Why is high interest rate still unable to suppress employment? Will the Federal Reserve take tough measures? It all depends on tonight's non-farm payroll report.

6 月裁员放缓、劳动力囤积现象仍在,今夜非农可能再迎 “惊吓”。

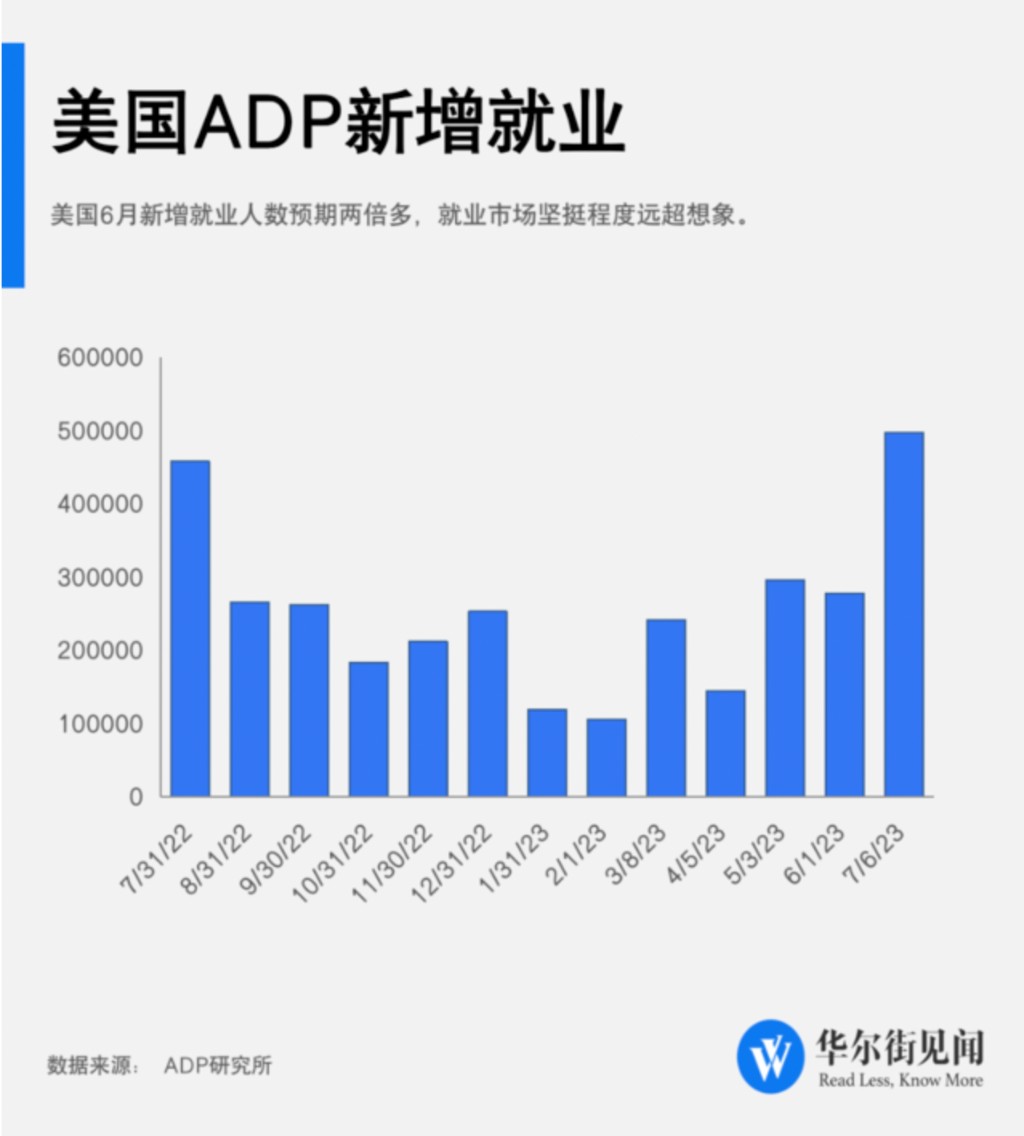

美国就业又双叒叕超预期,数据偏离幅度令人大跌眼睛。

周四最新发布的 “小非农” ADP 报告显示,6 月美国新增就业人数 49.7 万,为市场预期 22.5 万人的两倍多,远超前值 27.8 万,创下 2022 年 7 月以来最大月增幅。

这一数据凸显劳动力市场继续高烧不退,并引爆激进加息预期,隔夜美股市场又见 “股债双杀”。

为何 ADP 大超预期?为何高利率难为就业降温?今夜非农是惊喜还是惊吓?

ADP 为何远超预期?

