A Thirty-Year Supercycle for Storage Chips? UBS: In an Oligopoly of Three, DRAM Will Remain in Short Supply Until the End of 2027

Driven by AI-induced HBM demand growth coupled with a traditional server replacement cycle, UBS believes the global DRAM market's supply-demand gap will persist until the fourth quarter of 2027. The DRAM market has highly consolidated into an oligopoly of three players, leading to a lack of sufficient "competitive capacity expansion" on the supply side to smooth out demand shocks, thus prolonging upward price pressure

A Once-in-Thirty-Years Storage Chip Supercycle? UBS: In an Oligopoly of Three, DRAM Will Remain in Short Supply Until Late 2027

The storage chip industry is at a rare historical inflection point.

According to Windmill Trading Desk, UBS's latest research report suggests that AI-driven HBM demand continues to encroach on DDR capacity, combined with a synchronized surge in traditional server replacement cycles and SSD demand, the global DRAM market's supply-demand gap will persist until the fourth quarter of 2027, marking a storage supercycle not seen in nearly three decades.

Concurrently, the DRAM market has highly consolidated into the current three-player oligopoly. The supply side lacks sufficient "competitive capacity expansion" momentum to mitigate demand shocks, reducing the intensity of cyclical corrections, while the upward price pressure from this demand supercycle will be more prolonged.

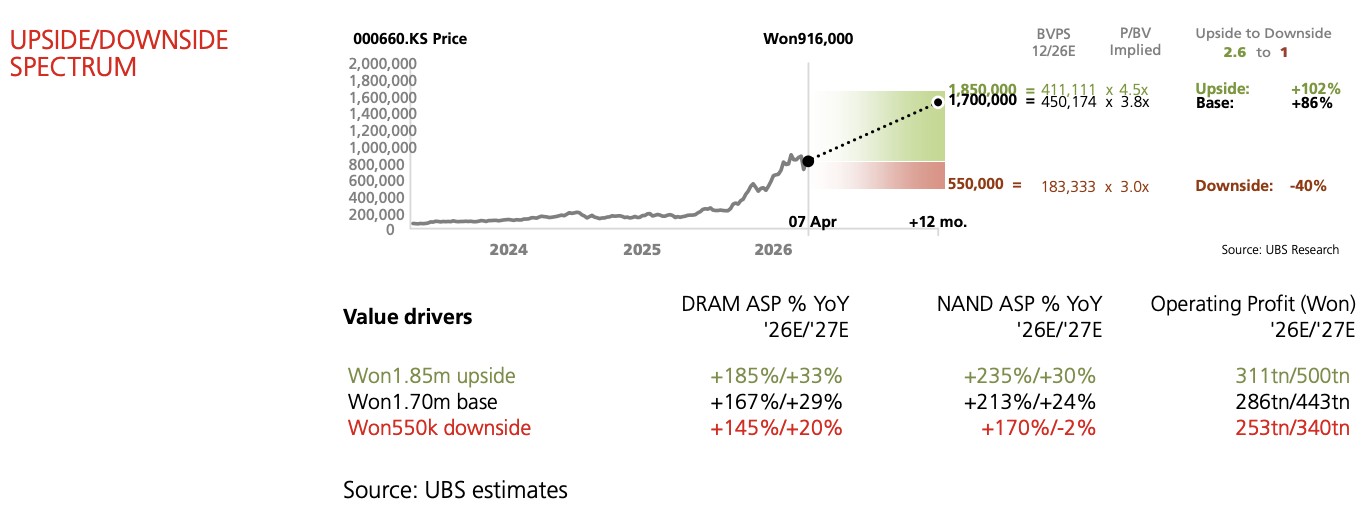

SK Hynix holds a leading position in the HBM field. UBS has raised its 12-month target price from KRW 1.55 million to KRW 1.70 million and significantly increased earnings forecasts: earnings per share for 2026 and 2027 are raised by 22% and 29% respectively, with operating profit forecast for 2026 reaching KRW 286 trillion, approximately 57% higher than market consensus.

Regarding recent catalysts, SK Hynix's ADR listing may be accompanied by a share buyback program in the Korean market, creating a "double positive" – it will both enhance the convenience of offshore investor allocation and directly support stock prices in the Korean market.

