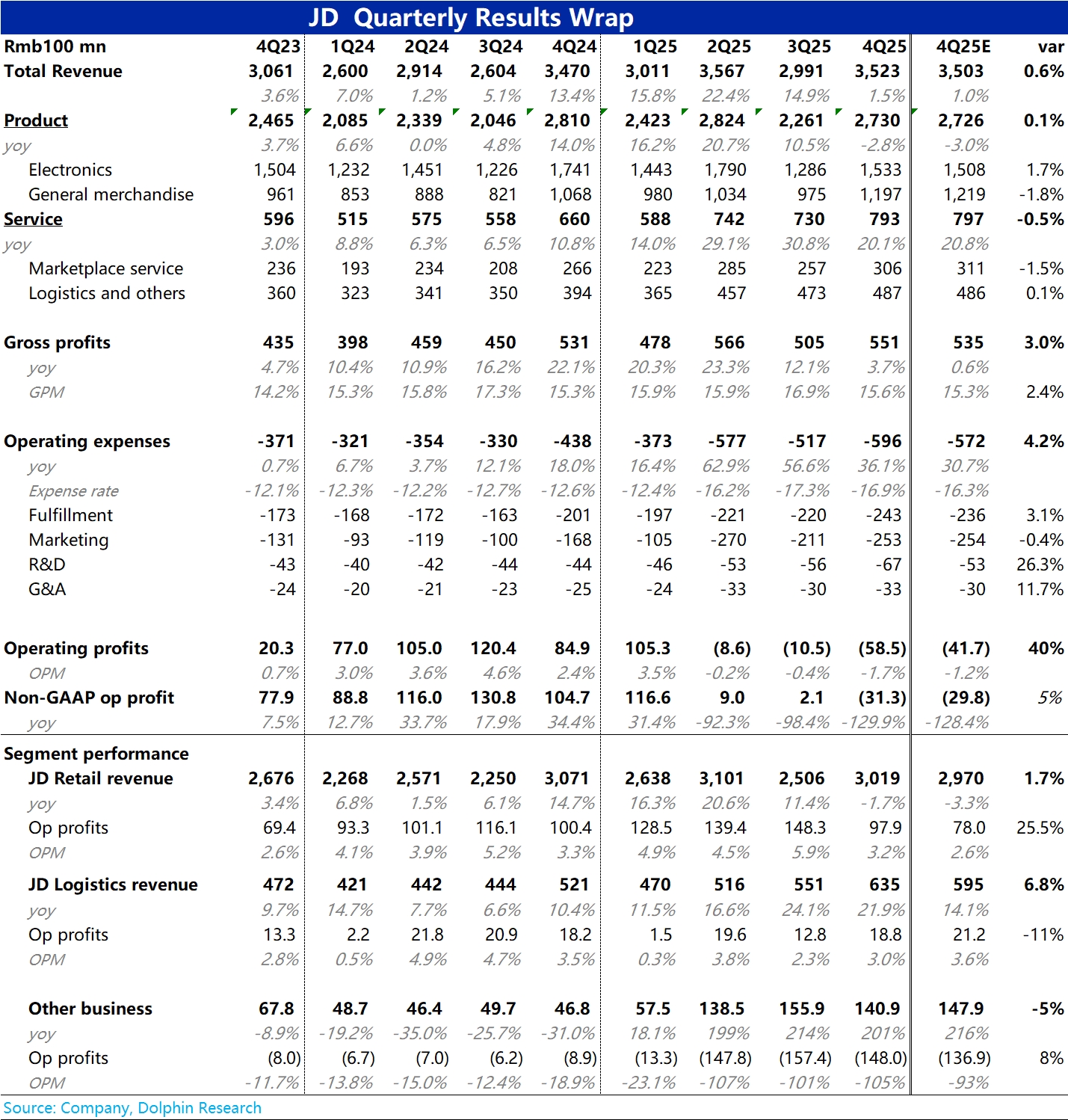

JD 4Q25 First Take. Overall, results were steady after broad estimate cuts by the market.

1) With state subsidies fading, group revenue growth slowed sharply to 1.5%, roughly in line with Bloomberg consensus at 1%. The main drag was a 12% YoY decline in electronics and appliances, broadly in line with market expectations.

General merchandise rose 12% YoY and services revenue grew 20% YoY, providing a cushion. Across business lines, top-line growth broadly matched sell-side expectations.

2) Profit was weaker both absolutely and relatively. Adj. OP swung to a loss of RMB 3.1bn, the first since 2017 and worse than the heavy food-delivery investment in 2Q–3Q. As state subsidies faded, Core Mall OP fell 2.5% YoY to RMB 9.8bn, down from RMB 13–15bn per quarter during the subsidy boom.

While food-delivery losses narrowed, rising investment in Jingxi and overseas pushed new businesses to a loss of RMB 14.8bn. The QoQ decline was limited.

Versus expectations, Core Mall profit beat, though slightly down YoY. Loss narrowing in new businesses lagged, likely due to ongoing food-delivery subsidies to sustain volumes despite low visibility, and possibly higher Intl spend. Please join the call for detail. $JD.com(JD.US) $JD-SW(09618.HK)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.