Guo Jin Mou Yiling: Signals for Risk Asset Bottoming and Medium-Term Themes

The weakening dollar is showing signs of bottoming out for risk assets. The US-Iran conflict is manageable, and non-US central banks are prioritizing interest rate hikes, limiting dollar strength. The dollar index has not broken past 100.50. Market pricing of a prolonged US involvement in the Iran issue has led to a sell-off in US equities, signaling a bottom for global risk assets. Trump's cycle of pressure and compromise has failed to achieve "America First," instead causing the dollar to weaken

Abstract

1 The Dollar Illusion Fades, Risk Assets Show Signs of Bottoming

In last week's report, we posited that the market downturn was essentially a dollar resurgence. However, this week, amid the new US-Iran conflict and the escalating impact of prior energy supply disruptions, the "strong dollar" trend has moderated. On one hand, the US-Iran conflict is evolving into a prolonged but controllable situation: diplomatic channels are opening, though military actions continue; on the other hand, a month has passed since the Strait of Hormuz closure, and rising oil prices are creating inflationary pressures globally. Consequently, non-US central banks are bringing interest rate hikes back to the agenda, constraining the strong dollar. The characteristics signaling a bottom for risk assets include the dollar index topping out, a cooling of market expectations for Federal Reserve rate hikes, and a pullback in US assets that limits the conflict's intensity. This week, the dollar index rose by 0.68%, but its peak (100.20) did not surpass the 100.50 high reached in the third week of the conflict. As we noted last week, the market is increasingly pricing in the possibility of the US getting bogged down in a protracted conflict over Iran, potentially undermining its fundamental advantages. This is evidenced by the sell-off in US equities, which had previously outperformed. This situation, to some extent, curbs the US's willingness to escalate the conflict further, or suggests that the ongoing war is beginning to drag down US assets, reducing their pull on non-US stocks and physical assets, with gold already rebounding on rising oil prices.

