Shenwan Hongyuan: The Current Moment May Be the Phase of Greatest Pressure; China's Energy and Supply Chain Security Could Be Global Alpha

Shenwan Hongyuan points out that the market is currently facing its most pressured phase. Impacted by the US-Iran conflict, risk appetite continues to be under pressure, and funds are seeing a concentrated short-term withdrawal. Mid-term variables are being underestimated; monetary tightening to counter imported inflation is a suboptimal strategy, while an increase in inflation tolerance is highly probable. Although the US-Iran conflict may see recurrences, its impact on A-shares is expected to gradually diminish. Short-term market projections indicate that rising oil prices and shipping costs could lead to a stagflation cycle, causing a synchronized decline in stock fundamentals and valuations. Amid the concentrated withdrawal of funds, the implementation of steady and sustained growth policies is logical

- I. The stalemate in the US-Iran conflict continues to weigh on risk appetite. Attention should be paid to the short-term concentrated withdrawal of funds that supported the "first phase of the rally" (shrinking industry ETF sizes, annuities reducing positions to avoid net value losses, and "Fixed Income+" position reductions and redemptions). This suggests the current moment may already be the phase of greatest pressure. The implementation of steady and sustained growth policies is logical; however, note that there may be differences between the structure of steady and sustained growth policies and the structure of absolute return fund reductions, which could constitute tail risks.

- We still remind that mid-term variables are underestimated: 1. For both China and the US, monetary tightening to deal with imported inflation is a suboptimal strategy. Increasing inflation tolerance is a high probability. 2. The US economy is resilient, and China's economy has room for maneuver; recession is not the baseline assumption. 3. Amid geopolitical stalemate, China's energy security and supply chain security could be global Alpha. Even if the US-Iran conflict sees mid-term recurrences, its impact on A-shares will likely gradually diminish.

