockets, Rocket Lab builds satellites and platforms, offering turnkey spacecraft for clients. It also in-sources and sells core subsystems and parts, including GNC components like star trackers and reaction wheels, comms, separation systems, solar arrays, and even space software.

Chart: Rocket Lab’s star tracker & reaction wheels

Source: Rocket Lab, Dolphin Research

Chart: Rocket Lab solar array systems

Source: Rocket Lab, Dolphin Research

Much of its integration came via M&A, showcasing consolidation skill. E.g., Geost added electro-optical/IR; SolAero brought rad-hard PV cells and array modules.

Looking ahead, Rocket Lab vs. SpaceX won’t stay purely differentiated.

On launch, Neutron directly targets Falcon 9-class missions in mega-constellation deployment and deep-space exploration. First flight is planned for Q1-2026.

Neutron’s design differs from mainstream: its ‘Hungry Hippo’ fairing is integrated with stage-1, opening like a hippo’s mouth to release stage-2, then returning with stage-1. Fairing recovery efficiency rises and costs fall. With stage-2 housed inside the fairing, it avoids heavy structural shells, enabling smaller dimensions and shifting mass/cost to stage-1, improving cost dilution via stage-1 reuse.

Chart: Neutron fairing opens and releases stage-2

Source: Rocket Lab, Dolphin Research

On satellites, Rocket Lab launched the Flatellite platform to boost per-mission deployment counts. Combined with its sat-manufacturing base, it could evolve into a services operator and build its own constellation, competing with Starlink.

II. Competitive landscape in constellation ops

SpaceX faces rising competition not just in launch but in constellation operations. Starlink’s core service is global broadband, analogous to home internet, requiring a Starlink Terminal with a phased-array antenna. The terminal functions like an optical modem.

Chart: Starlink Terminal

Source: SpaceX, Dolphin Research

SpaceX is also developing D2D (Direct to Device), or D2C (Direct to Cell), akin to cellular networks. Phones connect directly to satellites via this service.

1) Global broadband: Bezos’ challenge

Blue Origin’s plan

Blue Origin’s Project Kuiper is advancing quickly and directly targets Starlink. Over 100 satellites have reached orbit. Amazon also plans TeraWave, with higher bandwidth and faster service for premium enterprise users.

China’s plan

China has launched GW (China SatNet), Qianfan (Shanghai Yuanxin), and Honghu constellations, with Qianfan aimed at consumer and enterprise customers. China SatNet and Shanghai Yuanxin have secured domestic sat-internet licenses.

In late-2025, China filed with the ITU (a UN agency that allocates satellite spectrum and orbital slots and sets standards) for 14 constellations including GW and Qianfan, totaling ~203k satellites. This far exceeds Starlink’s current on-orbit count.

