Overseas market explosion, MiniMax's revenue in 2025 increased by 158.9% year-on-year, adjusted net loss expanded by 2.7% year-on-year to USD 250 million, gross margin significantly improved | Financial report insights

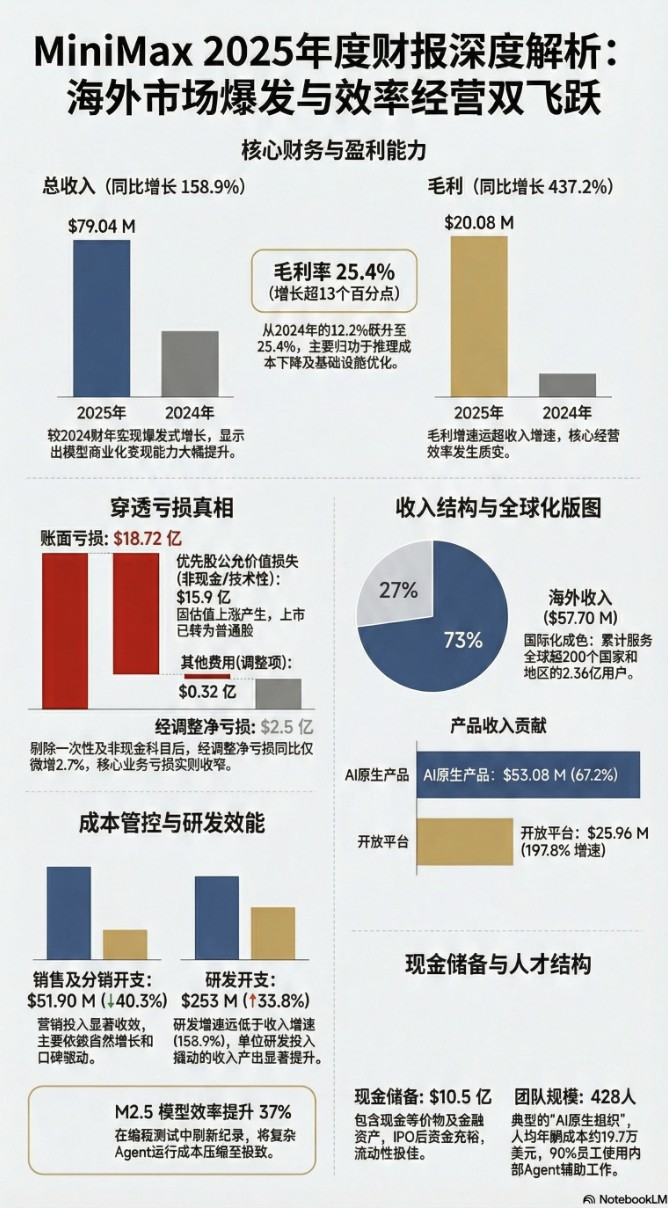

In MiniMax's revenue structure: AI products account for 67.2%, and the open platform accounts for 32.8%; overseas revenue accounts for 73%. The company reported a loss of $1.872 billion, primarily due to the issuance of convertible preferred shares before the company's IPO, which is reflected as financial liabilities. The surge in valuation led to a significant paper loss, with the adjusted net loss being $250 million, essentially flat compared to last year's $244 million

MiniMax released an impressive annual performance announcement on March 2, 2026. In the fiscal year 2025, the company's total revenue increased by 158.9% year-on-year to $79.04 million, with gross profit surging by 437.2% to $20.08 million, and the gross margin doubled, demonstrating a dual improvement in the company's model efficiency and business monetization capability.

On the financial statements, the company reported a loss of $1.872 billion for the year, primarily due to a fair value loss on preferred stock amounting to $1.59 billion. This represents the "technical cost" of the company's continuously soaring valuation on the financial statements. Currently, the preferred stock has automatically converted into common stock, and this non-cash accounting loss has become history.

Excluding stock-based compensation, fair value losses on preferred stock, and listing expenses, the adjusted net loss for 2025 was $250 million, essentially flat compared to $244 million the previous year, with a year-on-year increase of only 2.7%.

From a strategic perspective, MiniMax's internationalization is particularly prominent. In 2025, revenue from regions outside mainland China accounted for 73% of total revenue, serving over 236 million users across more than 200 countries and regions, with 214,000 enterprise clients and developers spread across over 100 countries and regions.

On the technical front, the company has built a globally competitive model matrix across multiple modalities including language, video, voice, and music, and the M2.5 released in February 2026 set a new industry record in programming benchmark tests.

Revenue Structure: AI Native Products Dominate, Open Platform Grows Even Faster

In 2025, MiniMax's revenue sources were mainly divided into two major segments: AI native products contributed $53.08 million, accounting for 67.2% of total revenue, with a year-on-year growth of 143.4%, driven by increased user willingness to pay and the continued commercialization of products like Hai Luo AI.

The open platform and other AI-based enterprise services contributed $25.96 million, accounting for 32.8%, with an even more rapid year-on-year growth rate of 197.8%, primarily benefiting from a significant expansion in the number of paying enterprise clients.

