Iranian War Shocks Gold Market, Central Bank's "Permanent Buyer" Myth Begins to Waver!

Turkey's sale of over $8 billion in gold reserves this month has sparked concerns about a collective shift from central banks globally to becoming sellers. If this trend continues to spread, it could fundamentally overturn the key logic that has driven gold prices to new highs over the past decade

A core pillar of support for the gold market is beginning to crumble.

Since March, the Central Bank of Turkey has sold and swapped approximately 60 tons of gold, a volume exceeding the outflows from gold ETFs during the same period. The selling pressure from the latter had already intensified due to the 'cash is king' sentiment driven by financial market turmoil, rising bond yields, and a strengthening dollar.

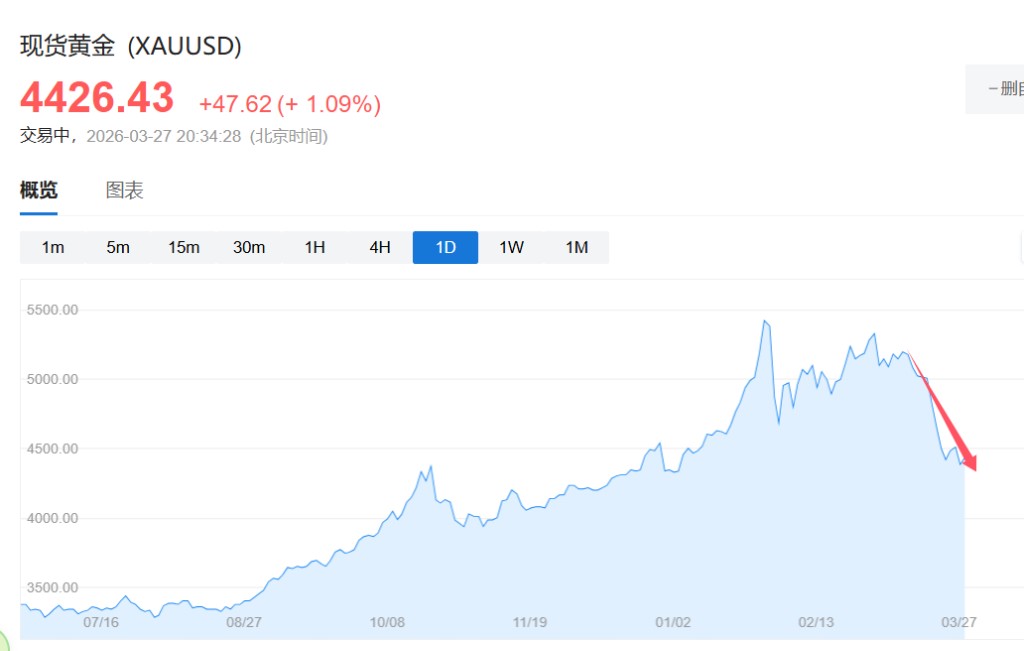

Gold prices have fallen about 18% from their peak of over $5,000 an ounce earlier this year. The escalating conflict in the Middle East and soaring energy costs are forcing more energy-importing nations to use their gold reserves to obtain U.S. dollars, posing an unprecedented challenge to the market consensus of central banks being "one-way buyers" of gold.

Turkey Leads the Way, Breaking the "Central Banks Don't Sell Gold" Convention

The scale of Turkey's selling has caught the market's attention. In two weeks of March, the country's central bank sold and swapped about 60 tons of gold, worth over $8 billion, to counter the currency pressures from surging energy costs and a spike in demand for U.S. dollars.

This volume has already surpassed the net outflow from gold ETFs during the same period – outflows that were themselves under scrutiny due to overall financial market turbulence, rising bond yields, and the dollar's rebound.

Nicky Shiels, Head of Metals Strategy at MKS PAMP SA, stated: "The narrative of central banks as permanent, one-way buyers is being challenged."

Central Bank Gold Purchases: The Cornerstone of the Post-2022 Gold Bull Market

Since the global financial crisis, central banks have generally been net buyers of gold. At the end of 2022, the freezing of Russia's foreign exchange reserves highlighted the need to diversify away from dollar assets, leading to a significant acceleration in central bank gold purchases. Sovereign buyers' annual gold purchases have amounted to roughly a quarter of the world's annual mine supply.

Driven by this trend, gold prices have more than doubled since 2022 and surpassed the $5,000 an ounce mark earlier this year.

However, the geo-economic shockwaves triggered by the war in Iran are eroding this support. If more central banks follow Turkey's lead, the overall pace of gold purchases will significantly slow down, and the market's long-held assumption of central banks being "reluctant sellers of gold" will be fundamentally questioned.

Energy Importers and Gulf Nations: Reserve Dilemmas Under Dual Pressure

The transmission path of this risk is clear. Some countries that have accumulated substantial gold reserves are themselves energy importers. A sharp increase in oil and gas bills means reduced dollar holdings available for replenishing precious metal reserves, thereby decreasing gold purchasing power.

Simultaneously, Persian Gulf nations are also facing pressure. The blockade of most energy exports through the Strait of Hormuz has severely squeezed the inflow of petrodollars that these countries rely on to sustain their fiscal health. Although Gulf nations hold substantial diversified assets, the depletion of petrodollars still constrains their reserve management.

Gold Market Lacks a "Lender of Last Resort" Mechanism, Rising Risk of Downward Spiral

Unlike the U.S. Treasury market, the gold market lacks a unified management body overseeing all parties. This means that gold assets held by various countries will not face the threat of being frozen. However, it also implies that there is no institution, like the Federal Reserve, that can act as a "lender of last resort" to shore up prices during a crisis.

Gold bulls are currently looking to the People's Bank of China to fill the demand gap. However, according to Bloomberg analysis, if emerging market economies collectively enter the market to sell gold for dollars during a crisis, the self-reinforcing downward price spiral will be even harder to contain.

Gold prices have already seen a significant pullback from their peak, and the uncertainty surrounding the war's trajectory and energy markets makes it difficult to determine when this pressure will bottom out.