Deutsche Bank: If navigation through the Strait of Hormuz is disrupted, Asia's energy supply will be severely impacted, with Japan and South Korea being the most affected!

Deutsche Bank warns that 89% of the crude oil flowing through the Strait of Hormuz goes to Asia, and a disruption would have an extremely asymmetric impact on Asia. Japan and South Korea, with energy import dependence rates of 87% and 81% respectively, are the most vulnerable. The Asian foreign exchange market has already begun to feel the tremors

Deutsche Bank warns that the Strait of Hormuz, as the world's most important energy chokepoint, carries about 20% of the world's total oil consumption and 20% of liquefied natural gas (LNG) supply, and currently there are almost no viable alternative shipping routes.

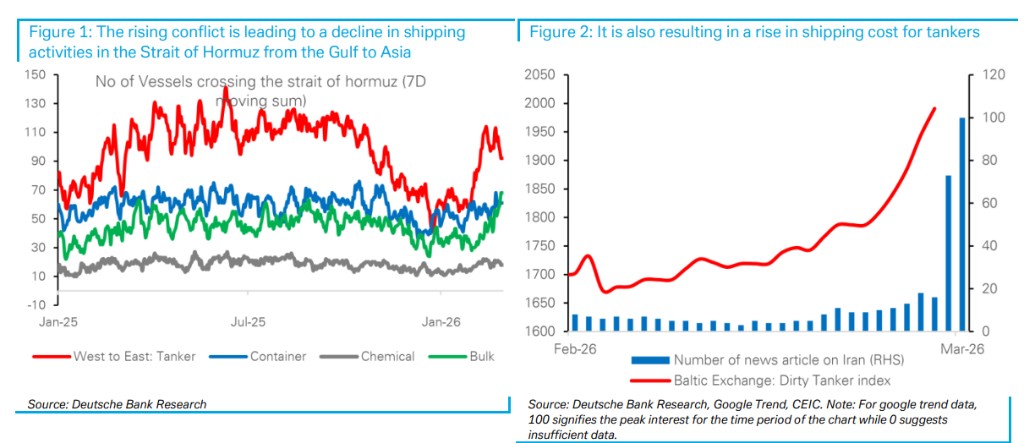

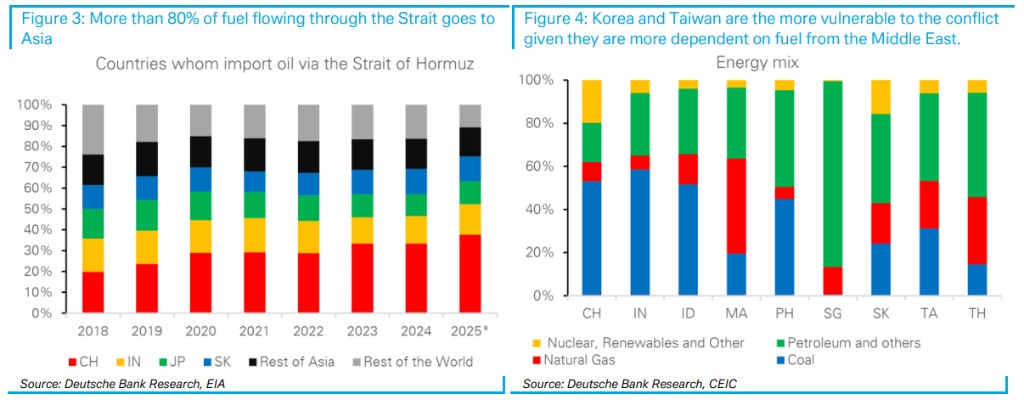

After the joint military action by the US and Israel, the Iranian Navy announced a ban on vessels passing through the Strait of Hormuz. Although Tehran has not issued an official national statement, the threat of a blockade has credibly driven down transit shipping volumes and rapidly increased transportation costs—this trend has already begun to show in the market.

Among all Asian economies, Japan and South Korea will be the most affected. Japan relies on imports for 87% of its total energy consumption, while South Korea's dependence is as high as 81%, with over 70% of both countries' imported crude oil coming from the Middle East, most of which must be transported through the Strait of Hormuz. Deutsche Bank believes that the high dependence on imports means that Japan and South Korea's energy security is more vulnerable in this round of crisis, and if supply shocks persist, it will pose a significant threat to the economic operations of both countries.