2) D2D: direct-to-handset competition

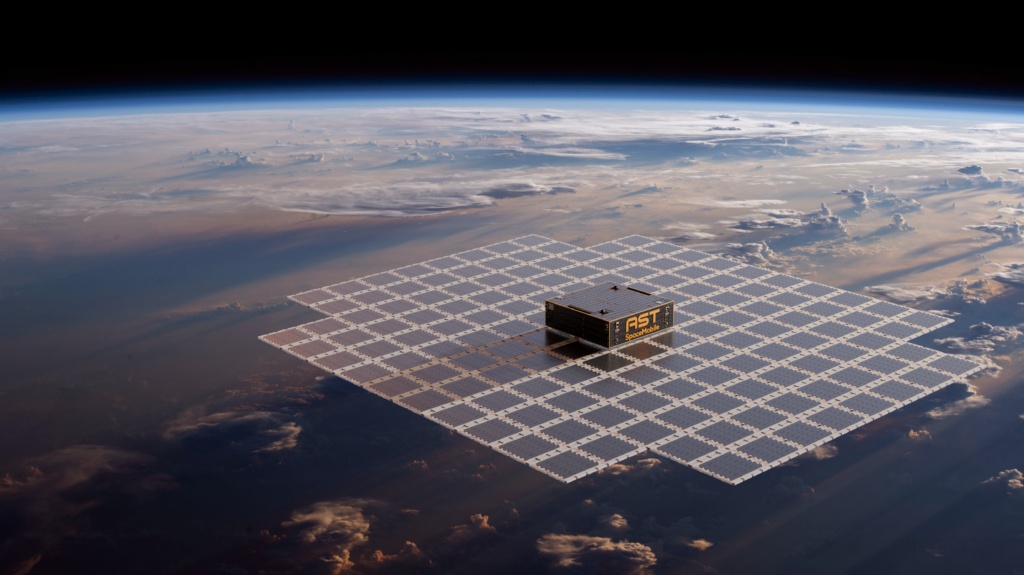

U.S. startup $AST SpaceMobile(ASTS.US) is progressing on satellite-to-phone. Its constellation is only dozens of satellites, claiming giant phased arrays to offset low counts, but capacity may still trail Starlink’s tens of thousands. If parity were feasible, Starlink could adopt similar or hybrid architectures.

With backing from Big Tech, such as Google, AST could still pressure SpaceX. Other D2D programs in the U.S. are underway as well.

Chart: AST SpaceMobile uses giant phased arrays for D2D

Source: AST SpaceMobile, Dolphin Research

Still, satellite comms have fewer disruptive moats than launch. As Blue Origin and others mature in rockets, satellite operators have more cost-effective launch choices — that’s the core competitive lever. The race in reusability remains the key.

