When Oil Becomes "Gold"

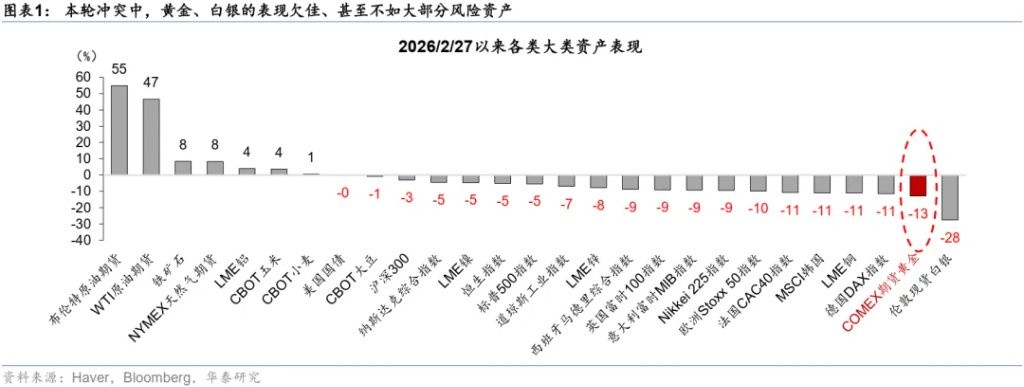

On February 28, the Middle East conflict escalated, and the market's pricing of the conflict's impact continued to update, with precious metals like gold underperforming compared to risk assets. Gold may become the "canary" for global cash flow pressures and material shortages, with short-term trends influenced by the situation in the Middle East. The conflict between the U.S., Israel, and Iran has heightened risk aversion, but in the medium to long term, it will strengthen global capital expenditure. The Strait of Hormuz is the epicenter of the conflict, carrying 60% of the Middle East's and 20% of the world's oil transport volume. A blockade would create a supply gap of over 10% in oil, affecting logistics for natural gas and chemical products. Energy shortages are intensifying, leading to price increases

On February 28, since the outbreak of the current Middle East conflict, the overall situation of the war has been escalating, and the market's pricing of the duration and impact of the conflict is continuously updating, with the probability distribution spreading from "short-term shock" to "medium-term disturbance." Generally speaking, in a stagflation environment, the dual attributes of safe-haven + anti-inflation allow precious metals like gold to perform well, but in this round, the performance of gold and others is even worse than most risk assets (Chart 1). This article explores the logic and certain inevitability of this divergence.

Gold may have become the "canary in the coal mine" under the trends of cash flow pressure, material shortages in Gulf countries, emerging markets, and even globally, with its short-term trend largely depending on the tension level of the Middle East situation. However, in the medium to long term, we maintain our allocation recommendation for scarce resources like gold as a hedge against the credibility of fiat currency. At the same time, although the US-Israel-Iran conflict temporarily boosts safe-haven sentiment, it will further strengthen the logic of global capital expenditure expansion and a significant increase in consumption in the medium to long term.