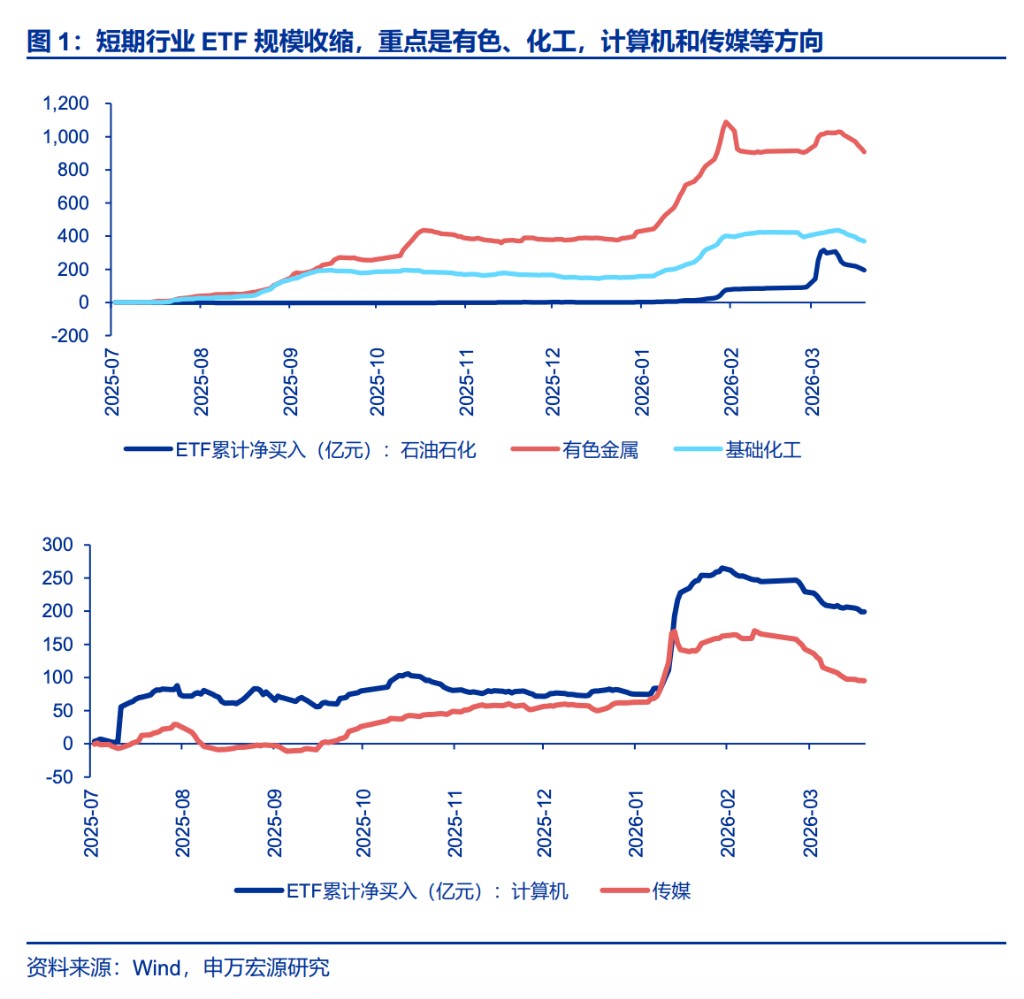

- The US-Iran conflict has reached a stalemate, and all parties are inadequately prepared for a new Middle Eastern order. However, the formation of a new equilibrium will still require a long period of strategic maneuvering. This is reflected in the ongoing short-term event-driven disturbances, which directly pressure capital market risk appetite. Short-term market projections of the US-Iran conflict's impact primarily draw parallels from the experiences of the two oil crises: rising oil prices and shipping costs → rising inflation → monetary tightening → economic recession, confirming a stagflationary cycle → synchronized decline in stock fundamentals and valuations. This logic chain cannot be falsified in the short term. Simultaneously, we note a short-term concentrated withdrawal of funds that supported the "first phase of the rally": 1. Shrinking industry ETF sizes, particularly in the non-ferrous, chemical, computer, and media sectors.