3) Spectrum and orbital slots: urgency rising

Resource scarcity

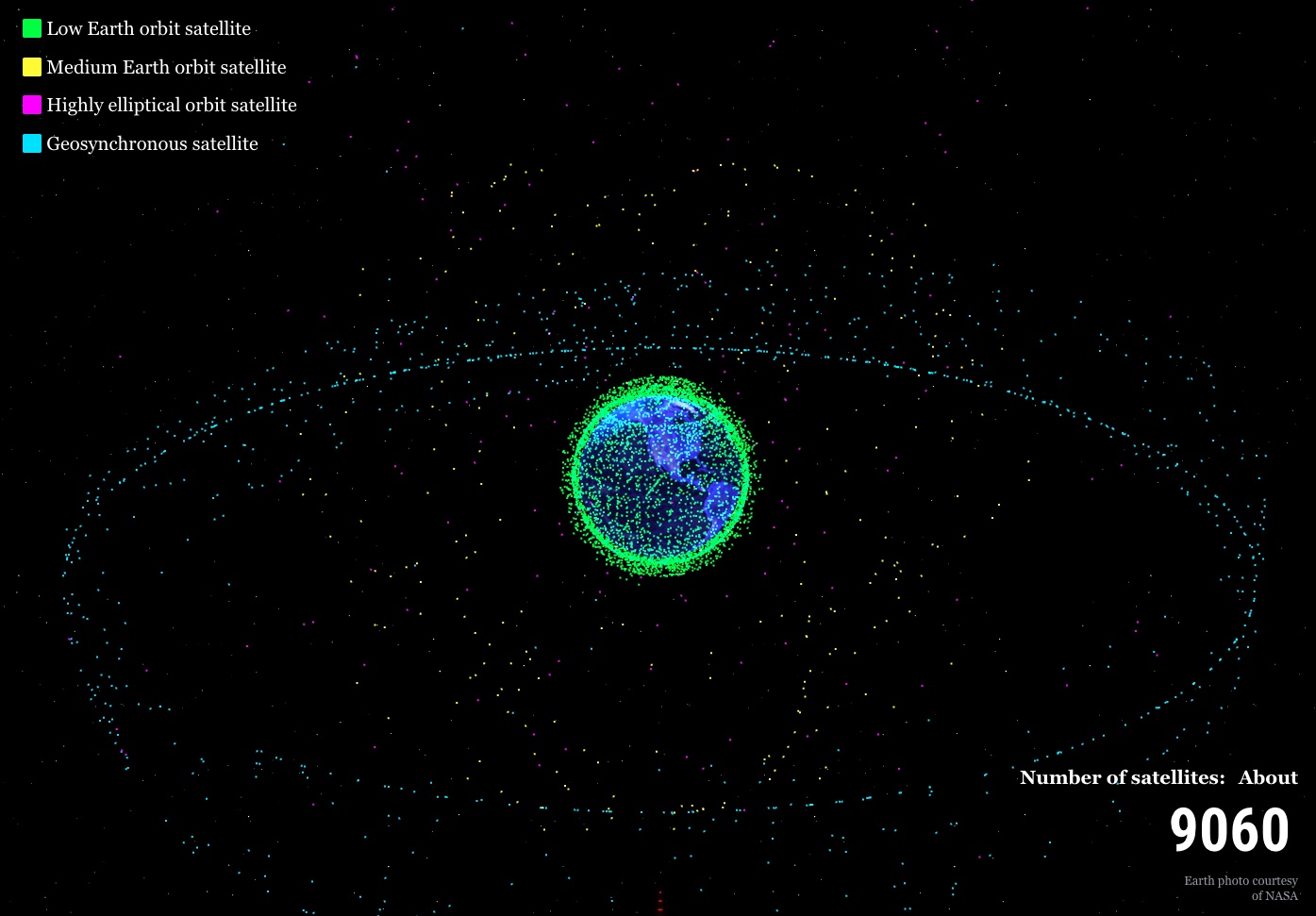

Spectrum and orbital slots are finite and allocated first-come, first-served. LEO orbital capacity is theoretically ~60k satellites. Starlink is nearing ~10k on-orbit, while ITU filings across countries now total in the hundreds of thousands.

Chart: On-orbit satellites

Source: NikkiAsia, Dolphin Research

Per ITU rules, by year 7 post-filing you must launch and successfully operate one satellite for 90 days. By year 9, 10% of the filed constellation must be deployed; by year 12, 50%; by year 14, 100%.

National security

Strategically, Starlink demonstrated significant military value in the Russia–Ukraine war: with terrestrial comms degraded, Starlink kept Ukraine online. It supported ISR and comms via drones, coordinated long-range combined arms, and maintained real-time connectivity with NATO.

Spectrum and orbit aren’t just commercial assets; they underpin national comms sovereignty and security. This is a crucial window. Whoever places more satellites faster gains advantage, and 2026 will see more reusable rockets enter flight testing, reflecting the competitive stage.

III. Where are the opportunities?

1) Launch providers

SpaceX led commercial space into reusability, collapsing launch costs and catalyzing demand. Given multiple players’ momentum and milestones, full reusability should continue to iterate quickly — it’s a matter of time.

The market is unlikely to be monopolized. SpaceX created a viable path, compressing followers’ R&D cycles. Bezos’ more conservative cadence still delivered milestones, and buyers won’t accept single-supplier risk, so they will nurture rivals, accelerating catch-up.

Even so, SpaceX remains ahead technically, and if Starship achieves full reuse, its cost curve could reset again. Starlink’s early network effects also strengthen the first-mover moat.

In a blue-ocean space, we see opportunity both in SpaceX and in credible chasers. Among chasers, Rocket Lab stands out for tech leadership, rapid iteration, and core gov./defense positioning, but Neutron’s first-flight progress is the key watch.

