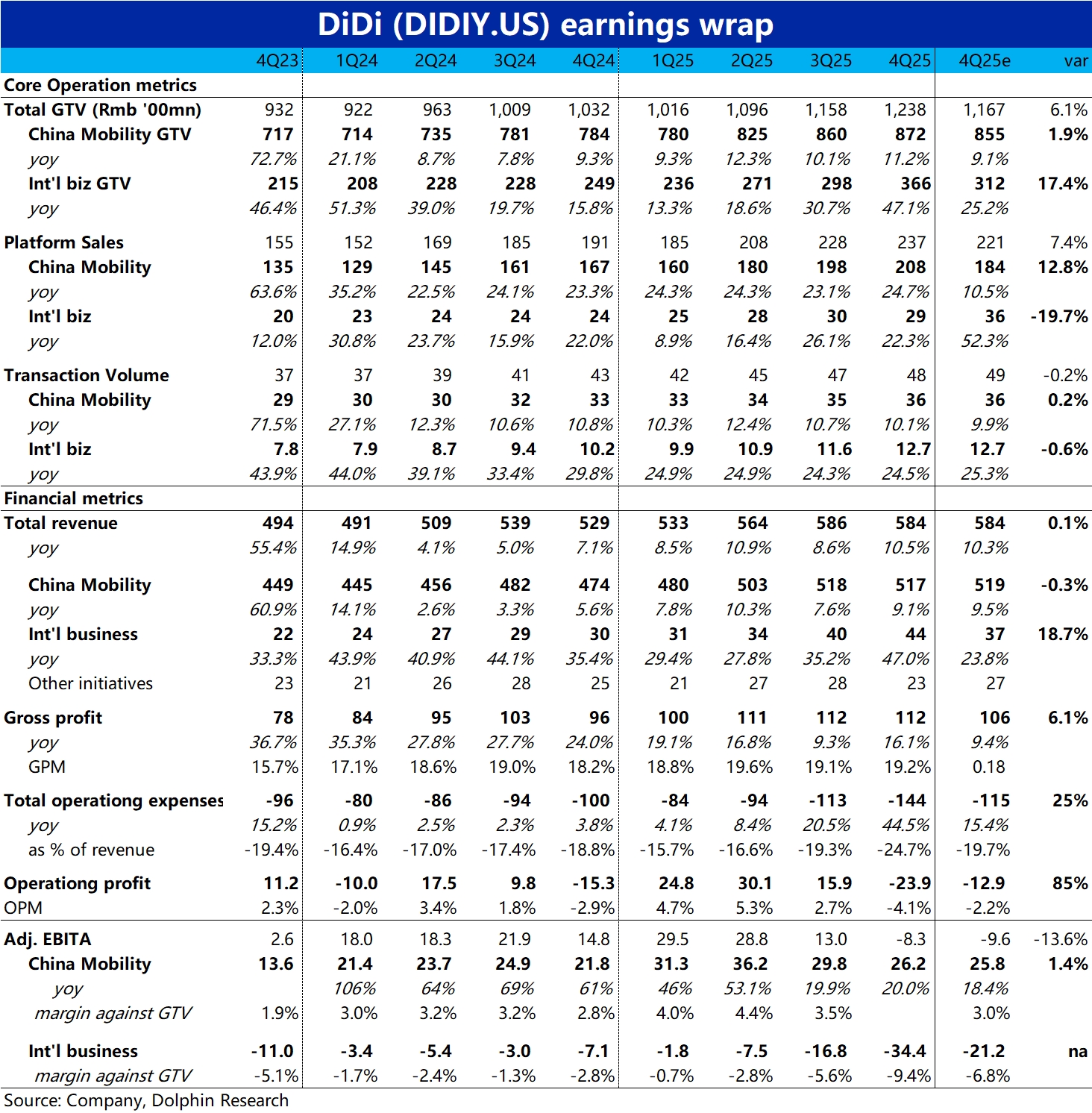

Didi 4Q25 First Take: While the market had anticipated wider losses in overseas ops, largely due to the Brazil food-delivery push, the actual loss came in far worse than expected, and shares have already fallen nearly 40% from the peak. Domestic ops remained solid. Details below:

1) Domestic ops: GTV rose Approx. 11% YoY, with a modest QoQ acceleration driven by higher ticket size. Domestic platform monetization continued to trend up, with reported take rate (Platform sales/GTV) at 23.9% vs. 23% last quarter.

Supported by this, domestic margin (adj. EBITA/GTV) improved to 3% vs. 2.8% YoY. Profit was Approx. RMB 2.6bn (+20% YoY), slightly ahead of Street estimates. The core domestic business remains steady, with balanced growth and incremental profit release.

2) The main issue lies in overseas ops, where losses widened sharply to RMB 3.4bn vs. RMB 1.7bn last quarter and market est. of RMB 2.1bn. The market was prepared for some pain, but the reality proved tougher. Specifically, overseas GTV growth jumped to 47% YoY, well above recent quarters and Street expectations.

However, Platform sales growth slowed QoQ to only 22%, underscoring that heavy investment and subsidies meaningfully lifted volume but did not translate into platform revenue. As scale grew, losses expanded.

3) On costs, total marketing expense surged to RMB 6.25bn vs. RMB 3.2bn YoY and RMB 4.7bn last quarter, the most notable increase among all cost lines and broadly in line with the incremental overseas loss. The loss was mainly driven by stepped-up overseas customer acquisition and consumer subsidies.

4) Overall, dragged by the RMB 3.0bn overseas deficit, other innovation businesses also posted a higher year-end loss of RMB 1.29bn, roughly in line with 4Q24's RMB 1.15bn, and the group swung to a net loss of RMB 0.8bn this quarter. Overspending remains a recurring issue for some China ADRs. $DiDi(DIDIY.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.