The Asian foreign exchange market has shown predictable weakness, with risk-sensitive currencies such as the South Korean won, Australian dollar, and Malaysian ringgit under significant pressure. Deutsche Bank currently maintains its existing foreign exchange strategy portfolio, holding short positions on the US dollar against the South Korean won, Indian rupee, and Malaysian ringgit, and views Malaysia as the biggest beneficiary of rising oil prices in the region.

Strait of Hormuz: An Irreplaceable Global Energy Lifeline

Deutsche Bank points out that historical experience shows that credible blockade threats alone are sufficient to drive shipping activity to contract and transportation costs to rise, and the current market has clearly felt this effect—transit shipping numbers are decreasing, and tanker transportation costs continue to rise.

Deutsche Bank cites data from the US Energy Information Administration (EIA) emphasizing that about 20% of the world's total oil consumption and 20% of LNG supply pass through this extremely narrow waterway, and currently, there are almost no practical alternative shipping routes.

This structural characteristic means that any threat of a shutdown of the Strait of Hormuz will have a profound impact on the global energy supply landscape, rather than just a regional disturbance.

Asia Faces 80% of the Impact: High Concentration of Energy Dependence

Deutsche Bank's report clearly states that a shutdown of the Strait of Hormuz would have an extremely asymmetric impact on Asia.

According to Deutsche Bank's estimates, about 89% of the crude oil and condensate passing through the strait ultimately flows to Asia; approximately 81% of LNG is delivered to Asia. Asia's dependence on this passage for energy is far greater than any other region.

Within the region, Japan, South Korea, and India are the main destinations, collectively accounting for a significant share of the total crude oil and LNG passing through the strait. This highly concentrated pattern means that once the strait is closed, Asia will face a severe energy supply gap, and it will be nearly impossible to compensate for it in the short term through alternative shipping routes Deutsche Bank emphasized that although some Asian countries have a larger absolute volume of imports, the risks faced by Japan and South Korea are more pronounced in terms of the vulnerability of energy security, due to their overall high dependence on imported fossil fuels.

Specifically, Japan's total energy consumption is as high as 87% from imports, while South Korea is at 81%, and India is only 35%. More critically, over 70% of the crude oil imported by Japan and South Korea comes from the Middle East, most of which must pass through the Strait of Hormuz.

In terms of energy reserves, South Korea has about 52 days of natural gas reserves and 60 to 70 days of crude oil reserves, which are relatively ample; however, once shipping disruptions persist, this buffer space remains limited. Deutsche Bank believes that sustained supply interruptions will have a substantial impact on the energy security and economic stability of both Japan and South Korea.

Macroeconomic Impact: Regional Differentiation Effect of Rising Oil Prices

Deutsche Bank stated that if the Strait of Hormuz is closed for an extended period, oil prices will continue to face upward pressure. Based on a scenario analysis of a 10% increase in oil prices, Asian economies will show significant differentiated impacts.

In terms of the current account, Thailand, the Philippines, and South Korea will experience the most significant negative shocks, closely related to the high dependence of these three countries on oil imports.

In terms of inflation transmission, South Korea, Singapore, the Philippines, and Thailand will be the most sensitive—this is mainly due to the fuel pricing mechanism linked to the market in these countries, allowing fluctuations in international oil prices to be transmitted more quickly and directly to end consumer prices. Deutsche Bank also pointed out that some countries can partially alleviate inflationary pressures through tax reductions, such as South Korea and Thailand.

Foreign Exchange Market Strategy: Malaysian Ringgit Benefits, Korean Won Faces Pressure but Support Remains

Deutsche Bank noted that after the market opened, Asian currencies have shown predictable weakness, with risk-sensitive currencies like the Korean Won, Australian Dollar, and Malaysian Ringgit under the most pressure.

In terms of specific positions, Deutsche Bank currently maintains short positions on the US Dollar against the Korean Won, Indian Rupee, and Malaysian Ringgit. Regarding the Korean Won, Deutsche Bank believes that seasonal factors (the natural slowdown in fuel demand entering the second quarter), a strong export cycle for electronic products, and a market position structure that is not overly long all provide important support; however, Deutsche Bank also admitted that if overall risk sentiment deteriorates significantly, it will consider exiting this position at an opportune time