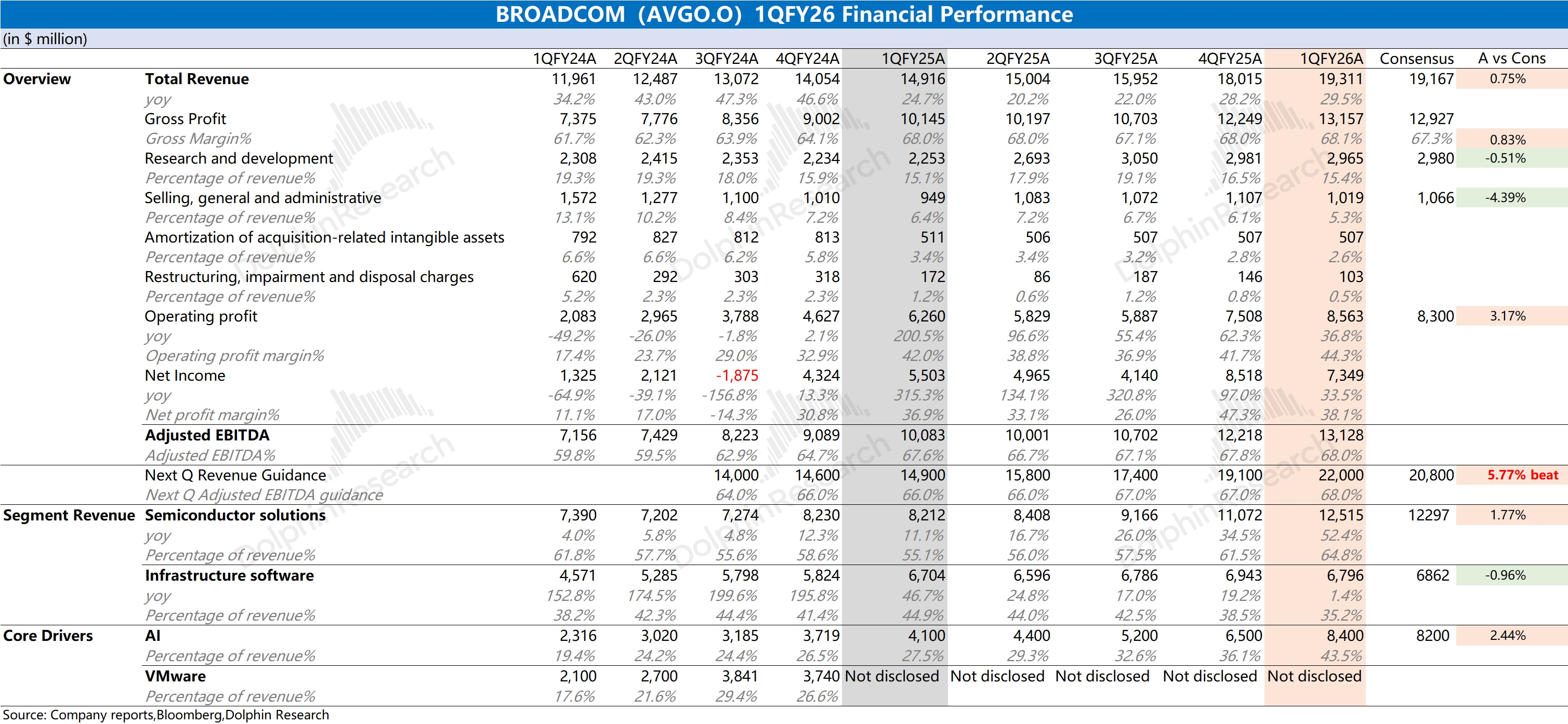

AVGO First Take: revenue and GPM met expectations this quarter. Top-line growth was driven by AI. On a business basis, GPM was 75.8% after excluding acquisition amortization and restructuring, ticking down QoQ on mix shift as lower-margin ASIC contributed more.

For next quarter, the company guides revenue to $22bn, up $2.7bn QoQ, above the Street (~$20.8bn). Growth again comes from AI.

1) Acquisition impact: Total Debt/LTM Adj. EBITDA fell to 2, back to pre-deal levels. The debt impact from the VMware acquisition has been absorbed within two years.

2) AI performance: AI revenue was $8.4bn this quarter, +$1.9bn QoQ. Mgmt guides AI revenue to $10.7bn next quarter, +$2.3bn QoQ, above the Street (~$9.7bn).

With AI as the main driver, AVGO is in an earnings upcycle. Coupled with capex outlooks at Google and Meta, rapid AI growth into 2026 looks highly visible.

Yet despite Big Tech raising capex, the stock has traded sideways, as the market questions sustainability. Meta's 2026 capex is projected to exceed half of annual revenue, leaving limited room to push higher.

AVGO and NVDA have recently seen strong results but multiple compression, and beyond beat-and-raise guidance, investors want clearer commitment from mgmt on sustained mid-to-long-term growth. For detailed follow-ups, please track Dolphin Research's upcoming commentary and Trans. $Broadcom(AVGO.US)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.