Severely Underweight Positions, Failing to Keep Pace with US Stock Rally, Hedge Funds Engage in 'Panic Buying'

The S&P 500 broke through 7,000 points to set a new all-time high, leaving hedge funds in an awkward position—positions lagged behind the market, and the long-short ratio even fell below levels seen during the panic selling of 'Tariff Day'. Institutions with insufficient positions were forced to blindly chase the rally, directly triggering the largest single-day call option volume of the year. While CTA strategies have turned net long, their exposure remains at only the 31st percentile historically, leaving ample room for further additions

The strong rebound of US stocks to historic highs has left many hedge funds in an awkward predicament—severely underweight positions that lagged the market, forcing them into panic buying.

The S&P 500 recently broke through 7,000 points to set a new all-time high, with core thematic sectors such as AI, semiconductors, and technology hardware generally recovering to and surpassing pre-conflict levels. However, according to Conor Lyons, a trader at UBS, in his latest report, although performance data suggests hedge funds participated in this repricing, overall position data shows that net exposure did not keep pace.

This mismatch is forcing hedge funds to chase the rally almost blindly, directly driving recent abnormal activity in the options market—yesterday (April 15) recorded the largest single-day call option volume since 2026.

The head of Goldman Sachs' Delta-One business holds a similar view: current capital flows are unidirectional, with CTAs, clients, and various participants generally underweight and competing to buy the rally. This structure has formed an effective short gamma scenario on the upside, further reinforcing the market's continued upward momentum.

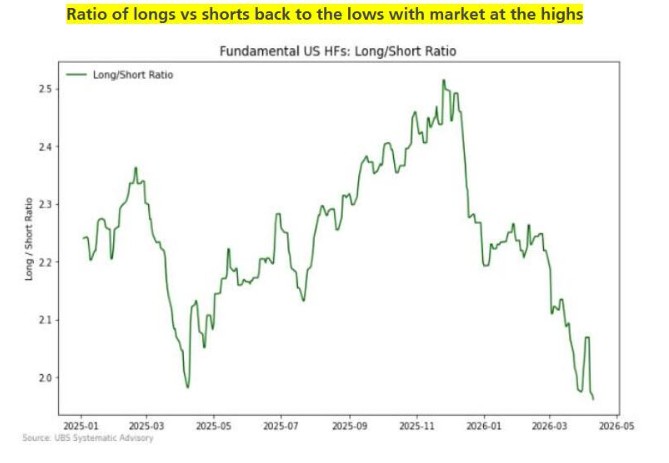

Hedge Fund Positions Lag, Long-Short Ratio Drops to Lows

UBS data shows that last week saw the largest weekly net sell-off by hedge funds since 2026, driven by both active reduction of long positions and the addition of new shorts. Long reductions were concentrated in the US technology hardware sector, while new shorts primarily targeted the US software sector.

More notably, the current hedge fund long-short ratio remains below the peak levels seen during the panic selling of 'Tariff Day', when the stock market was far from its current height. This means that with the S&P 500 having recovered to historic highs, the overall net exposure of hedge funds remains relatively low, with total positions showing only a slight overweight bias.

Retail investors also failed to keep pace with this rebound. UBS data shows that retail outflows last week also hit the highest level of the year, with supply heavily concentrated in the semiconductor sector. The current operating mode for retail investors is to reduce positions on price increases rather than buy on dips—even though the market has almost ceased providing obvious pullback buying opportunities.

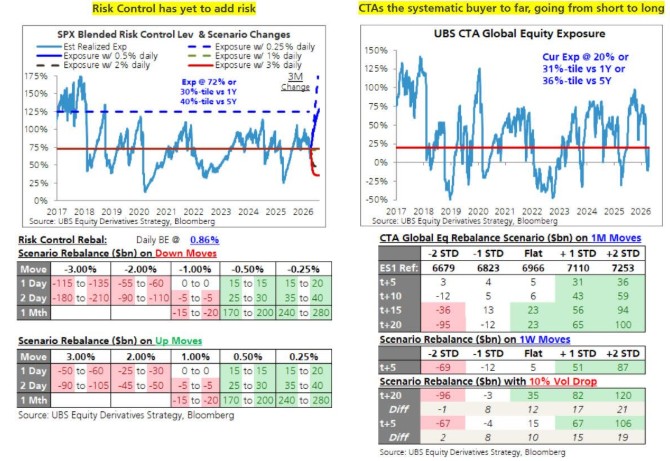

CTA Turns Net Long, But Room for Further Addition Remains Large

In the systematic strategy camp, Commodity Trading Advisors (CTA) were the primary buying force in this rebound. According to UBS reports, CTAs have shifted from net short to net long since last week, but current exposure remains at only the 31st percentile historically, meaning that if the market continues to rise, CTAs still have significant room for adding positions.

Risk Control strategies have not yet become effective buyers, constrained by recently elevated realized volatility, with their exposure remaining roughly flat quarter-over-quarter. However, UBS estimates that if the S&P 500 stabilizes in the future and daily volatility narrows to within plus or minus 50 basis points, Risk Control strategies could purchase approximately $185 billion over the next month.

The head of Goldman Sachs' Delta-One business pointed out that the current position structure effectively creates a short gamma effect on the upside, continuously reinforcing the market's upward inertia. He also noted that at the index level, the S&P 500's gamma is actually in a relatively bullish state, which helps suppress volatility while the market continues to rise. However, he also stated that he does not agree with the current logic of chasing the rally, but fully respects the reality that technical momentum may persist.

Structural changes in the options market warrant caution. Options analytics firm SpotGamma notes that with the expiration of VIX options today (April 15), the positive gamma protection previously accumulated in the market has largely dissipated, leading to expanded exposure to bidirectional volatility.

SpotGamma places the key pivot point for the S&P 500 near 6,900 points, with resistance levels at 7,000 and 7,020 points above, and support around 6,800 points below. The dissipation of positive gamma means that the options hedging mechanisms that previously helped suppress volatility and smooth the upward trend have significantly weakened, opening up volatility space in both directions.

Earnings Season Becomes Key Test Ahead

UBS concludes in its report that the current position landscape indicates that, absent major geopolitical risk shocks, the path of least resistance for the stock market remains upward. However, earnings season will be a critical hurdle in the short term.

The options market currently prices an average single-earnings move for the S&P 500 this quarter at 5.3%, slightly above historical averages for this period. Among these, implied volatility premiums are most prominent for the technology, industrial, and materials sectors, indicating the market assigns the highest uncertainty pricing to earnings results in these sectors.

For investors, the core contradiction in the current market is: institutions with insufficient positions are forced to chase the rally, pushing the market higher; however, as gamma protection weakens and earnings season approaches, the market's ability to buffer against negative shocks is simultaneously declining.