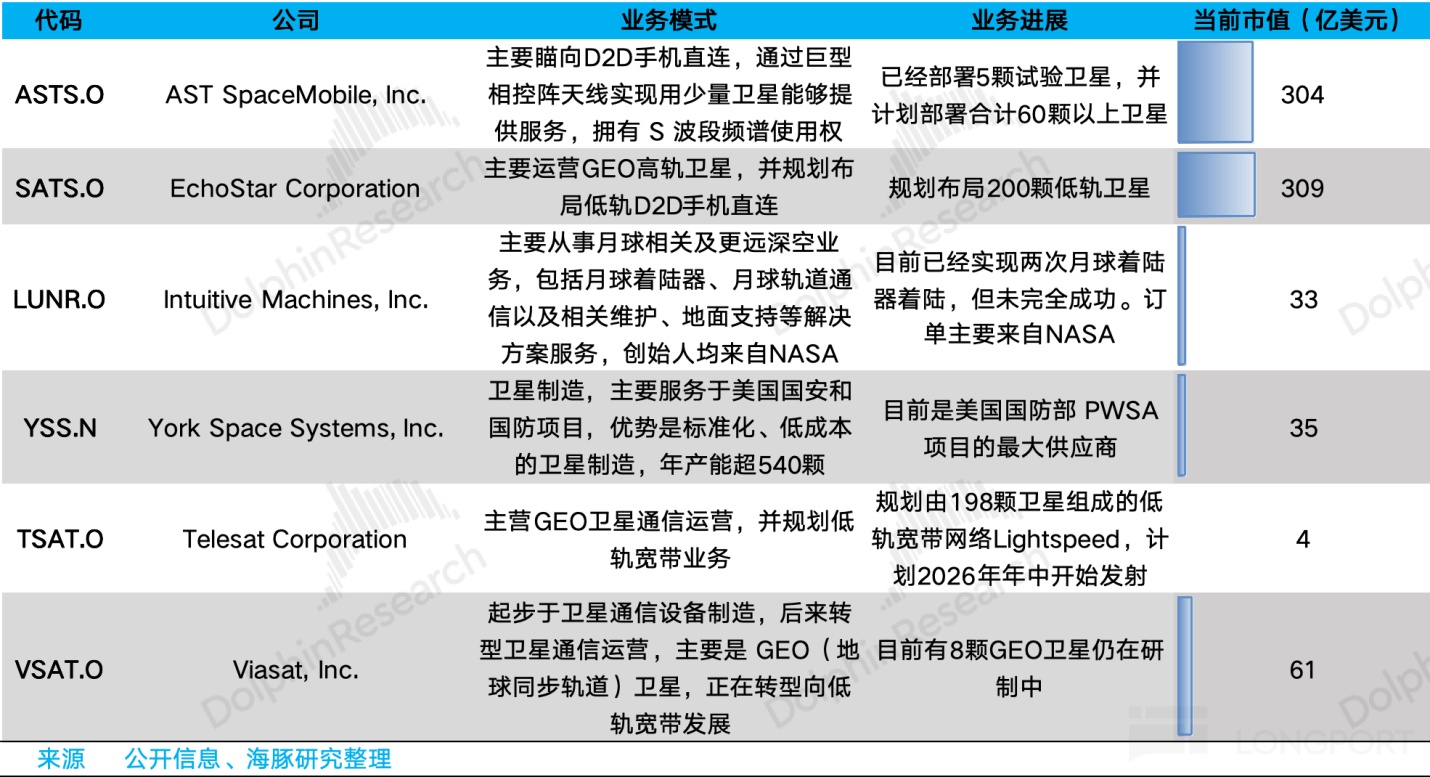

2) Constellation operators

We rank satellite ops behind launch providers. For LEO operators under the SpaceX/Blue Origin overhang, the key is differentiation on price, performance, and service. For traditional GEO operators, Starlink-class LEO poses a structural challenge, so watch their transition.

Key U.S.-listed satellite operators include:

