When will the oil price shock trigger a real crisis? History reveals three major triggering signals

Deutsche Bank believes that historically, a true oil price crisis that triggers a more than 15% drop in U.S. stocks must meet one of three conditions: a sustained oil price surge of 50%-100%, a macroeconomic slide into recession, or the central bank being forced to aggressively raise interest rates. Currently, none of these three conditions have been triggered, WTI oil prices remain below the average for 2024, and the S&P 500 is only down 1.4% from its historical high

The situation in Iran is turbulent, and oil prices have risen sharply for several consecutive days, causing market nerves to tighten again, with heightened attention on whether the impact will further spread.

According to the Chase Wind Trading Desk, Deutsche Bank macro strategist Henry Allen pointed out in a recent research report: Historically, the current rise in oil prices alone has never been sufficient to trigger a sustained market crisis. The oil price shocks that have caused U.S. stocks to drop more than 15% have historically required one of the following three conditions to be met:

Significant and sustained oil price surge: An increase of at least 50% to 100%, maintained for several months;

Substantial damage to the macro economy: An oil price shock sufficient to push an already slowing economy into recession;

Central banks forced to adopt a hawkish stance: Inflationary pressures compel major central banks like the Federal Reserve to raise interest rates significantly.

Currently, none of the above three conditions have been triggered. Deutsche Bank clearly indicates that this is a dynamically evolving situation, and the next few days to weeks will be a critical window period:

Current oil price shock is of "moderate to low" magnitude

Brent crude oil rose +7.3% in a single day on March 2, marking the largest single-day increase since March 2022, leading to declines in European bonds and stock markets. However, when this volatility is viewed in a longer historical context, the conclusions are quite different:

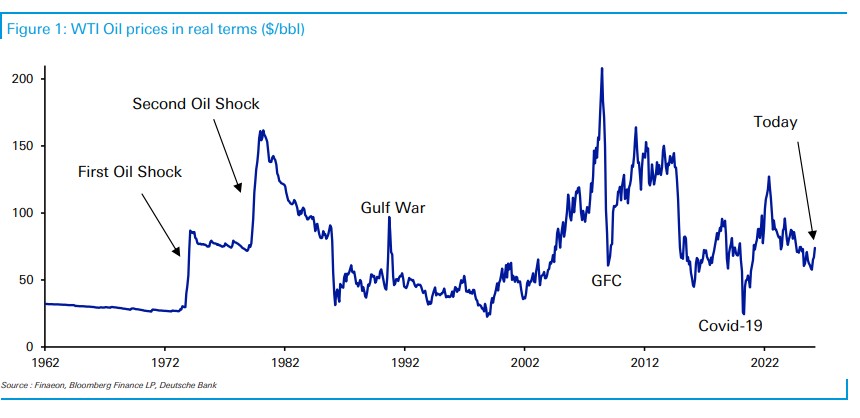

The absolute level of WTI oil prices is still below the average price for 2024 (USD 75.8/barrel), far from the price levels seen during major historical crises; since 1990, there have been 55 instances of single-day increases of this magnitude, which is not a rare event;

European natural gas prices also recorded the largest single-day increase since 2022, but the absolute price level is still far below the peak in 2022 and has not yet returned to the highs of 2025.

The S&P 500 index actually rose slightly on Monday, down only 1.4% from its historical high; this stands in stark contrast to the market's rapid entry into a bear market following the outbreak of the Russia-Ukraine conflict in 2022.

Deutsche Bank concludes that the current oil price fluctuations are historically classified as "moderate to low" magnitude and do not constitute triggering conditions for systemic risk.

Common codes of four historical oil price crises

Deutsche Bank studied all significant cases where oil price shocks evolved into more than 15% deep pullbacks in the S&P 500 and distilled three common characteristics:

Condition 1: Oil price increases of at least 50% to 100%, sustained for several months

- 1973 Oil Crisis: OAPEC implemented an oil embargo, causing oil prices to nearly quadruple, leading the U.S. and the U.K. into recession, with the S&P 500 plummeting over 40% within a year.

- 1979 Iranian Revolution and Iran-Iraq War: Oil prices doubled again, with a significant decline in Iranian production capacity, leading to sustained supply shocks.

- 1990 Gulf War: After Iraq invaded Kuwait, oil prices more than doubled, and the S&P 500 fell 19.9% between July and October 1990

- In 2022, the Russia-Ukraine conflict caused Brent crude oil to soar from about $80 per barrel at the beginning of the year to a closing price of $128 per barrel on March 8, an increase of approximately 60%.

Condition Two: The macroeconomy faces substantial shocks, and the risk of economic downturn significantly rises

The oil price shock is not an isolated event. In 1990, the Federal Reserve had already completed a round of interest rate hikes from 1988 to 1989, and economic growth was already slowing. At this point, the oil price shock became the last straw that broke the camel's back, pushing the United States into recession. Research reports emphasize that there has not yet been a substantial deterioration in data terms— even if there was a brief panic of recession in the summer of 2024, the market quickly stabilized.

Condition Three: Central banks are forced to turn hawkish, significantly raising interest rates to combat inflation

In 1979, then-Federal Reserve Chairman Paul Volcker initiated an unprecedented monetary tightening cycle, compounded by the oil price shock, leading the United States into recession in early 1980, with the S&P 500 dropping 17% again. In 2022, it was the aggressive interest rate hike cycle of the Federal Reserve resonating with the oil price shock that resulted in the S&P 500 experiencing its first consecutive three-quarter decline since the financial crisis.

Currently, the market pricing for interest rate hikes by the Federal Reserve or the European Central Bank remains a "tail risk" rather than a baseline scenario, far from the hawkish levels seen in the historical cases mentioned above