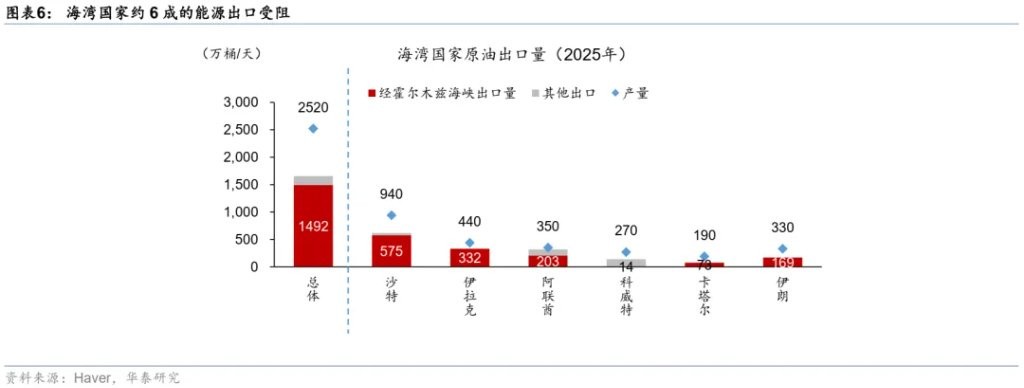

For the global economy, the "epicenter" of this conflict is the Strait of Hormuz. In the three years leading up to the US-Israel-Iran conflict, oil prices were generally in a downward channel, and the market had formed a consensus expectation of long-term supply and demand stagnation in oil. On February 27, the forward curve implied that the market expected the average annual price of Brent crude oil in 2026 to be around $70 per barrel, while the short end rose to $92 three weeks later, an increase of over 30%. However, the intensity of the conflict is still escalating. For the global economy, the "epicenter" of the conflict is the Strait of Hormuz—this strait, which is only 33 kilometers at its narrowest point, is easy to defend but hard to attack, carrying about 60% of the Middle East's and 20% of the world's oil transport volume. Even accounting for all possible mitigating measures, a blockade of the strait would still cause a "hard gap" of over 10% in oil supply. Additionally, the strait is crucial for the logistics of natural gas and a large number of chemical products, including fertilizers. In early March, the Strait of Hormuz was nearly completely blocked for the first time in history, and this shock will further worsen the "physical" shortages of global energy and other critical supplies. It is worth reiterating that the relationship between the duration of the blockade of the Strait of Hormuz and the degree of shortages and price increases of various materials may be nonlinear.

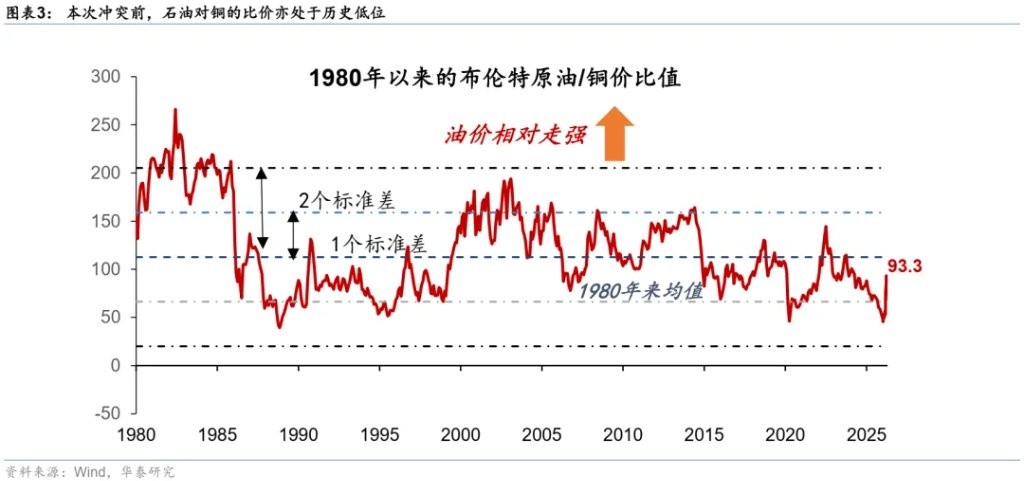

Three weeks into the US-Israel-Iran conflict, energy has become "gold." Here we take the most representative "energy" as an example, but the same logic can be extended to more key materials with physical shortages. In the short term, the probability of reopening the strait is decreasing. Currently, both the US and Israel are still signaling further escalation of confrontation, which not only threatens more military targets but may also substantially destroy a large amount of energy infrastructure in the Middle East, making the impact of the conflict long-term. It is noteworthy that since the conflict has only erupted for three weeks, many ships in transit have already exited the Strait of Hormuz, and their loading capacity has not been affected, with most countries globally having certain reserves of energy and critical materials. Therefore, many material supplies still have some buffer, but these buffers are rapidly disappearing—if the blockade of the strait is prolonged, the pressure of global material shortages will rise exponentially. Reflecting on the pandemic period, the "butterfly effect" when the highly globalized logistics system faced physical shocks is difficult to predict accurately, but it must be approached with great respect The physical shortage and relatively "inelastic" demand for energy further highlight its value compared to gold, which has lower demand elasticity, especially as the price ratio of oil to gold has already reached post-war extremes before this conflict (its "distortion" comparable to that during the 2020 pandemic, as shown in Charts 2 and 3).