-

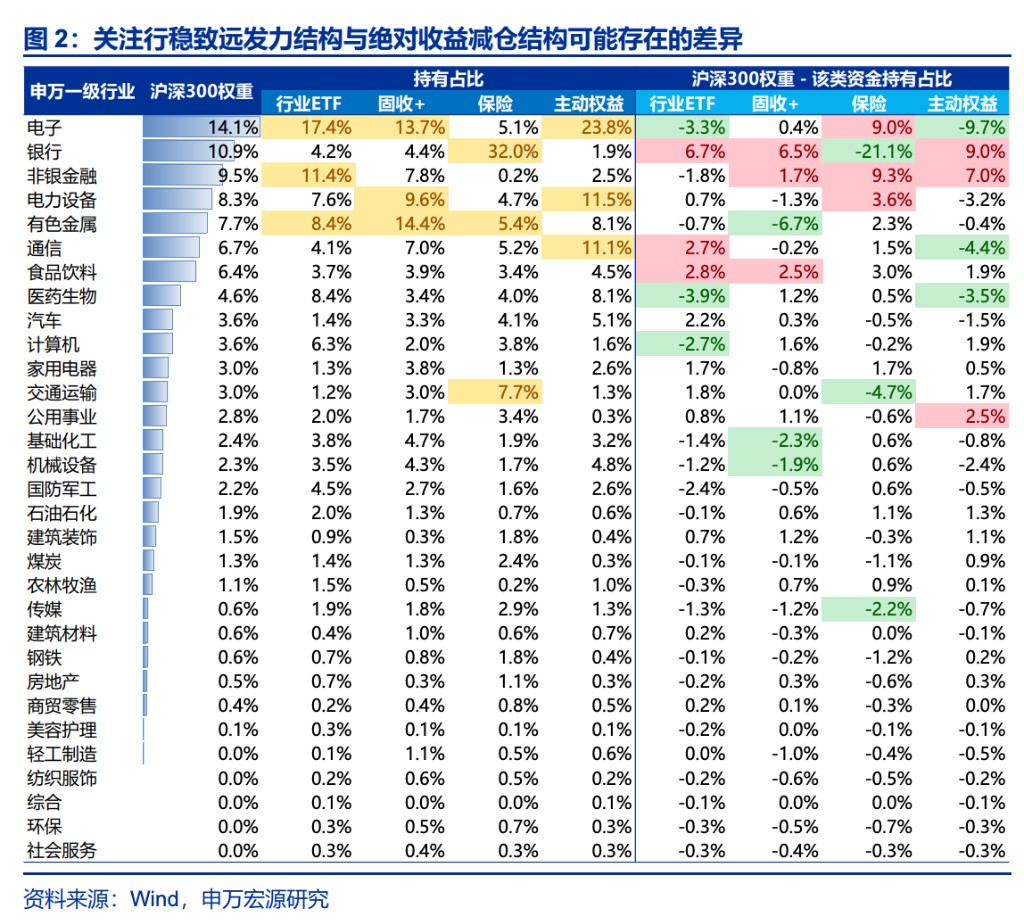

- Absolute return funds are seeing their floating profits rapidly shrink, forcing them to reduce equity positions to avoid principal losses. Annuities, which had significantly increased their equity exposure earlier, are seeing the stability of their high positions decline in the short term. Referencing the holding structures of active public funds and "Fixed Income+" products, sectors such as non-ferrous, chemicals, communications, and electronics may all face pressure for position reductions. Allocation-based funds increased equity exposure in this round, with "Fixed Income+" products being an important channel, and short-term redemption pressure is beginning to manifest. With the concentrated withdrawal of funds, the implementation of steady and sustained growth policies is logical. Attention should be paid to potential differences between the structure of steady and sustained growth efforts and the structure of absolute return fund reductions (CSI 300 weight - industry ETF weight, CSI 300 weight - "Fixed Income+" holding weight). Overall index risk is controllable, but structural shocks may still pose tail risks.

- II. Mid-term: The A-share market is in a period of oscillation and consolidation between the "two-phase rally." Short-term: The market may follow a process of "oversold → steady and sustained growth policy implementation → rebound." Subsequently, it will likely remain in range-bound oscillation, with leading sectors continuing to rotate. In phases with new main theme opportunities (such as short-term rallies in energy storage and optical communications based on prosperity validation), the market may challenge the upper bound of the oscillation range; however, if the evolution of main themes is hindered after a rebound, the market may test the lower bound of the oscillation range.

- III. Short-term: Recommendations continue to center on the "prioritize reality" structure, with CPO and energy storage being strong directions. Under the shock of energy costs, new energy and new energy vehicles benefit from energy diversification and trends towards energy supply resilience, potentially becoming important strategic resources alongside traditional energy. Additionally, for structures that are highly likely to participate in the "second phase of the rally" (AI industry chain + price increase cycle), dips can be utilized for positioning, though short-term timeliness is limited. We reiterate that based on historical experience, the style characteristics of the two-phase rally are consistent. During the intermediate consolidation phase, the style is not a rotation from high to low, but rather a broader diffusion of main themes. High-elasticity investment opportunities still primarily stem from the extension of main assets + the expansion of macroeconomic narratives.

- Mapping to the present, the "prioritize reality" characteristic will persist at least until the first-quarter earnings season. The subsequent evolution of the AI industry trend may shift from the hardware end toward the application end; focus on "picks and shovels" in the application layer (cloud computing, edge devices, robotics), the domestic AI chain catching up (major domestic manufacturer chains), and opportunities for AI to transform traditional industries (contrary to HALO trades). Expansion of macroeconomic narratives: focus on the possibility of strengthened pricing based on shifts in relative national power, which presents an opportunity for the revaluation of manufacturing.

I. The stalemate in the US-Iran conflict continues to weigh on risk appetite. Attention should be paid to the short-term concentrated withdrawal of funds that supported the "first phase of the rally" (shrinking industry ETF sizes, annuities reducing positions to avoid net value losses, and "Fixed Income+" position reductions and redemptions). This suggests the current moment may already be the phase of greatest pressure. The implementation of steady and sustained growth policies is logical; however, note that there may be differences between the structure of steady and sustained growth policies and the structure of absolute return fund reductions, which could constitute tail risks.

