U.S. stocks surge on March's closing day, analysts say "this rally is not to be trusted"

U.S. stocks rebounded strongly at the end of March, with the Dow Jones Industrial Average surging 1125 points in a single day, but analysts cautioned that it is "not to be trusted." "Today's market perfectly illustrates the current volatile market environment – everything can reverse in an instant." Brent crude oil soared 63.3% in a single month, the largest monthly increase in 35 years, and market anxiety has shifted from inflation to growth. If high oil prices impact corporate profits, this rebound may be vulnerable

U.S. stocks staged a strong rebound on the last trading day of March, but analysts warned that the rally may not be worth chasing.

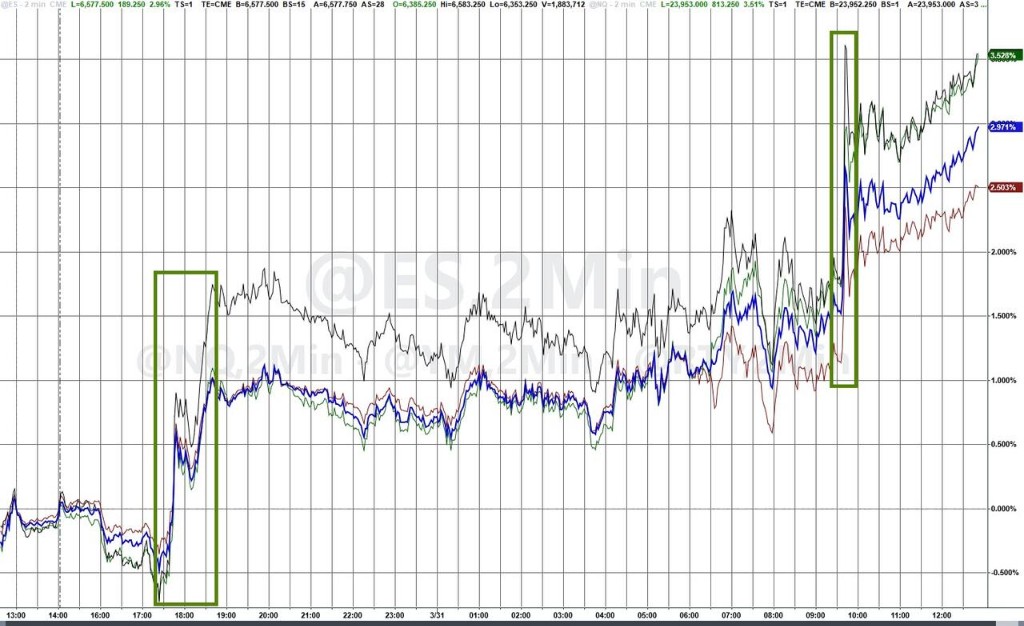

On Tuesday, boosted by news that the Trump administration might seek to end the military conflict with Iran, the Dow Jones Industrial Average surged 1125 points, or 2.49%; the Nasdaq Composite Index soared 3.83%; and the S&P 500 Index rose 2.91%. Technology and communication services sectors were the main drivers of this rally. However, this surge occurred against a backdrop of extreme market volatility – in March, Brent crude oil futures rose by as much as 63.3% in a single month, the largest monthly increase since records began in 1988, with international oil prices closing at $118.35 per barrel.

Garrett Melson, a portfolio strategist at Natixis Investment Managers Solutions, bluntly stated: "I don't think this rally is really trustworthy." He also pointed out that the end of the month and quarter nodes themselves are prone to amplified market fluctuations. Kevin Gordon, head of macro research and strategy at Charles Schwab Investment Research Center, said: "Today's market perfectly illustrates the current volatile market environment – everything can reverse in an instant."

Signs of easing in Iran situation, but uncertainty remains

The direct trigger for this rebound was a series of news reports suggesting a potential cooling of the U.S.-Iran conflict.

According to Xinhua News Agency, Trump is considering halting military strikes against Iran, even though the Strait of Hormuz remains under Tehran's control. Meanwhile, Iranian President Raisi stated that Iran has the "necessary willingness" to end the war, provided its demands are met, especially assurances of no further aggression.

However, Gordon noted that there is still a severe lack of accurate information regarding the extent of damage to Middle Eastern energy infrastructure, and future security measures remain unclear. Melson added that even if Trump manages to find an "exit strategy" for the conflict, it cannot guarantee a swift decline in oil prices: "We are in a race against the "oil price shock clock."