2 Trump's Asset Price Cycles: Lessons from the Pressure-Compromise Loop

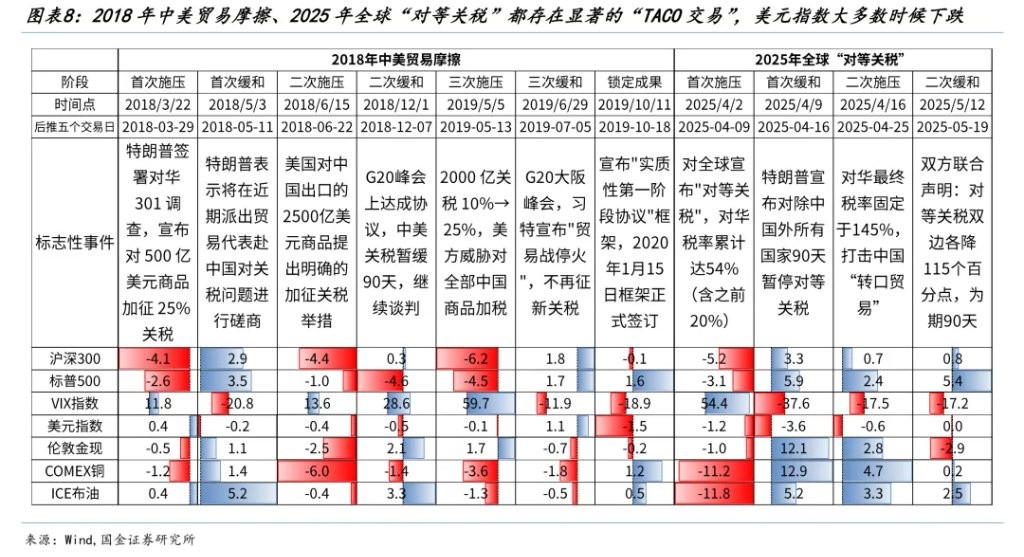

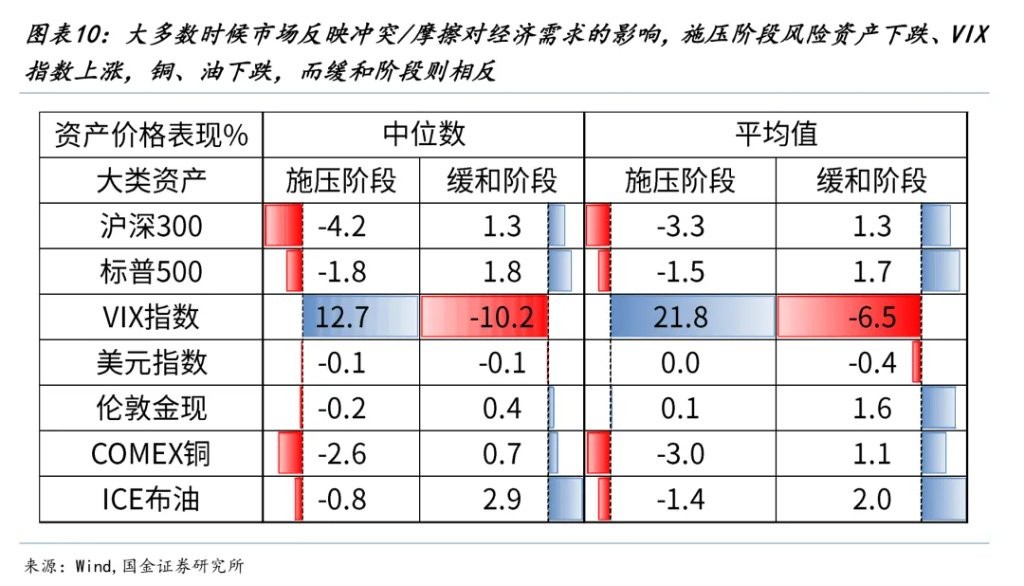

Throughout Trump's two terms, a consistent pattern emerged: to achieve ultimate objectives, he would first apply extreme pressure on targets, then offer space for compromise to gain acceptance of terms (the "TACO" strategy), and reapply pressure if conditions weren't met, creating a cyclical process. However, this modus operandi proved unsuccessful in achieving "America First" during the US-China trade friction (2018-2020), the sanctions on Iran over its nuclear deal (2018-2020), and the proposed "reciprocal tariffs" on a global scale (2025). Instead, the dollar index consistently weakened in the later stages. Additionally, asset performance followed a pattern: (1) During pressure phases, risk assets fell, the VIX rose, and copper and oil prices declined, generally reflecting suppressed aggregate demand. The "TACO" phase saw the opposite, with gold and dollar movements being less predictable. (2) As time progressed, the rebound amplitude of these assets after "TACO" periods diminished significantly, as historical precedents taught markets that "pauses do not equate to resolutions, merely a deferral of risk." (3) The simultaneous rise of the dollar, gold, and Brent crude oil, as seen last Friday evening, is rare but occurred similarly on January 3, 2020, following the US assassination of a senior Iranian general. This priced in escalated geopolitical risk (driving gold up), while the consequences of prolonged conflict (driving oil up) disproportionately harmed non-US countries relative to the US (leading to a stronger dollar).

3 Beyond Volatility: What to Buy Next

The magnitude of each "TACO" transaction cycle is diminishing, and the market is no longer trading solely on the basis of friction/conflict. Instead, it is focusing on medium-term themes. For A-shares, we identify clear main themes and optimal assets across three dimensions: The initiated and directly related theme is energy. The US-Iran conflict exhibits a "prolonged" characteristic, with the Strait of Hormuz remaining closed and oil transportation still disrupted. Even after reopening, supply losses and inventory concerns will lead to a sustained higher energy price center. Furthermore, the significant increase in old energy prices will accelerate the adoption of new energy sources; domestic battery manufacturers saw a substantial month-on-month increase in production in March. The second theme is the peaking and subsequent decline of the dollar, leading to a rebound in commodity prices driven by their monetary attributes, where stocks in the price-increase chain begin to outperform their corresponding commodities. The third theme is the strengthening of manufacturing advantages due to the current energy shock. While China is resource-poor in oil and gas, its current ample oil reserves, energy self-sufficiency centered on coal, and its new energy industrial chain provide long-term advantages in navigating the post-energy shock landscape of global re-industrialization.