For Gulf countries that have accumulated a large amount of gold through foreign exchange earnings in recent years (the "epicenter" of this conflict), as well as developing countries that previously purchased large amounts of gold driven by the trend of de-dollarization and rising gold prices (which are now marginally most affected and most vulnerable), cash flow depletion not only limits the funds available for gold purchases but also makes it reasonable to exchange the previously accumulated floating profits in gold for necessities at the current price ratio—this is why gold may become the "canary in the coal mine" under the impact of shortages—we will analyze this in detail below.

Why is gold no longer "gold" (in the short term)? Under the impact of stagflation, rising costs, material shortages, demand contraction, and cash flow pressures on various market participants occur. The first step in classic stagflation trading is to return cash. Historically, precious metals have performed well under geopolitical shocks due to their dual properties of being a safe haven and an inflation hedge. However, gold is not cash, and moreover, the price ratio between gold, cash, and today's "hard commodities" has reached an extreme level. The underlying logic is that the previous significant price increase means that the holdings of gold by various entities, especially central banks, have reached a twenty-year high. In a short-term environment of rapidly tightening cash flow, gold may face the dilemma of insufficient buying interest and increased selling pressure. The recent trends in gold prices can be attributed to the following four points:

-

Pressure to "devirtualize" under the impact of material shortages. As discussed above, under stagflation, "cash is king," and assets that have strong cash flows or even benefit from the situation are more resilient. Gold, however, lacks cash flow support, especially after a significant price increase and high accumulated floating profits; in terms of pricing, gold's pricing against geopolitical risks is more fully reflected than other "hard shortage" materials. In the current environment, the stability of gold holdings is clearly not as strong as that of more scarce commodities with more certain cash flows.

