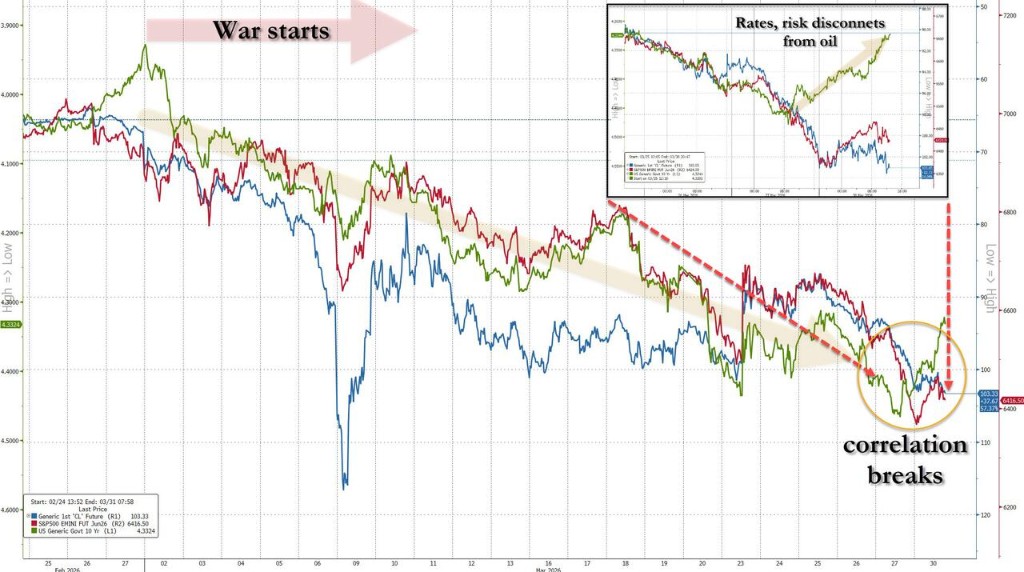

Market Logic Shifts! First Time Since Iran Conflict: U.S. Energy Stocks Fall, U.S. Treasuries and Gold "Decouple" from Oil Prices

Oil prices breaking $100 should have pushed up Inflation Expectations, but overnight 10-Year Treasury yields moved lower while gold surged, and U.S. energy stocks fell alongside the broader market. JP Morgan believes this signal proves a "shift from inflation trades to recession trades." The probability of a Federal Reserve rate hike in 2026 plummeted by over 15 percentage points in a single week, as the market pivoted back to betting on a mild rate cut this year

The market is sending a rare signal: the inflation trade that has dominated Wall Street for weeks is unraveling, and the recession trade is quietly taking over.

Overnight U.S. stocks opened high but closed low, with the three major indices failing to sustain their opening gains. Technology and chip sectors were the biggest drags on the S&P 500, while the energy sector also closed slightly down. Meanwhile, WTI crude futures rose more than 3%, breaking the $100 mark, yet 10-Year Treasury yields moved inversely lower, and gold surged significantly at one point.

This combination of movements is extremely rare – according to JP Morgan, this is the first time since the outbreak of the Iran conflict, and only the second time this year, that energy stocks and the broader market have declined simultaneously while bonds and gold have risen together.

JP Morgan interprets this signal as a critical shift in market trading logic: "This may prove that the market's trading logic has shifted from an inflation trade to a recession trade." Concurrently, money markets adjusted their pricing, with the probability of a Federal Reserve rate hike in 2026 dropping from about 35% last Friday to approximately 20%. Markets have begun to re-price expectations for a mild rate cut within the year.

Oil Prices Top $100, Yet U.S. Treasuries and Gold Strengthen in Opposite Directions

Overnight, WTI May crude oil futures settled up $3.24, marking the first close above the $100 per barrel psychological level since July 2022. Following the market logic of previous weeks, soaring oil prices should have driven up Inflation Expectations, thereby depressing bond prices and pushing yields higher.

However, Monday's trading saw the opposite. By late New York trading, the 10-Year Treasury Yield fell 8.95 basis points, continuing its decline throughout the day; the 2-year U.S. Treasury yield dropped 9.22 basis points.

Gold surged significantly at one point, with gains reaching up to 3.6%. Federal Reserve Chair Powell's dovish remarks that day further reinforced the market's bets on rate cuts. Money markets immediately adjusted their pricing, lowering the probability of a Fed rate hike in 2026 from about 35% last Friday to approximately 20%, and shifting to re-price expectations for a mild rate cut within the year.

This "decoupling of bonds and oil" signals the market's shift from short-term inflation fears to concerns about a medium-term economic recession.

Inflation Expectations Quietly Subside, Growth Concerns Emerge

Despite the continuous surge in energy prices, long-term Inflation Expectations have shown almost no significant upward movement. Measured by the five-year inflation swap, market expectations for inflation over the next five years have fallen by about 20 basis points from their January peak, returning to levels seen during the volatile period last April.

Goldman Sachs analyst Chris Hussey pointed out that the core of the market's focus this week remains the tug-of-war between growth and inflation: on the inflation front, spiraling prices of oil, natural gas, aluminum, and their derivatives threaten to spread globally, especially into Asia. On the growth front, the continued uncertainty in the Middle East, coupled with the shock of energy prices, is dimming the outlook for labor demand. Goldman's assessment is that under various scenarios, bond yields will eventually decline, and long-term stock volatility will increase, leading to a situation where the market faces "economic growth fears" rather than "persistent inflation fears."

Francisco Simón, Head of European Strategy at Santander Asset Management, also stated that while inflation remains a concern, the potential drag on growth and confidence should begin to form a hedge, limiting further upward movement in yields. He added that the bond market is currently one of the clearest tools for pricing the macroeconomic impact of this conflict.

Fiscal Stimulus Expectations Priced In, Morgan Stanley Highlights U.S. Treasury Pricing Logic

Morgan Stanley's chief interest rate strategist, Matthew Hornbach, suggested that the U.S. interest rate market may be increasingly reflecting an expectation that fiscal stimulus will follow the demand destruction caused by energy prices. This view implies that the strength in the bond market is not solely driven by risk aversion but by markets beginning to position for the next round of policy responses.

Torsten Slok, Chief Economist at Apollo, noted that there is a significant premium embedded in current 10-year Treasury rates. Under normal Federal Reserve expectations, the 10-Year Treasury Yield should be around 3.9%, not the current 4.4%, implying an "excess premium" of approximately 55 basis points. The source of this premium could include fiscal concerns, quantitative tightening, declining foreign demand, and doubts about the Federal Reserve's independence. Slok commented, "Investors need to seriously consider what these 55 basis points actually mean."