4 Market's Core Trio: Energy, Currency, and Manufacturing Landscape Reshaping

Energy, the dollar, and the reshaping of the manufacturing landscape have emerged as three critical drivers in this market volatility, offering investors the best handles for assessing aggregate and structural trends. We prioritize new and old energy sources: crude oil, oil shipping, coal, and power equipment (lithium batteries, wind, solar, energy storage), as well as electricity. Next, as the dollar illusion gradually dissipates, we anticipate a rebound in commodity prices driven by their financial attributes: copper, aluminum, and gold. Finally, we foresee a revaluation of China's manufacturing sector: machinery and equipment, chemicals. Sustained export outperformance and capital inflows will also drive domestic demand, which has been dormant for a long time, leading opportunities in tourism and scenic spots, fermented condiments, beer and other alcoholic beverages, pharmaceutical distribution, and medical aesthetics.

Report Body

1 The Dollar Illusion Fades, Risk Assets Show Signs of Bottoming

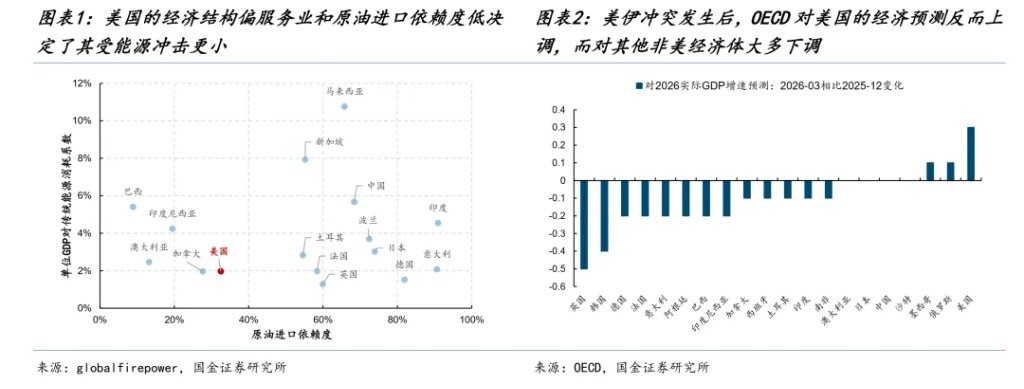

In last week's report, we proposed that the market downturn was fundamentally a dollar counterattack. The US-Iran conflict solidified two core logics for a strong dollar: (1) From an economic fundamentals perspective, the US, with its service-oriented economy, relies significantly less on traditional energy than other nations, thus experiencing less impact and maintaining a relative economic advantage. (2) Amid geopolitical conflicts, investors seek "safe-haven" assets. Between gold and the dollar, the US's demonstration of force in the Middle East has, to some extent, signaled its control over global order, thereby strengthening the dollar.