-

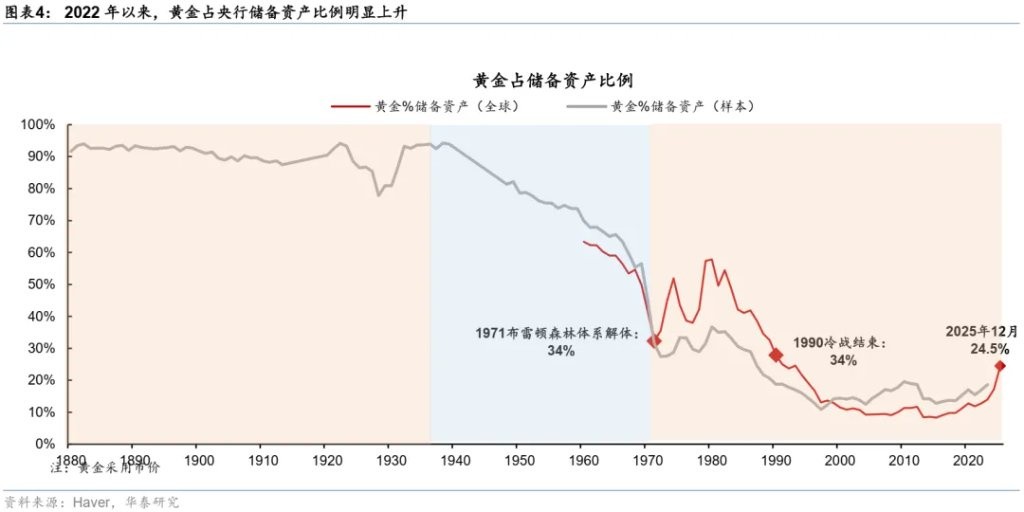

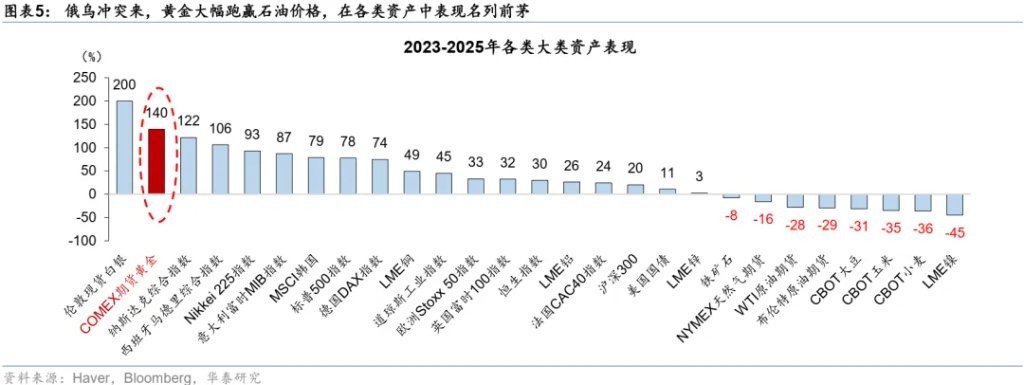

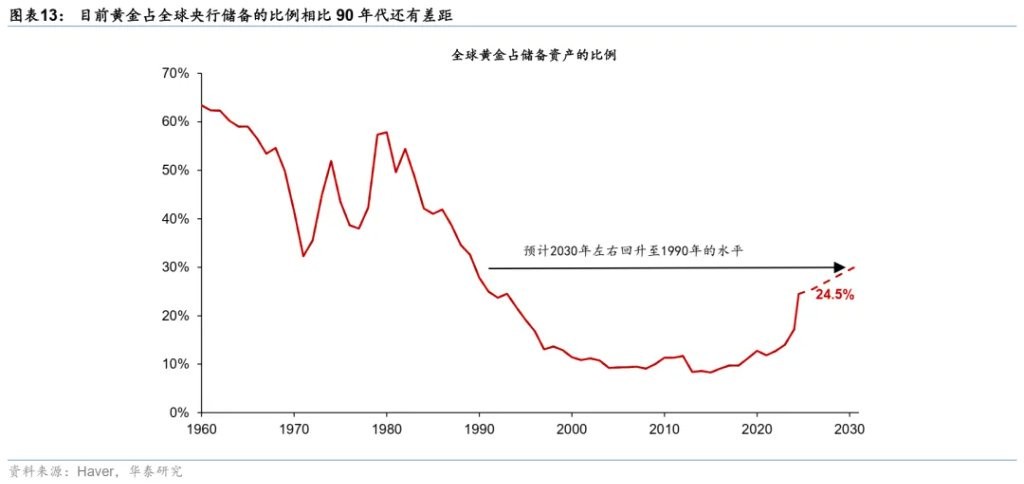

High positions + high floating profits make short-term gold holdings prone to decline and difficult to rise. Since 2022, global central bank gold purchases have accelerated significantly, prompting the private sector to join in. We estimate that from 2022 to 2025, the annual gold purchase volume by global central banks will be twice that of the previous ten years. Coupled with the significant rise in gold prices, the proportion of gold in central bank reserve assets has increased from 12.8% in 2020 to 24.5% in December 2025 (Chart 4). From 2023 to 2025, the price ratio of gold to oil has increased by 3.1 times, ranking among the top in various asset classes (Chart 5). However, when gold is not a "necessity," and marginal buyers, such as Gulf countries and emerging market countries, face significant cash flow pressures, the short-term supply-demand balance is unfavorable for gold prices.

