Is the US economy approaching a "soft landing"? The bearish voices of Morgan Stanley and Goldman Sachs are gradually fading.

得益于通胀数据下滑,促使摩根大通首席全球市场策略师 Marko Kolanovic 软化了他对美国可能出现衰退的看法。

智通财经 APP 获悉,得益于通胀数据下滑,促使摩根大通首席全球市场策略师 Marko Kolanovic 软化了他对美国可能出现衰退的看法。Kolanovic 曾警告投资者在经济风险逼近之际避开股市。他表示,6 月份消费者价格指数 (CPI) 略微增加了美联储实现 “软着陆” 的可能性——即在不引发经济衰退的情况下遏制通胀。

他在周一给客户的一份报告中写道:“尽管我们仍预计美联储将在 7 月会议上加息,但 CPI 意外下跌意味着通往软着陆的狭窄道路将略微拓宽。”

在 2022 年市场抛售的大部分时间里,科拉诺维奇是华尔街最大的乐观主义者之一,但由于经济前景恶化,他在去年 12 月中旬、今年 1 月、3 月和 5 月削减了摩根大通的模型股票配置。

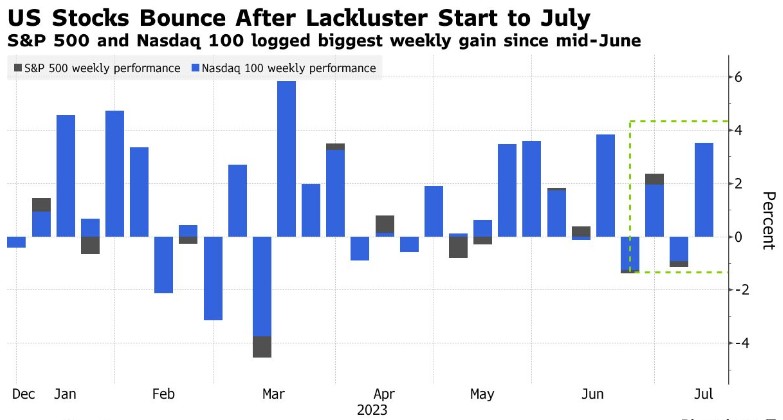

与此同时,投资者普遍降低了对美国经济衰退的预期。花旗集团策略师 Chris Montagu 指出,资金流数据似乎显示,交易员押注美国经济将软着陆,在一系列积极的经济数据公布后,他们上周加大了对标普 500 指数的看涨押注。

尽管 Kolanovic 表示,他的公司正在淡化近期经济衰退的风险,但摩根大通仍对通胀能否在经济不下滑的情况下持续回到央行的舒适区间表示怀疑。与此同时,他说,如果通货膨胀率降至 2.5%,利率开始下降,美国中小型股可能会有 “相当大的上行空间”。

此外,Kolonavic 警告称,欧洲股市下半年将面临进一步收紧货币政策、债券收益率走低以及可能令人失望的财报等风险,表现将逊于美国股市。

“这次倒挂不一样!”,高盛下调美国经济衰退概率

摩根大通的观点与高盛不谋而合。尽管美国国债收益率曲线的大幅倒挂引发了对经济衰退前景的焦虑,但在上周低于预期的通胀报告出炉后,高盛集团也进一步将美国经济衰退的可能性从 25% 下调至 20%。该行首席经济学家 Jan Hatzius 周一在一份报告中写道:“我们不认同对收益率曲线倒挂的普遍担忧。”

Hatzius 反对大多预测者的观点——他们指出,曲线倒挂在预测经济衰退方面有着几乎无可挑剔的记录。在美国过去 7 次衰退之前,3 个月期美国国债收益率每次都高于 10 年期美国国债。目前,3 年期美债利率较 10 年期美债利率高 150 个基点,接近 40 年来最深倒挂水平。

通常情况下,收益率曲线是向上倾斜的,因为投资者持有长期债券比持有短期债券要求更高的风险补偿或期限溢价。Hatzius 解释称,当收益率曲线倒挂时,意味着投资者正在消化降息幅度大到足以压过期限溢价的预期,这种现象只有在衰退风险变得"清晰可见"时才会发生。

不过,这位经济学家说,这一次情况有所不同。这是因为期限溢价 “远低于” 其长期平均水平,因此仅需要更少的预期降息来使得曲线倒挂。此外,根据 Hatzius 的说法,随着通胀降温,它为美联储在不引发经济衰退的情况下放松利率开辟了 “一条合理的道路”。

Hatzius 补充说,当经济预测变得过于悲观时,它们对长期利率的下行压力就会超出合理范围。他写道:“因此,认为倒挂曲线证实了经济衰退的普遍预测的观点,至少可以说是循环论证的。”