Market anxiety shifts from inflation to growth

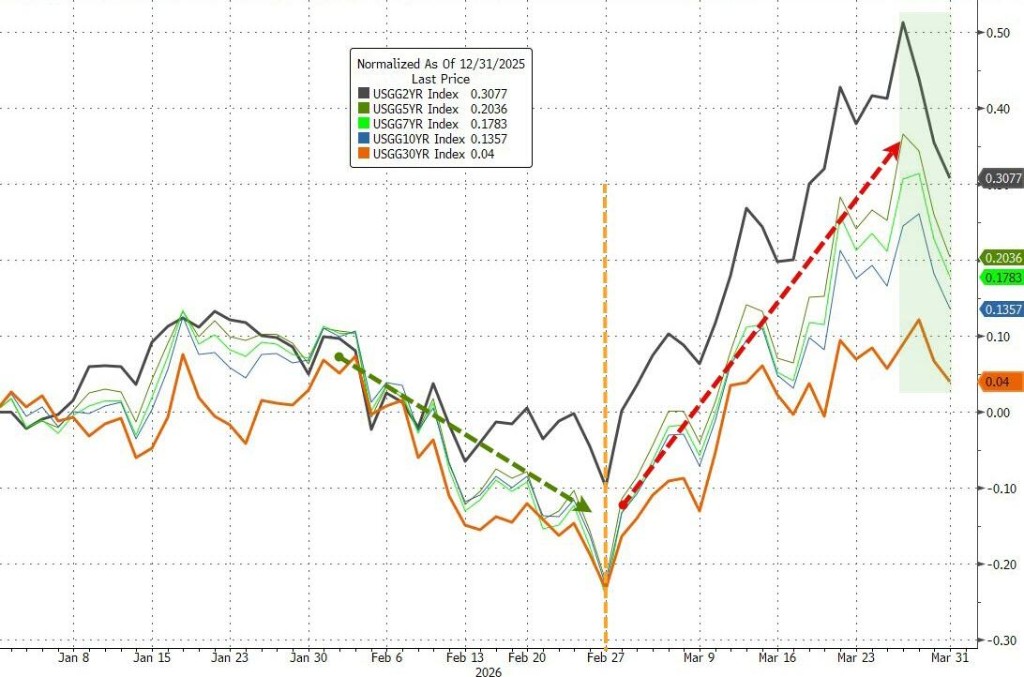

The bond market's performance revealed a subtle shift in investor sentiment.

On Tuesday, the yield on the 10-year U.S. Treasury note fell to 4.310%, down from the 2026 high of 4.439% reached last Friday. In the roughly $30 trillion Treasury market, funds are moving from "inflation concerns" to "growth worries."

Melson said: "The market is turning the page, shifting from worrying about inflation to worrying more about economic growth." He pointed out that during the first four weeks of the conflict, concerns that the Federal Reserve might be forced to raise interest rates due to inflationary pressures had loomed over the market. Now, the substantial damage that historically high oil prices could inflict on the economy is the core issue. He warned that if gasoline prices of $4 per gallon persist, or if higher oil prices begin to erode corporate profit margins, Wall Street will have to revise its current wait-and-see forecast.

Valuation improvement amid unrevised earnings expectations

Stocks experienced a significant adjustment in March. Except for the S&P 500 Index narrowly avoiding a technical bear market (defined as a decline of at least 10% from recent highs), the other three major stock indexes all entered correction territory within the month. Wells Fargo Securities and JPMorgan Chase have also recently lowered their year-end target prices for the S&P 500 Index.

According to data from FactSet senior earnings analyst John Butters, as of last Friday, the 12-month forward price-to-earnings ratio for the S&P 500 Index had fallen to 19.9 times from 22 times in December of last year, easing valuation pressures. Meanwhile, driven by upward revisions in earnings expectations for the energy sector, the overall earnings growth expectation for the first quarter was slightly raised to 13%, up from 12.8% the previous week.

However, Melson pointed out that the current valuation improvement is based on the premise that Wall Street has not yet substantially lowered earnings expectations – a situation mirroring the Federal Reserve's wait-and-see attitude. This premise will be tested once the impact of high oil prices on corporate profits becomes apparent.