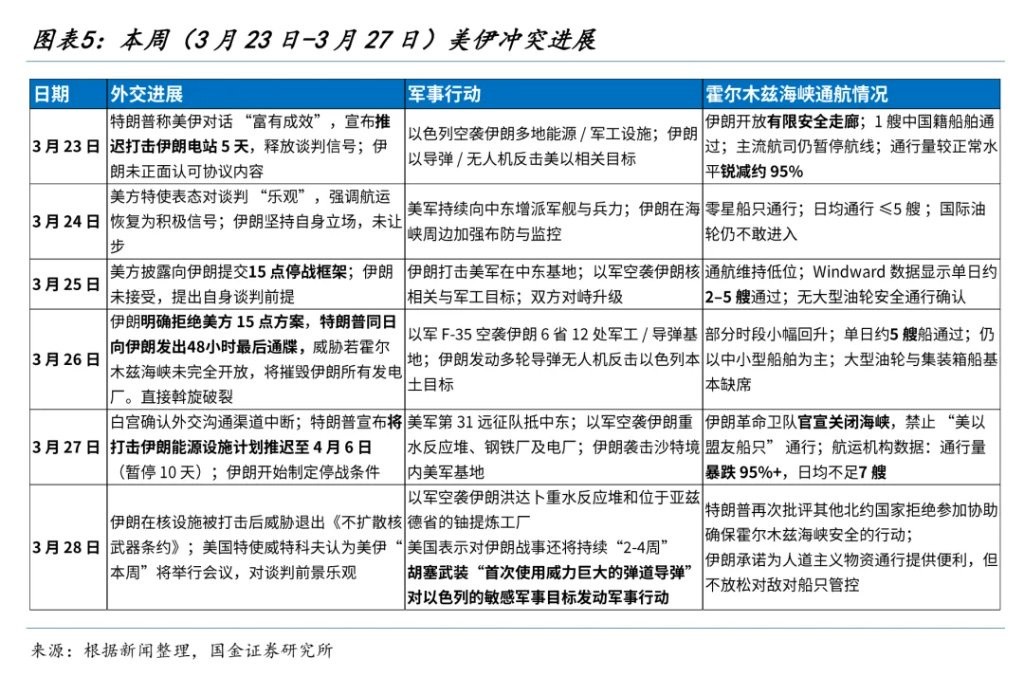

However, this week, amid the new US-Iran conflict and the escalating impact of prior energy supply disruptions, the "strong dollar" trend has moderated. On one hand, the US-Iran conflict is evolving into a prolonged but controllable situation: controllability is evident on the diplomatic front; although Iran directly rejected the US's 15-point proposal, it also presented five preconditions for negotiations, opening a potential window for talks. The US has also expressed conciliatory remarks, with Trump tweeting on Thursday, March 26th, that the airstrikes on Iranian energy facilities would be postponed for ten days, until April 6th at 8 PM EST. The prolongation is evident on the military front, with neither side showing signs of a short-term "ceasefire." The US continues to reinforce its Middle East presence, Israel has conducted airstrikes on Iranian energy and infrastructure facilities, and Iran continues to attack US military bases in the region. On the other hand, a month has passed since the closure of the Strait of Hormuz, and the substantial increase in oil prices is beginning to create inflationary pressures in various countries. Against this backdrop, non-US central banks are increasingly bringing interest rate hikes to the agenda, which also serves as a constraint on the "strong dollar."

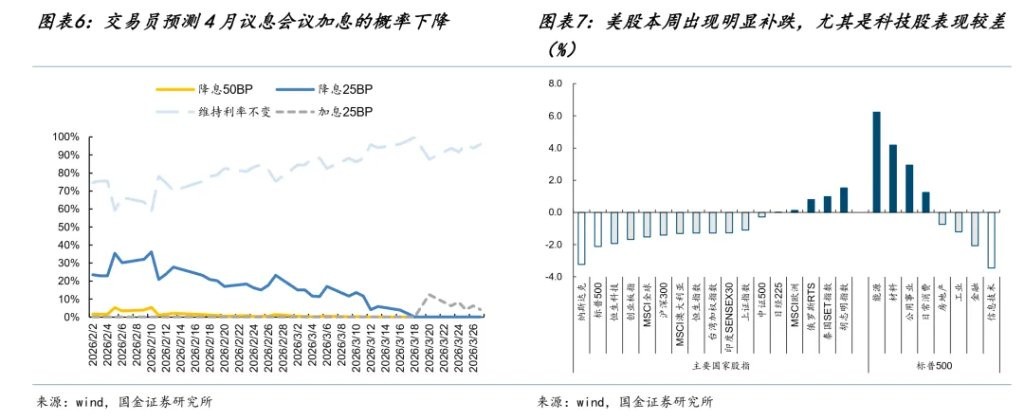

Risk assets are showing signs of bottoming out: the dollar index has peaked, market expectations for Federal Reserve rate hikes are cooling, and a pullback in US assets is constraining the conflict's intensity. This week, the dollar index rose by 0.68%, but its peak (100.20) did not surpass the 100.50 high reached in the third week of the conflict. This could be due to two reasons: Firstly, market expectations for the Federal Reserve to raise rates at its next policy meeting have cooled compared to last week, reducing support for the dollar index; the probability has dropped from a high of 12.4% last Friday to 4.1% this Friday. Secondly, as we mentioned in last week's report, the US might become mired in a protracted conflict over Iran, thereby weakening its fundamental advantages (e.g., the tech supply chain losing support from Japanese and Korean suppliers). This week, the market has increasingly priced in this possibility, leading to a sell-off in US equities, which had previously outperformed. This, to some extent, constrains the US's willingness to escalate and engage further in the conflict. On Thursday, Trump's statement about postponing strikes on Iranian energy facilities might be proof that financial asset volatility is limiting the conflict's intensity.