A Once-in-Thirty-Years Phenomenon: The Underlying Logic of the DRAM Shortage Cycle

This storage chip cycle is historically rare, "once in thirty years," driven by the synergistic resonance of multiple demand-side shocks.

Firstly, the explosive growth in HBM demand is continuously crowding out traditional DDR capacity. By the end of 2026, global front-end HBM-exclusive DRAM capacity will reach 500,000 wafers per month (equivalent to 12-inch wafers), accounting for 25% of the industry's total capacity; by 2027, this proportion will be around 31%.

Secondly, a traditional server replacement cycle is simultaneously underway, with sustained demand for conventional DRAM such as DDR5. Meanwhile, the expansion of AI infrastructure is also driving incremental demand for servers and storage SSDs.

Thirdly, capacity expansion outside of China is almost entirely focused on HBM, with extremely limited new supply for conventional DRAM. The three major suppliers (SK Hynix, Samsung, Micron) have significantly constrained willingness to expand capacity in non-HBM areas.

The DRAM market has highly consolidated into the current three-player oligopoly. The supply side lacks sufficient "competitive capacity expansion" momentum to mitigate demand shocks, reducing the intensity of cyclical corrections, while the upward price pressure from this demand supercycle will be more prolonged.

SK Hynix's HBM Leadership: Short-Term Disturbances Do Not Alter the Long-Term Landscape

Recent market concerns about SK Hynix stem from two specific issues: the partial redesign of HBM4 products and HBM shipment volumes. Neither poses a fundamental threat to its industry position.

Regarding the HBM4 redesign, SK Hynix is nearing completion of minor redesign work for logic chips and DRAM dies, and is actively advancing the final certification process for Nvidia's Rubin platform. Based on this, SK Hynix's market share assumption for the HBM4/Rubin platform is adjusted to 60%, with Samsung at 30% and Micron at 10%.

In terms of shipment volumes, SK Hynix is expected to ship 18.4 billion Gb of HBM bits in 2026 (a 46% year-on-year increase) and 24.7 billion Gb in 2027 (a 34% year-on-year increase). In terms of industry bit share, SK Hynix is projected to maintain its leading position in the HBM market for two consecutive years, with shares of 51% and 44% respectively.

SK Hynix's technical accumulation and customer trust built over several years in HBM execution are the core barriers to its continued leadership. This HBM4 design adjustment is a localized optimization, not a directional reversal.

Earnings Significantly Exceed Market Expectations: Significant Room for Valuation Repair

Based on the aforementioned judgments, UBS's earnings forecasts for SK Hynix far exceed market consensus, with a striking magnitude of difference.

On the revenue front, total revenue is forecast to be KRW 355.1 trillion in 2026 (market expectation KRW 251.6 trillion, about 41% higher), and forecast for 2027 is KRW 531.6 trillion (market expectation KRW 323 trillion, about 65% higher).

In terms of operating profit, it is forecast to be KRW 286 trillion in 2026 (market expectation KRW 182 trillion, exceeding by about 57%), and KRW 443.5 trillion in 2027 (market expectation KRW 235.6 trillion, exceeding by about 88%).

Specifically for the first quarter, operating profit for Q1 2026 is forecast at KRW 41.76 trillion, significantly higher than the market consensus of KRW 32.2 trillion.