We still remind that mid-term variables are underestimated: 1. For both China and the US, monetary tightening to deal with imported inflation is a suboptimal strategy. Increasing inflation tolerance is a high probability. 2. The US economy is resilient, and China's economy has room for maneuver; recession is not the baseline assumption. 3. Amid geopolitical stalemate, China's energy security and supply chain security could be global Alpha. Even if the US-Iran conflict sees mid-term recurrences, its impact on A-shares will likely gradually diminish.

The US-Iran conflict has reached a stalemate, and all parties are inadequately prepared for a new Middle Eastern order. However, the formation of a new equilibrium will still require a long period of strategic maneuvering. This is reflected in the ongoing short-term event-driven disturbances, which directly pressure capital market risk appetite. Short-term market projections of the US-Iran conflict's impact primarily draw parallels from the experiences of the two oil crises: rising oil prices and shipping costs → rising inflation → monetary tightening → economic recession, confirming a stagflationary cycle → synchronized decline in stock fundamentals and valuations. This logic chain cannot be falsified in the short term. Simultaneously, we note a short-term concentrated withdrawal of funds that supported the "first phase of the rally": 1. Shrinking industry ETF sizes, particularly in the non-ferrous, chemical, computer, and media sectors.

- Absolute return funds are seeing their floating profits rapidly shrink, forcing them to reduce equity positions to avoid principal losses. Annuities, which had significantly increased their equity exposure earlier, are seeing the stability of their high positions decline in the short term. Referencing the holding structures of active public funds and "Fixed Income+" products, sectors such as non-ferrous, chemicals, communications, and electronics may all face pressure for position reductions. Allocation-based funds increased equity exposure in this round, with "Fixed Income+" products being an important channel, and short-term redemption pressure is beginning to manifest. With the concentrated withdrawal of funds, the implementation of steady and sustained growth policies is logical. Attention should be paid to potential differences between the structure of steady and sustained growth efforts and the structure of absolute return fund reductions (CSI 300 weight - industry ETF weight, CSI 300 weight - "Fixed Income+" holding weight). Overall index risk is controllable, but structural shocks may still pose tail risks.

Regarding mid-term projections, we explicitly disagree with the judgment that "short-term sharp decline, mid-term slow decline, and the major rally has ended." We believe the impact of the US-Iran conflict will likely see its greatest shock in the immediate future. Short-term market concentrated pricing of uncertainty and reductions by absolute return funds have amplified the adjustment phase. In the mid-term, the pessimistic projections that cannot be falsified in the short term actually involve at least three variables, making mid-term expectations likely to be significantly milder than short-term projections: 1. Facing imported inflation, the optimal choice for monetary policy in both China and the US is likely not tightening. China has a low inflation base, and rising oil prices fundamentally altering monetary policy is a low-probability event. Coupled with our mature policy framework for addressing structural economic issues, it is highly probable that China will not tighten. On the US side, household sector employment is weak, and the forces for an inflationary cycle are limited. In the 1970s, the US was an oil importer, whereas now it is a major oil exporter, making imported inflation pressures more controllable. Warsh needs to balance supporting household employment, promoting manufacturing reshoring (which requires a weak dollar, low interest rates, and low costs), and addressing imported inflation. Simply assuming that Warsh is relatively hawkish and will tighten in response to imported inflation cannot be falsified in the short term, but there may be a significant expectation gap in mid-term validation. 2. If a trend of tight monetary policy does not emerge, economic pressures in both China and the US will also be manageable. 3. In the mid-term, the impact of shifts in relative national power will become apparent, and the probability of China's Alpha materializing has substantially increased. In recent years, each major global shock has presented an opportunity for re-evaluating China's supply chain capabilities. In this round, China's ability to maintain energy security and supply chain security may be validated anew. This provides an opportunity for stock market narratives to return to a stronger state. We also note the possibility of Middle Eastern capital flowing into Chinese assets as a result. Short-term concerns do not equate to mid-term projections; the short term might be the worst period. Guarding against short-term liquidity shocks, we should maintain confidence and patience in the mid-term.