It is noteworthy that the growth rate of the open platform has surpassed that of AI native products, with the revenue share gap narrowing from 71.4% to 28.6% in 2024 to 67.2% to 32.8% in 2025, reflecting the company's accelerating commercialization towards enterprise B-end business catching up with C-end consumer business.

By region, revenue from mainland China accounted for 27%, while overseas revenue accounted for 73%. This revenue structure implies both a larger market space and higher exchange rate fluctuations and cross-market compliance complexities.

Significant Improvement in Gross Margin: Efficiency Enhancement is the Core Logic

In 2025, the gross margin jumped from 12.2% in 2024 to 25.4%, an increase of over 13 percentage points, surpassing the 158.9% revenue growth rate, which is not an easy feat in the AI foundational model industry The company attributes this to the continuous improvement in model and system efficiency, as well as the optimization of infrastructure configuration. In short, the cost of inference is decreasing, while the maintenance or even increase of revenue per unit price has driven the continuous expansion of gross profit margins.

At the same time, the company's sales and distribution expenses have been significantly compressed against the trend, plummeting by 40.3% from $87 million in 2024 to $51.9 million in 2025.

Management explained that the AI-native product business is primarily driven by natural growth and word-of-mouth, allowing for a significant reduction in marketing investment. This combination of "cost reduction" and "efficiency improvement" serves as a dual engine for the improvement of gross margins.

Continued High Investment in R&D, Significant Efficiency Improvement

In 2025, R&D expenses amounted to $253 million, a year-on-year increase of 33.8%, making it the company's largest expense item, mainly used for basic model iteration, multi-modal capability development, and cloud service training.

However, the key comparative signal is that the growth rate of R&D expenses (33.8%) is far lower than the revenue growth rate (158.9%) during the same period, indicating a significant increase in revenue output per dollar of R&D investment, which is a necessary condition for AI companies to move towards scalable profitability.

In terms of model progress, in the fourth quarter of 2025, the company successively updated three language models: M2, M2.1, and M2-her, with M2 becoming the first Chinese model on OpenRouter to exceed 50 billion daily token consumption, topping the global hot list on HuggingFace.

The M2.5 released in February 2026 set a new industry record in the SWE-Bench Verified programming test, with a 37% efficiency improvement over the previous generation, and reduced the operating cost of complex agents to the extreme level of "10,000 dollars allowing 4 agents to work continuously for a year."

Breakdown of Huge Book Losses: Fair Value Loss of Preferred Shares as "Valuation Tax"

The $1.872 billion book loss for the year needs to be understood in terms of its composition. Among them, the fair value loss of financial liabilities reached $1.59 billion (compared to $214 million the previous year), making it the largest source of loss. This loss stems from:

The convertible redeemable preferred shares issued by MiniMax during the pre-IPO financing stage, which must be measured at fair value according to international financial reporting standards. The higher the company's valuation, the larger the book value of this "liability," and the corresponding loss also increases.

In other words, this loss of nearly $1.6 billion is essentially a "mark" left on the financial statements by the rapid surge in the company's valuation and does not represent actual cash outflow.

As the company officially went public on January 9, 2026, the $3,597,566 thousand of convertible redeemable preferred shares automatically converted into common stock, eliminating this from the liability side, and this distorting item will no longer appear in future financial reports.

This is also why investors need to look beyond the surface loss figures and focus on the adjusted net loss ($250 million).

Ample Cash, IPO Fundraising for Supplementation

As of December 31, 2025, the company's cash reserves reached $1.05 billion, including $508 million in cash and cash equivalents, $509 million in financial assets measured at fair value, and restricted cash, time deposits, etc., further increasing from $881 million at the end of the previous year In January 2026, the IPO and the exercise of the over-allotment option amounted to approximately HKD 5.293 billion (about USD 680 million) in net fundraising for the company, further strengthening its financial reserves and laying the financial foundation for subsequent model development and global expansion.

Regarding the debt-to-equity ratio, as of December 31, 2025, it stood at 343.3% (a significant increase from 187.8% at the end of the previous year), but this was primarily driven by preferred stock liabilities. As the preferred stock converts to equity post-IPO, this ratio will fundamentally improve.

The company's management also clearly stated in the financial report that post-IPO liquidity is sufficient, and operations will be conducted based on a going concern basis.

Streamlining Personnel but High Compensation: AI Native Organization Strategy Enhances Efficiency

As of December 31, 2025, MiniMax had only 428 full-time employees, but employee compensation expenses (including stock-based payments) amounted to USD 84.3 million, a 54% increase from USD 54.6 million the previous year, with an average annual salary cost of approximately USD 197,000, reflecting an elite personnel structure.

At the same time, the company is advancing its "AI Native Organization" transformation. Internal Agent interns have covered nearly 90% of employees, encompassing core functions such as programming development, data analysis, operations management, human resources recruitment, and marketing sales, and in January 2026, it will productize its accumulated capabilities by launching the MiniMax Agent AI-native Workspace.

This strategy serves not only as an external product output but also as a core mechanism for improving internal efficiency and compressing marginal costs.