2 Trump's Asset Price Cycles: Lessons from the Pressure-Compromise Loop

Throughout Trump's two terms, a consistent behavior pattern emerged: to achieve ultimate objectives, he would first apply extreme pressure on targets, then voluntarily offer room for compromise to gain acceptance of terms (the "TACO" strategy), and reapply pressure if conditions weren't met, thus creating a cyclical process. This pattern was evident in the US-China trade friction (2018-2020), the sanctions on Iran over its nuclear deal withdrawal (2018-2020), and the proposed "reciprocal tariffs" on a global scale (2025). In these three instances, Trump's "pressure-TACO" cycles failed to yield clear "outcomes" or achieve "America First": The first US-China trade war, while securing the Phase One trade deal, did not result in the promised purchase of US agricultural products and failed to reduce the US trade deficit. The global reciprocal tariff initiative has yielded no concrete results to date and was even ruled unconstitutional by the US Supreme Court. The sanctions on Iran following its withdrawal from the nuclear deal (2018-2020) did not lead to any negotiations; instead, Iran exceeded all limits set by the nuclear deal.

During these pressure-to-compromise cycles, asset performance exhibited certain patterns: (1) During pressure phases, risk assets declined, the VIX index rose, and copper and oil prices fell, generally reflecting suppressed aggregate demand. The "TACO" phase saw the opposite, with gold and dollar movements being less predictable. (2) As time progressed, the rebound amplitude of these assets after "TACO" periods diminished significantly, as historical precedents taught markets that "pauses do not equate to resolutions, merely a deferral of risk." (3) The simultaneous rise of the dollar, gold, and Brent crude oil, as seen last Friday evening, is rare but occurred similarly on January 3, 2020, following the US assassination of a senior Iranian general. This priced in escalated geopolitical risk (driving gold up), while the consequences of prolonged conflict (driving oil up) disproportionately harmed non-US countries relative to the US (leading to a stronger dollar). The resurgence of gold's safe-haven appeal also indicates that the dollar's strength is nearing a turning point, as the underlying resilience of the US economy and its overall national strength are weakening.

Based on these historical experiences, the current US-Iran conflict may witness further asset price fluctuations driven by multiple "pressure-TACO" cycles. Future developments to watch for that could disrupt the current market pricing of "strong dollar, strong gold, persistently high oil prices" include: One scenario is that the US's own economic fundamentals are negatively impacted by rising oil prices, for instance, if AI supply chains face disruptions due to energy shortages, and a weakening economy prevents the Fed from considering rate hikes. In this case, the dollar would weaken definitively, and gold would experience a substantial rebound driven by its financial attributes. Another scenario, similar to previous "pressure-TACO" cycles, is that Trump's current actions in the Middle East yield no clear results, especially after the US prolonged sanctions on Iran while excluding military strikes, as seen on January 9, 2020. This would lead to another downgrade of the dollar's creditworthiness, and gold would regain its long-term narrative as a "dollar alternative."

3 Beyond Volatility, the Market is Asking "What to Buy Next?"

As summarized above, the magnitude of each "TACO" transaction cycle is diminishing, and in reality, Trump's previous pressure-and-ease cycles have not achieved long-term success. Consequently, the market is shifting its focus from trading solely on friction/conflict to identifying medium-term themes. For A-shares, we believe there is a clear main theme and optimal assets spanning short, medium, and long terms.