II. Mid-term: The A-share market is in a period of oscillation and consolidation between the "two-phase rally." Short-term: The market may follow a process of "oversold → steady and sustained growth policy implementation → rebound." Subsequently, it will likely remain in range-bound oscillation, with leading sectors continuing to rotate. In phases with new main theme opportunities (such as short-term rallies in energy storage and optical communications based on prosperity validation), the market may challenge the upper bound of the oscillation range; however, if the evolution of main themes is hindered after a rebound, the market may test the lower bound of the oscillation range.

III. Short-term: Recommendations continue to center on the "prioritize reality" structure, with CPO and energy storage being strong directions. Under the shock of energy costs, new energy and new energy vehicles benefit from energy diversification and trends towards energy supply resilience, potentially becoming important strategic resources alongside traditional energy. Additionally, for structures that are highly likely to participate in the "second phase of the rally" (AI industry chain + price increase cycle), dips can be utilized for positioning, though short-term timeliness is limited. We reiterate that based on historical experience, the style characteristics of the two-phase rally are consistent. During the intermediate consolidation phase, the style is not a rotation from high to low, but rather a broader diffusion of main themes. High-elasticity investment opportunities still primarily stem from the extension of main assets + the expansion of macroeconomic narratives.

At this stage, structural choices continue to "prioritize reality," with short-term prosperity validation confirmed for CPO and energy storage. Under the shock of energy costs, new energy and new energy vehicles benefit from energy diversification and trends towards energy supply resilience, potentially becoming important strategic resources alongside traditional energy; this could be a direction with expanding earning potential. The market has already identified the strongest structures; how to assess their sustainability? We believe the pattern of stock price performance, "industry catalysis → valuation increase rally → historically high valuations, rally falters," remains applicable. When the rally falters, there will be a period of sideways oscillation, which can be managed calmly. In addition to continuously identifying new segments with strong growth prospects, structures that are highly likely to be part of the second phase from a mid-term perspective are worth buying on dips, with a focus on the AI industry chain and cyclical Alpha. However, we objectively acknowledge that these directions have limited short-term timeliness.

Our mid-term style judgment remains unchanged. Historically, the style characteristics of the first phase of the rally (structural rally) and the second phase of the rally (comprehensive rally) are consistent. The intermediate consolidation phase is not characterized by a rotation from high to low or style switching, but rather by a broader diffusion of main themes.

We have reviewed historical experiences from 2014 and 2018-19. We observed that during the consolidation phase, previously strong styles adjusted and stabilized first, preceding the start of the second phase of the rally. Sector performance during the consolidation phase has a weak positive correlation with both the first phase of the rally (structural rally) and the second phase of the rally (comprehensive rally) (i.e., no distinct rotation in styles). Therefore, the consolidation phase is not about rotating from high to low or style switching; it is more about the dissipation of main themes. Leading sectors and core targets from before enter a high-level oscillation range. The space for discovering new opportunities decreases, and the scale diminishes, hence it is a consolidation phase. However, in such a scenario, high-elasticity investment opportunities still primarily stem from the extension of main assets + the expansion of macroeconomic narratives.

Mapped to the current situation, the characteristic of "prioritizing reality" will persist at least until the first-quarter earnings season. The subsequent evolution of the AI industry trend may shift from the hardware end toward the application end; focus on "picks and shovels" in the application layer (cloud computing, edge devices, robotics), the domestic AI chain catching up (major domestic manufacturer chains), and opportunities for AI to transform traditional industries (contrary to HALO trades). Expansion of macroeconomic narratives: focus on the possibility of strengthened pricing based on shifts in relative national power, which presents an opportunity for the revaluation of manufacturing.

Risk Warning and Disclaimer

Markets carry risks, and investments require caution. This article does not constitute personal investment advice, nor does it consider the specific investment objectives, financial situation, or needs of individual users. Users should consider whether any opinion, view, or conclusion in this article is suitable for their specific circumstances. Investment based on this is at your own risk.