分析指出,ADP 远超预期可能有三点,6 月裁员放缓、劳动力囤积现象仍在,也有可能是之前的就业放缓才是 “插曲”。

1、6 月裁员人数下降

在过去的几个月里,美国科技行业掀起大规模的裁员潮,而如今这一趋势正在放缓。

根据招聘公司 Challenger, Gray & Christmas 周四上午公布的数据,美国雇主在 6 月份宣布裁员 40709 人,为 2022 年 10 月以来的最低月度数据。

尽管如此,今年上半年宣布的 458209 个裁员总数仍是 2009 年以来 1 月至 6 月的最高数据,不包括 2020 年,当时宣布了 896675 个裁员,技术行业继续占到裁员的绝大部分。

Challenger, Gray & Christmas 的高级副总裁 Andy Challenger 在一份声明中说:

裁员人数的下降在夏季来说并不罕见,事实上,6 月是史上宣布裁员最慢的月份,也有可能一句通胀和利率而预测的深度失业不会发生,特别是在美联储暂停加息的情况下。

2、失业率升高才是 “意外的小插曲”?

美国的失业率在 5 月份激增,从 3.4% 跃升至 3.7%。失业率的突然和急剧上升在很大程度上是出乎意料的,特别是考虑到强劲的就业增长。

月度非农报告由两项调查组成,以衡量就业水平和活动:一项是调查企业的就业、工时和收入情况;另一项是调查家庭,以获得人口的劳动力状况和人口统计细节。失业率来自于后者,由于样本量较小,通常被认为是不稳定的。

Glassdoor 的首席经济学家 Aaron Terrazas 在上周发表的评论中指出:

随着最近的大学毕业生进入就业市场,以及最近被解雇的工人的再就业速度放缓,6 月份的失业率可能上升到 3.9%。

3、劳动力囤积和软着陆

最近的就业市场数据显示,尽管需求疲软,但更多的企业正在囤积劳动力,维持员工人数。造成这种情况的部分原因是在疫情期间经历了严重的工人短缺,以及婴儿潮一代退出劳动力市场等更广泛的人口结构变化。

Wells Fargo 高级经济学家 Sarah House 指出:

鉴于此,我们确实认为企业将更不愿意让工人离开,这有助于经济能够实现软着陆的论点,在没有大量就业损失或引发经济衰退的情况下降低通胀。

为何高利率依旧难压就业?

为什么自 20 世纪 80 年代以来最激进的加息,也没有成功地将通胀率降至 2% 目标,为就业市场降温?

答案是高利率可能没有击中通胀的痛点。牛津经济研究院经济学家 Tomas Dvorak 认为,加息的影响只部分集中在推动基本通胀的部门。

众所周知,利率制定者在冷却商品价格方面几乎无能为力,而商品价格一直是通胀的主要驱动力,这使得美联储对受全球定价影响的经济活动,如农业和公用事业,控制不足。

相反,Dvorak 的估计显示,首当其冲的是制造业,在货币政策影响的峰值点,利率每增加一个百分点,其产出就会下降 0.23%。但制造业就业已经有所降温。而服务行业,如酒店业,价格上涨得更快,因为利率的冲击并不明显。

一些经济学家认为,很大的问题在于,在过去 40 年里,西方经济向服务业的巨大转变使货币政策失去了影响。根据传统理论,汽车制造商等耐用品生产商通过其持有大量库存的动机,尤其能感受到更高的利率。

美联储已经承认,服务业通胀可能需要更长的时间才能得到控制。作为对粘性通货膨胀的另一种解释,美联储研究表明,政策需要 18 至 24 个月才能在整个经济中产生影响。但如果这是真的,美联储就不应该以最新的通胀数字作为决策依据,鹰派官员最近表示滞后期已经缩短。

今夜非农将再迎冲击?

美国公司 6 月份的招聘活动出现了大规模的、意想不到的高峰,今夜将公布的重磅非农就业报告有可能也体现劳动力市场持续强韧。

分析预期,非农几乎肯定会显示美国劳动力市场连续 30 个月增加就业。

虽然目前的就业增长与 2010 年至 2019 年期间的劳动力市场扩张相形见绌,当时有创纪录的 100 个月的就业增长,但目前这种连续的增长偏离预期,高于平均水平的增长是在通胀放缓、美联储大幅加息的情况下出现的。

劳工统计局的数据显示,今年迄今为止新增的 157 万个工作岗位,是 1939 年以来 1 月至 5 月有记录以来第十大数据,今年每月平均 31.4 万个新增就业远远超过了疫情前的水平。

尽管如此,一些经济学家认为,劳动力市场增长终将放缓,这只是一个时间问题。经济学家预计,6 月份非农将低于这一平均水平,也低于 5 月份增加的 33.9 万个就业岗位。根据路透社的数据,经济学家的普遍预期是新增 22.5 万个工作岗位,然而构成这一共识的 82 位经济学家的预测差别很大,介于 11 万到 28.8 万个工作岗位;失业率预计将从 3.7% 下降到 3.6%,预期范围从 3.4% 到 3.8% 之间。