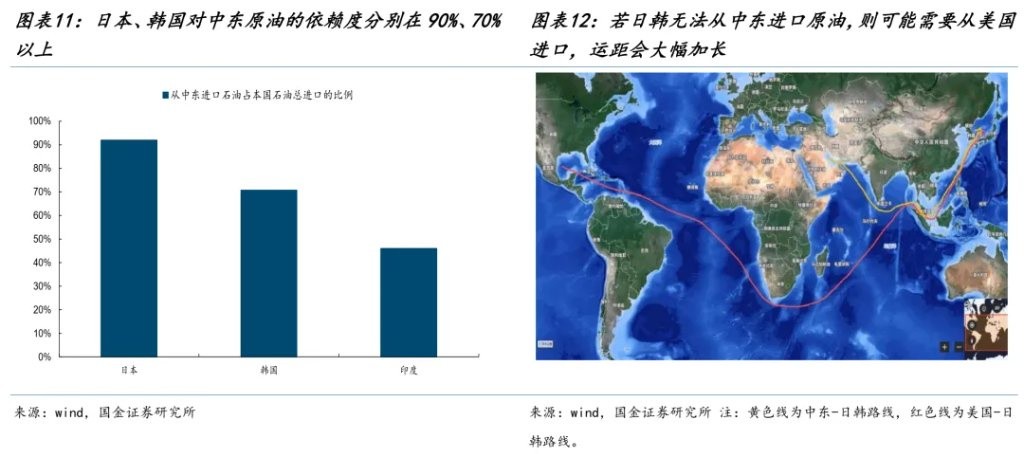

Short-term, the energy theme has already begun. Given the "prolonged" nature of the current US-Iran conflict, the continuous closure of the Strait of Hormuz, and ongoing disruptions to oil transport, countries dependent on Middle Eastern oil imports are forced to seek alternative sources. For example, Japan and South Korea might have to import crude oil from the US, and India may need to transport oil from farther afield, such as Russia. These route changes will significantly increase shipping distances. The substantial rise in old energy prices will also accelerate the adoption of new energy sources. In March, production for domestic battery sample enterprises increased by 21.93% month-on-month. Cathode and anode production rose by 23.3% and 16.42% respectively; diaphragms and electrolytes increased by 8.7% and 18.78% respectively.

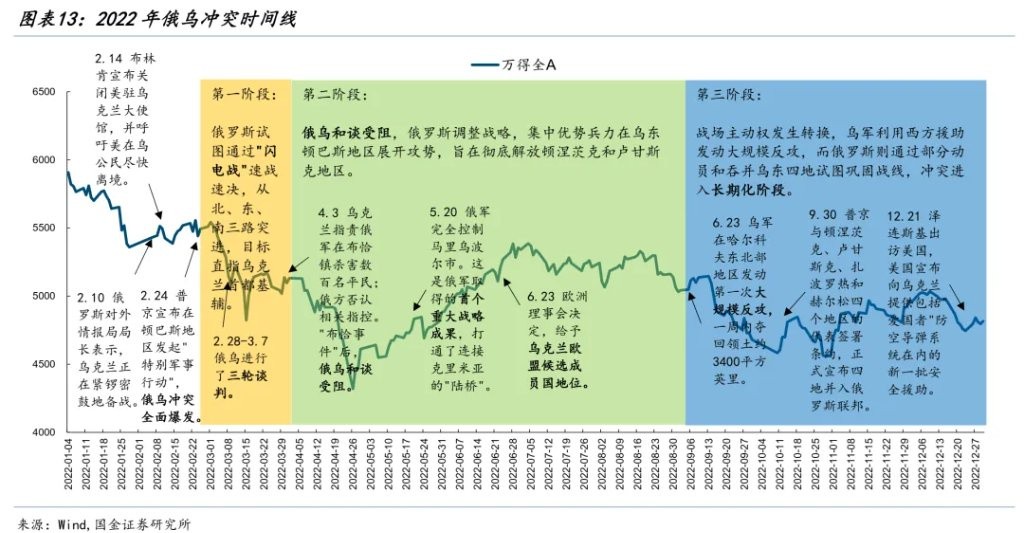

In the medium term, we anticipate the dollar peaking and declining, leading to a rebound in commodity prices driven by their financial attributes. During this phase, stocks in the price-increase chain will begin to outperform their corresponding commodities. Looking back at the Russia-Ukraine conflict in 2022, after the expectation of a "lightning war" resolution between Russia and Ukraine faded, they entered a repetitive game of "localized conflict - possibility of negotiation - localized conflict." At that point, commodity prices might not have seen further "explosive increases," but the confirmation of reduced volatility and a higher center of gravity allowed investors to better value the long-term production capacity of stocks, leading stocks to outperform commodities.

