$XIAOMI-W(01810.HK)

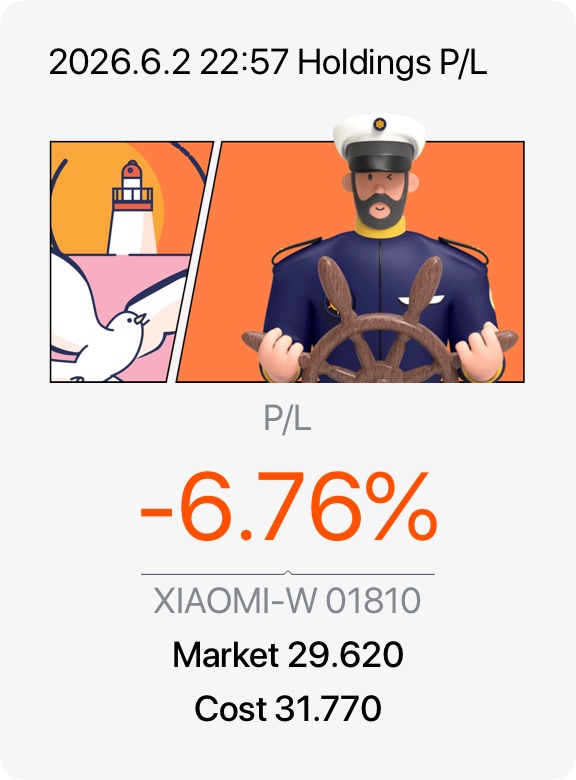

Xiaomi had a solid run today, closing up +3.13% at HKD 29.62. After a period of consolidation, the market seems to be pricing in the long-term potential of their EV segment and the record-high average selling price in their smartphone business.

The Latest Developments:

1️⃣ EV Momentum: Following the Q1 earnings, the Beijing factory has moved to a double-shift schedule to meet the massive demand for the SU7. The target? 100,000+ deliveries this year.

2️⃣ Premiumisation: Smartphone ASP hit a record high of RMB 1,310. It is proving that Xiaomi is no longer just a “budget” brand but a serious premium contender.

3️⃣ Analyst Outlook: Q1 2026 earnings saw some profit pressure due to EV R&D, many analysts are maintaining a “Buy” or “Outperform” rating. They eyeing a breakout above the $32–$35 range as EV deliveries scale.

As a shareholder (1,200 shares strong!), I am watching the $30 resistance level closely. The bridge between tech and transport is looking sturdier than ever. 🚗📱 加油😉。

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.