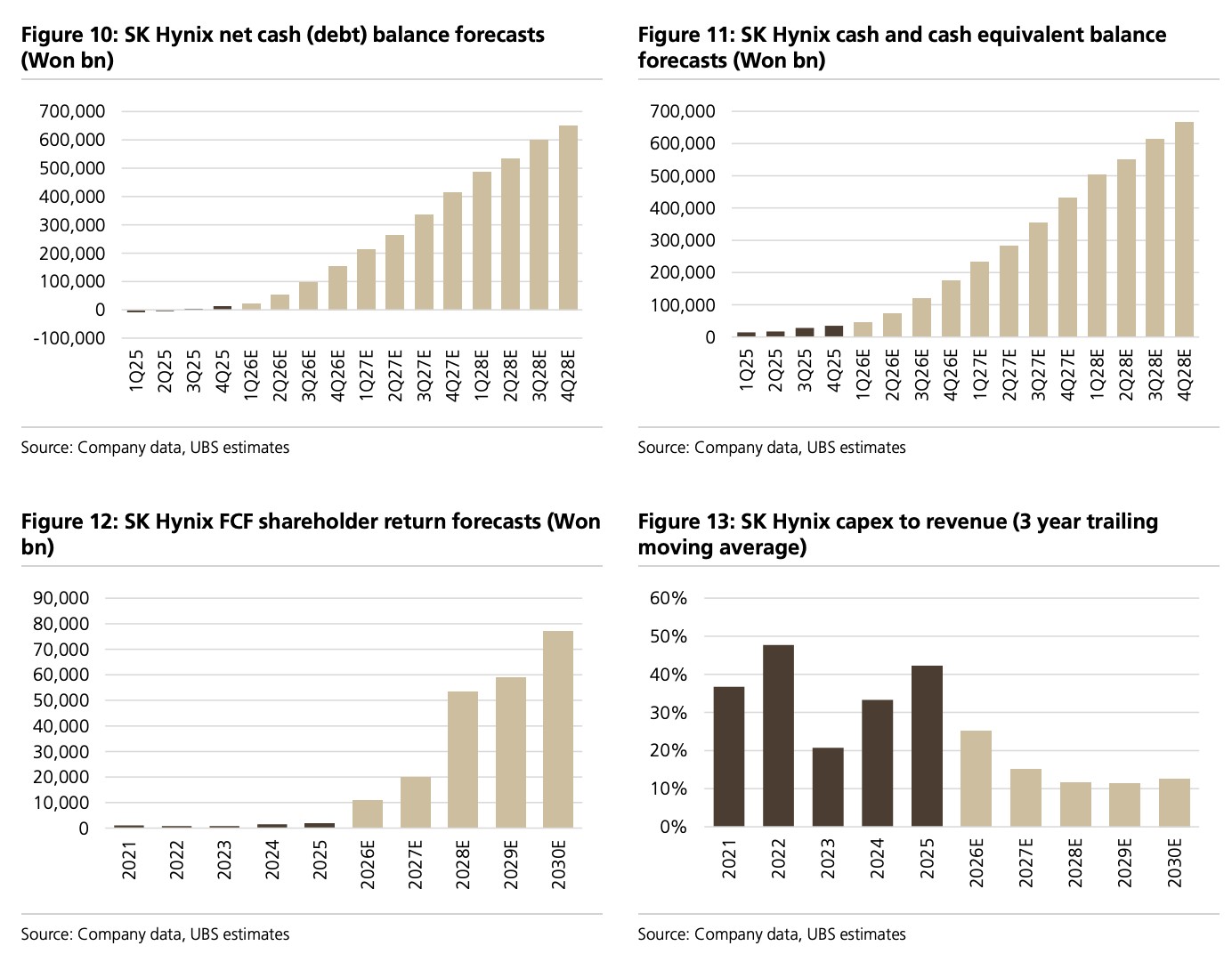

On the cash flow front, free cash flow is expected to be KRW 143.8 trillion in 2026 and further jump to KRW 269.8 trillion in 2027, corresponding to free cash flow yields of approximately 21.6% and 40.5% respectively.

Valuation and Catalysts: ADR Listing and Share Buybacks Provide Dual Support

Using a 12-month forward price-to-book (P/B) multiple valuation method for SK Hynix, based on its long-term ROE forecast of 32.1% and a cost of equity of 11.2%, a target P/B multiple of 2.86x is derived, corresponding to a target price of KRW 1.70 million.

The current NTM P/B multiple of 1.54x implies a long-term ROE of only 17.3%, which is not only lower than the historical average of 21% over the past decade but also significantly lower than UBS's forecast of 32.1%.

This valuation gap implies that the market has not fully priced in SK Hynix's higher DRAM profitability and its strong free cash flow generation capabilities.

Regarding recent catalysts, the ADR listing may be accompanied by a share buyback program in the Korean market, creating a "double positive" – it will both enhance the convenience of offshore investor allocation and directly support stock prices in the Korean market.

The UBS research team believes that around April 24, 2026 (approximately at the time of the first-quarter earnings release), positive catalysts exist, including smartphone sales data, pricing negotiation outcomes, and GPU supply chain dynamics.