-

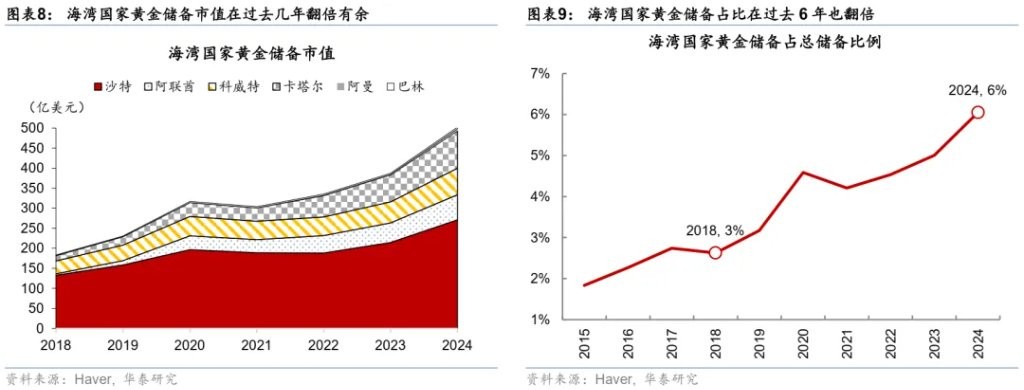

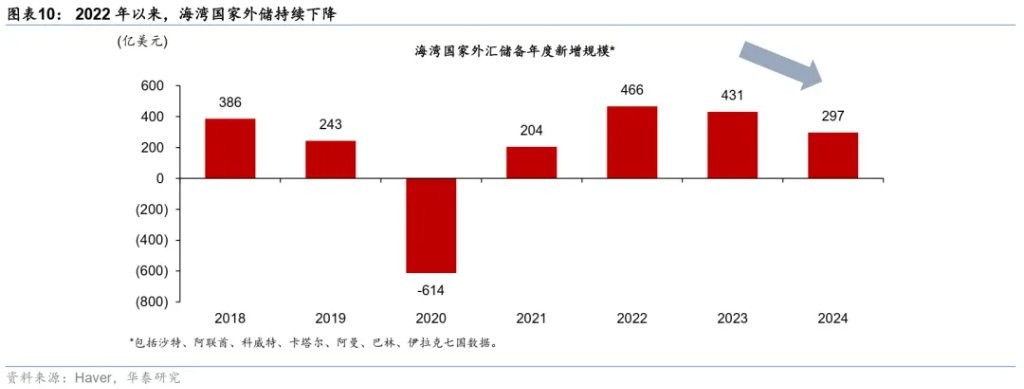

Short-term disruptions in the oil dollar cycle may break the gold supply-demand balance. Unlike previous energy crises, the cash flow of Gulf countries has been physically cut off and may turn negative, potentially worsening the gold supply-demand balance. As we mentioned, past oil shortages have instead increased the relative pricing power of Gulf countries' export commodities In this conflict, the Strait of Hormuz has been essentially blocked for the first time in history, threatening oil and gas infrastructure, leading to a sharp decline in the income of Gulf countries, and the circulation of petrodollars is likely to be significantly obstructed. If the conflict lasts for a longer period, the substantial reduction in petrodollars may increase the risk of dollar shortages, further pushing up the dollar as a safe haven and tightening liquidity. As shown in Chart 6, approximately 60% of Gulf countries' exports are obstructed in terms of energy, while in previous years, the decline in oil prices combined with accelerated domestic infrastructure investment has left little "redundancy" in cash flow. Over the past few decades, Gulf countries have exchanged energy and other raw materials for dollars and invested in other regions globally. The net foreign investment position of Gulf countries is $2 trillion, with gold positions being one of the fastest-growing, most recently floating profits (i.e., reducing holdings without realizing losses), and the configuration with the most significant short-term and oil price ratio increase (Chart 7). The market value and proportion of gold reserves in Gulf countries have more than doubled in the past six years (Charts 8-9). The two peculiarities of this round of shocks are: 1) cash flow in Gulf countries is blocked, and 2) in recent years, gold positions and floating profits have significantly increased, making this round of gold prices a "canary in the coal mine" for the economic pressure on Gulf countries.