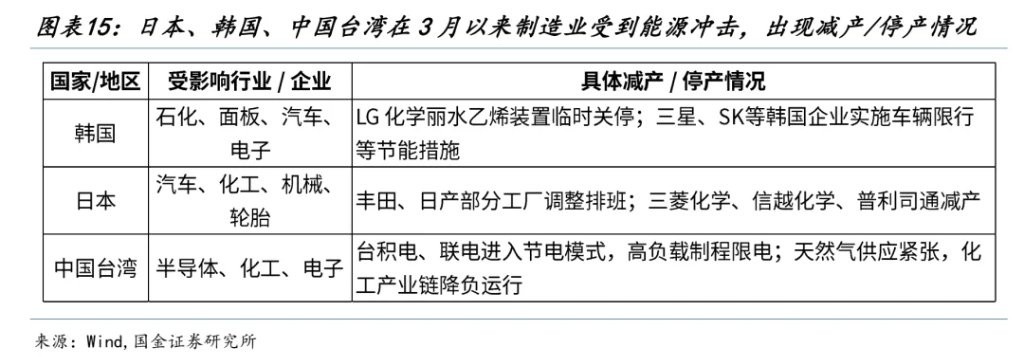

In the long term, manufacturing advantages are strengthened by the current energy shock. While China is resource-poor in oil and gas, its current ample oil reserves, energy self-sufficiency centered on coal, and its new energy industrial chain offer advantages in navigating the post-energy shock global re-industrialization landscape. For example, during the Russia-Ukraine conflict in 2022, Europe's reduced natural gas imports from Russia led to higher gas prices, forcing its chemical giants to cut production or even shut down, allowing China to further replace Europe's share in the global chemical market. Currently, Japan, South Korea, and Taiwan have experienced varying degrees of production cuts or shutdowns since March due to energy supply issues, affecting industries such as chemicals, electronics, automotive, and machinery. In our spring strategy report, "Return to Reality," we identified absolute global leaders and high-growth leaders in Chinese manufacturing, concentrated in sectors like chemicals, electrical machinery, and electrical equipment. These absolute leaders are continuously validating their overseas revenue growth and profit margins, yet their valuations still differ significantly from global peers, offering room for valuation expansion.

4 Energy, Currency, and the Reshaping of Manufacturing Landscape

The dollar illusion is gradually fading, and signs of risk assets bottoming out are becoming clearer. Despite the rapid market volatility this week, based on Trump's past "pressure-TACO" cycles, the fluctuations are expected to narrow in subsequent rounds of negotiation. The market will begin to focus on the true medium- to long-term themes. A potential risk is that if the US economic fundamentals can no longer sustain their "self-preservation" logic and relative advantages begin to weaken, the dollar illusion will completely dissipate, potentially leading to a significant rebound in gold. However, this would present new challenges for equity markets and commodity demand. In our view, the best approach for managing short-term volatility is to allocate capital to the source of volatility – energy. From a medium-term perspective, investors can follow the rhythm of the "pressure-TACO" cycles and the gradual weakening of the dollar to profit from the financial attributes of commodities. In the long term, this conflict, similar to the Russia-Ukraine conflict in 2022, highlights China's manufacturing advantages in energy self-sufficiency and control. Our recommendations are:

First, amidst the current global instability, energy security has become paramount. We prioritize new and old energy sources – crude oil, oil shipping, coal, and power equipment (lithium batteries, wind, solar, energy storage);

Second, as the dollar illusion gradually retreats, expect a rebound in the financial attributes of commodities – copper, aluminum, and gold;

Third, a revaluation of Chinese manufacturing – machinery and equipment, chemicals. As Chinese manufacturing becomes the global anchor, sustained export outperformance and capital inflows will also drive domestic demand, which has been dormant for a long time, creating structural opportunities amidst the reversal of suppressive factors – look for opportunities in tourism and scenic spots, fermented condiments, beer and other alcoholic beverages, pharmaceutical distribution, and medical aesthetics.

Risk Disclosure and Disclaimer

Markets are risky; investment requires caution. This article does not constitute personal investment advice, nor does it consider the specific investment objectives, financial situation, or needs of individual users. Users should consider whether any opinion, view, or conclusion in this article is appropriate for their specific circumstances. Investment based on this is at the user's own risk.