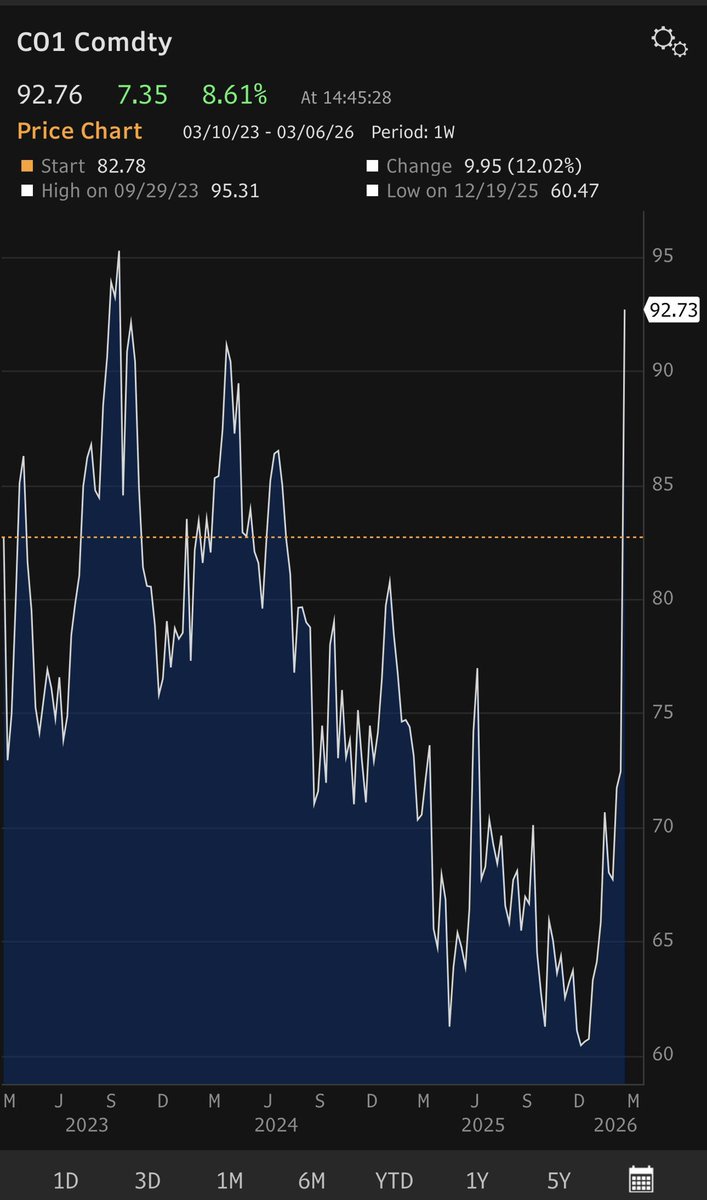

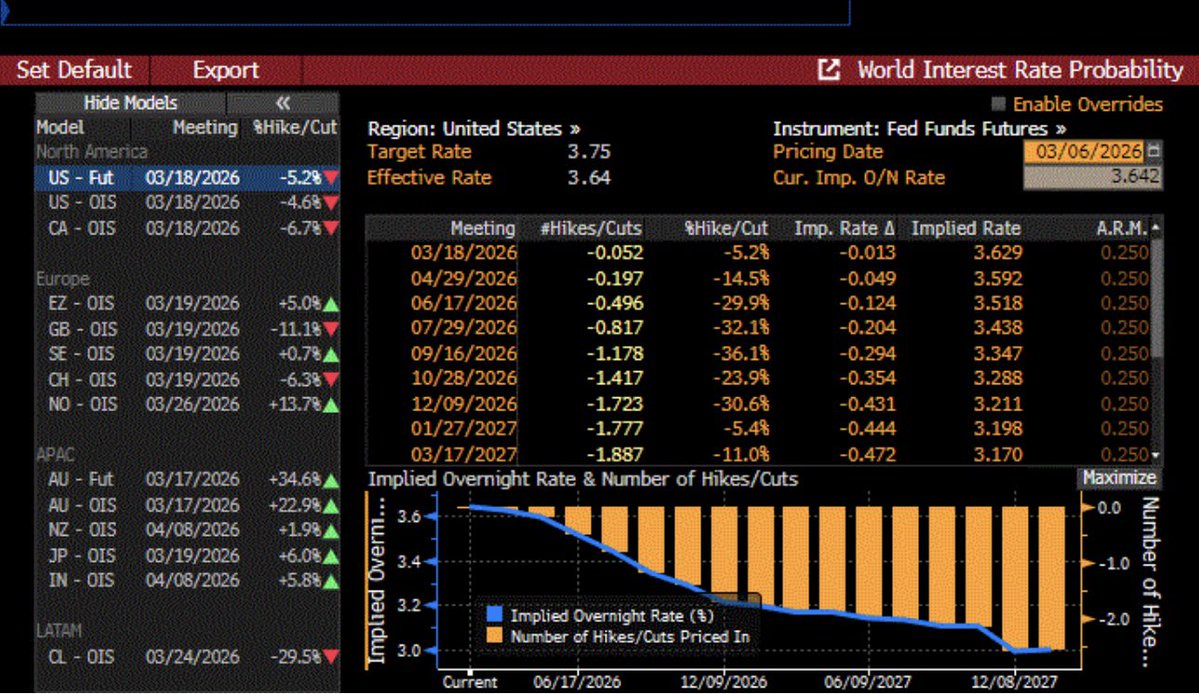

Today’s weak Feb jobs report (-92K vs +55K exp) punished stocks at a time when a widening war in the Middle East is lifting oil prices (brent crude +8% today to $92.45/bbl) and fueling inflation concerns. Renewed anxiety about the private-credit industry also curbed risk appetite. 10yr treasury yields fell and gold and silver prices rose. Reflecting investors’ declining risk appetite, #bitcoin sank -4%. Money markets are again discounting two Fed rate cuts this year, starting in June.

The Fed’s biggest fear has always been having to choose between fighting inflation and growing jobs. Friday’s employment report brought that confrontation one step closer. Significant weakening in the labor market would support a rate cut, but given the risk that higher-for-longer oil prices could trigger another inflation surge, the Fed may feel compelled to remain on the sidelines. We believe declining interest rates will outweigh any market decline due to the temporary surge in inflation caused by the fighting in the Middle East. To that end, we continue to see equities reclaiming new highs once the Middle East conflict ends, with oil prices likely to retreat and employment growth slowing, increasing odds of quicker Fed rate cuts. Analysts are forecasting 2026 S&P 500 earnings of $310 vs 2025 S&P 500 earnings of $275, which implies an S&P 500 2026 P/E of 22.2x, equal to a 4.5% earnings yield and a ~40bp premium to 10-year treasury yields, in line with historic spreads in non-recessionary periods.

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.