-

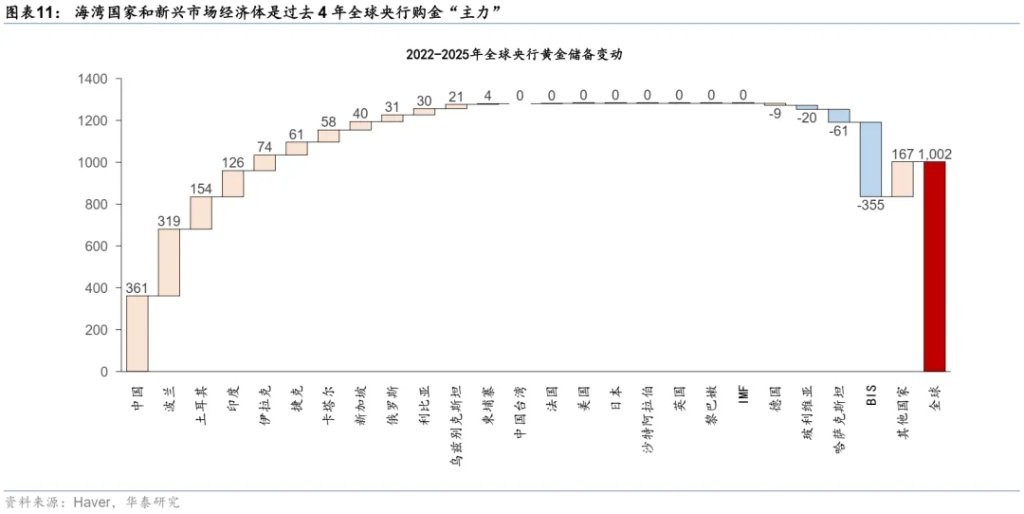

Global developing countries (previously the main buyers of gold) are unlikely to continue purchasing gold in the short term, and may even face "emergency" pressure. As shown in Chart 11, Gulf countries and emerging market economies have been the main buyers of gold by global central banks over the past four years. However, in this shock, emerging market countries are under the greatest overall pressure (with a few energy-exporting countries as exceptions). As we demonstrated in "First Release: Daily Monitoring System of 'Pressure Value' in Middle East Conflict (March 19)" (2026/3/20), many developing countries, especially in Southeast Asia, South Asia, Africa, and countries around the Gulf, have begun to implement relatively strict demand control policies under the dual pressure of rising costs and currency (purchasing power) depreciation. Chart 12 shows the multiple vulnerabilities faced by developing countries and their quantitative indicators. Meanwhile, if the rapid deterioration of external accounts and domestic fiscal conditions continues for a period, a decline in gold purchasing power cannot be ruled out, and even marginal selling pressure may emerge. After all, the relative scarcity of gold and "butter" will change with the fluctuations in price ratios and shortages, and may even temporarily reverse.

In summary, if the conflict escalates further and the Strait of Hormuz remains blocked, gold buying pressure is unlikely to recover in the short term, and short-term selling pressure may continue to rise. Therefore, under the premise that the oil and raw material infrastructure in the Gulf region is not decisively damaged, we consider the reopening of the Strait as a prerequisite for stabilizing gold prices.

In the short term, the dollar is strong; in the long term, gold allocation still has value. In the medium to long term, the conflict between the U.S., Israel, and Iran will not only not weaken but will instead strengthen several logics of de-dollarization and even the loosening of fiat currency "valuation anchors"—① the unsustainability of global finances will continue to rise; ② the foundation of dollar reserves will accelerate its loosening; ③ geopolitical risk premiums will further increase. Although the proportion of gold in global central bank reserves has rapidly increased, there is still a significant gap compared to the 1990s (Chart 13). More importantly, whether looking at the actual subsequent trends of historically high-intensity military conflicts or logical deductions, the price ratio of gold and other precious metals relative to fiat currencies is still expected to rise On one hand, the costs of conflict and the demand for reserves are driving the impulse for fiscal expansion (as U.S. Secretary of Defense Lloyd Austin proposed an additional budget of $200 billion last week). In the context of global fiscal sustainability being questioned, conflicts undoubtedly exacerbate global fiscal deficits. Furthermore, in the backdrop of a restructuring global order, with the U.S. withdrawing from global governance and potentially becoming a source of global geopolitical "volatility," it is reasonable for governments around the world to continue reducing their dollar assets in the medium to long term, supporting their own re-industrialization and re-militarization.

Risk Warning: U.S. attacks on Iranian power plants, Iran's unexpected counterattacks, and further escalation of the situation; the duration of the blockade of the Strait of Hormuz exceeds expectations.

Risk Warning and Disclaimer

The market has risks, and investment should be cautious. This article does not constitute personal investment advice and does not take into account the specific investment goals, financial situation, or needs of individual users. Users should consider whether any opinions, views, or conclusions in this article are suitable for their specific circumstances. Investment based on this is at one's own risk