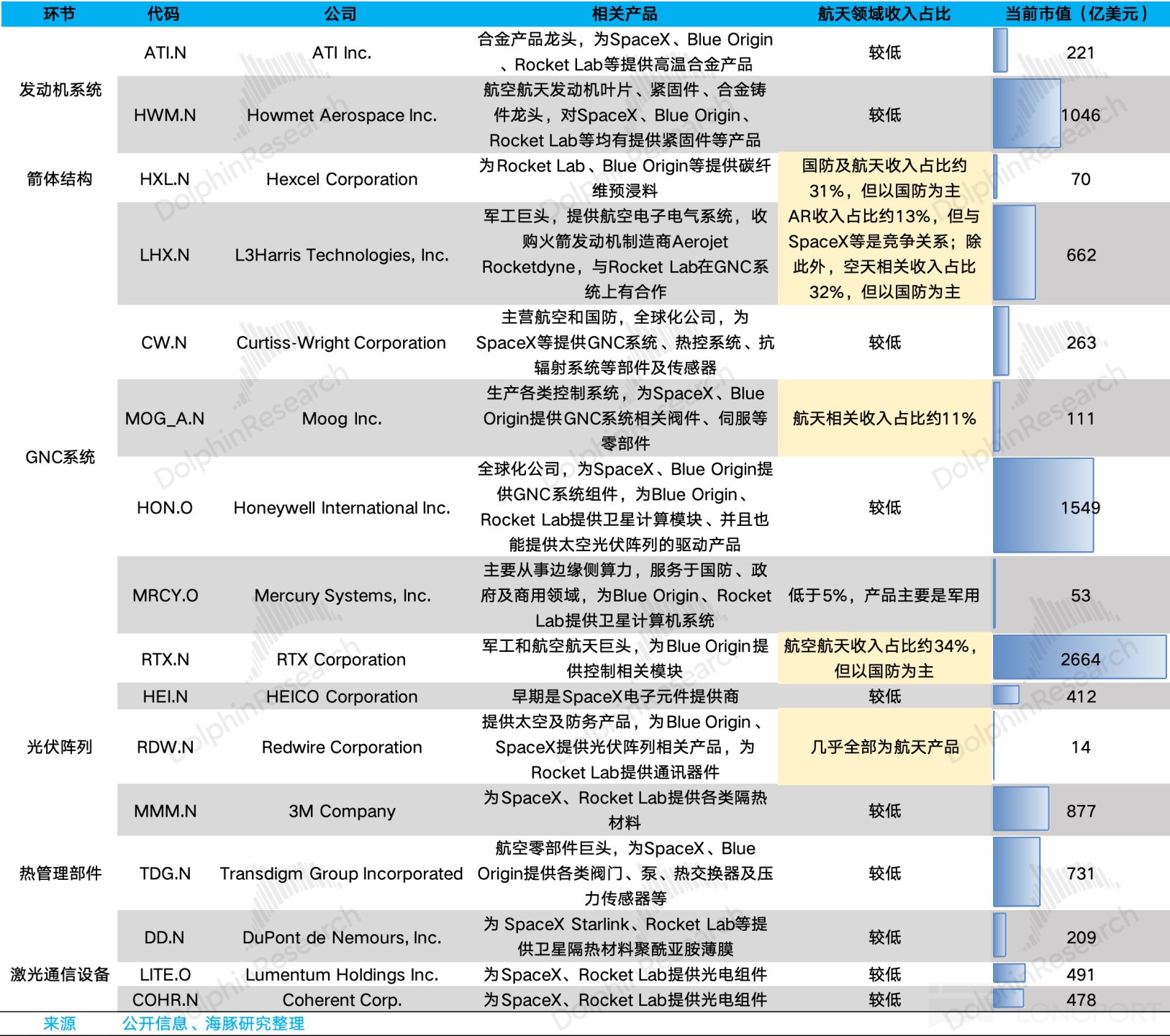

3) Upstream supply chain

Exploding demand creates upstream opportunities. Focus on two areas:

Core components tied to reusability and extreme cost-down: engines, structural materials, GNC, and AM (3D printing) techniques. SpaceX is highly vertically integrated; Blue Origin in-sources engines and structures; Rocket Lab internalizes engines, structures, GNC components, and some composites. External buys are mainly bulk materials and certain semis/electronics.

Surging satellite volumes and performance, especially compute satellites: these drive component demand faster than rockets, given lower per-launch costs under reuse. Typical examples:

Solar arrays: compute satellites may consume ~100 kW per spacecraft, ~4x Starlink commsats. Thermal management: higher power means more heat and complexity, lifting thermal subsystem value. Laser links: inter-satellite bandwidth is rising fast; Starlink is ~100 Gbps, ~5x GEO HTS, while compute satellites may need ~10 Tbps — orders of magnitude higher.

For arrays, SpaceX and Rocket Lab self-produce, though routes may shift, e.g., to silicon PV, implying potential external sourcing. For thermal parts, SpaceX sources materials and assemblies externally. For laser comms, SpaceX self-builds terminals, but chips, sensors, and modules rely on suppliers.

Across the U.S./EU, many suppliers sit within large conglomerates, are private, or unlisted. Independent pure-play listings are fewer after decades of industrial consolidation. Mega multinationals tend to dominate.

Some related U.S.-listed names are shown below:

In China, several listed firms play in upstream components and parts. Watch for potential HK listing opportunities.

Related tickers have been shared by Dolphin Research on the Longbridge app: https://longbridge.cn/sharelist/31528177?app_id=longbridge&utm_source=longbridge_app_share&locale=zh-CN&share_track_id=37d01a3d-7f74-40a3-802f-b2b6abcc1689&invite-code=032064

<End>

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.