AI turmoil, geopolitical escalation... panic is everywhere, but the most dangerous is private credit?

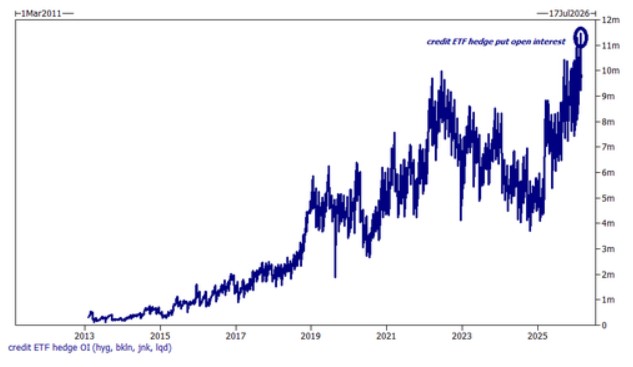

Goldman Sachs trader Garrett pointed out that among all the panic signals, the "retreat" in credit is the most concerning. The panic sentiment, which was previously limited to long and short books, has gradually permeated to the index level and ultimately transmitted to the credit market. The CDX investment-grade credit spread widened by 5 basis points in a single week, marking the largest weekly increase since last summer, and the open contracts for credit ETF hedging positions have risen to historical highs

Every corner of the market is sounding alarms, but Goldman Sachs' derivatives team believes that the most concerning risk does not stem from the violent fluctuations of tech stocks or the impacts of geopolitical conflicts, but rather from the quietly spreading cracks in credit.

Goldman Sachs derivatives trader Brian Garrett wrote in the latest weekend report that February felt "like a year"—the market evolved from the turbulence of individual stocks to turmoil at the index level, ultimately leading to the first "retreat" in the credit market: the CDX investment-grade credit spread widened by 5 basis points in a single week, marking the largest weekly increase since last summer, and the open contracts for credit ETF hedging positions reached an all-time high. Garrett candidly stated, "Among all these signals, the credit 'retreat' worries me the most."

Meanwhile, the pressures in the private credit market have begun to transmit to the public market. On Friday, the U.S. banking sector experienced its most severe decline of the year, with the KBW Bank Index dropping as much as 6% during the day, marking the largest single-day drop since the trade turmoil in April of last year.

Several private credit funds are facing liquidity issues, and even Goldman Sachs has had to send letters to investors to "prove its innocence," attempting to soothe market sentiment.

Panic signals are everywhere in the market, but retail investors remain calm

Garrett pointed out that signs of panic and contagion have "become impossible to hide in plain sight," yet retail investors seem oblivious—he mentioned in the report that he hears competitors say almost daily that "retail demand is at the 100th percentile for this historical period."

From specific indicators, the current level of market pressure is not to be underestimated. The index skew remains at multi-year highs; the implied volatility of individual stocks relative to the index has risen to the highest level since the 2008 global financial crisis; the open contracts for credit ETF hedging positions have also set a historical record.

Garrett noted that the -20% put options for a three-month term on the NDX can currently fully cover the cost of the +10% call options for the same term, indicating that the Nasdaq's one-month put/call skew is approaching the steepest level since the COVID-19 pandemic, providing relatively attractive structural opportunities for investors willing to bet on a rebound.

Hedge funds accelerate withdrawals, with tech and cyclical sectors hit hardest

Goldman Sachs' prime brokerage data shows that U.S. stocks have experienced net selling for the second consecutive week, and the pace of selling is accelerating, with both long and short positions being liquidated. The speed of hedge funds' net selling of individual U.S. stocks has reached the fastest level since the trade turmoil in April of last year.

At the sector level, the divergence is very pronounced. The technology, media, and telecommunications (TMT) sectors have faced net selling for the second consecutive week, with selling pressure particularly pronounced in software and the semiconductor and semiconductor equipment sectors, which intensified after Nvidia's earnings report on Thursday. All cyclical sectors in the U.S., including energy, materials, industrials, financials, and real estate, have experienced net selling, reaching -1.9 standard deviations from the five-year average In contrast, the healthcare sector has seen net buying from hedge funds for the second consecutive week, with long positions significantly outpacing short sales (approximately a ratio of 3.5 to 1). Currently, hedge funds are overweight in healthcare stocks by more than 12 percentage points compared to the Russell 3000 index, marking the highest level in five years. Consumer staples is another sector that has experienced net buying this year, highlighting its defensive attributes.

Credit Crack: From Private Equity to Public Markets

The most concerning transmission chain is taking shape amid this round of market turmoil. Garrett points out that the panic that was previously confined to long-short books has gradually permeated to the index level and ultimately transmitted to the credit market. Historical data shows that the last time CDX investment-grade spreads traded in the 50 median range, the S&P 500 index was approximately 1500 points lower than its current level.

The pressure in the private credit market is particularly concentrated. According to a previous article from Wall Street Insight, several private credit funds have encountered liquidity issues, with credit risk and equity risk showing a significant decoupling in recent days.

In the face of market panic, Goldman Sachs issued a detailed letter to investors on Thursday, endorsing its largest private credit fund aimed at retail investors. The letter indicated that Goldman Sachs Private Credit has an exposure of approximately 15.5% to enterprise software, which is relatively low compared to peers; the redemption rate for the fourth quarter is 3.5%, below the industry average.

Vivek Bantwal, Co-Head of Global Private Credit at Goldman Sachs Asset Management, stated in a subsequent conference call on Friday that diversified funding sources can sustain capital deployment throughout the cycle. He also admitted, "If we fully bet on the retail channel, the pace of scale expansion would obviously be faster."

"Heavy Assets, Low Obsolescence": Goldman Sachs Bets on a New Narrative

Amid the market's severe fluctuations, Garrett also provided his directional judgment, expressing agreement with the "HALO" investment logic—Heavy Assets, Low Obsolescence.

He quoted a market perspective in his report: “For the past 20 years, the investment community has operated under the assumption that light assets outperform heavy assets, software outperforms shovels, and code outperforms copper wire, allowing winners to expand almost infinitely at zero marginal cost... This logic is reversing, and it is reversing quickly.”

Garrett believes that the capital expenditure of up to $740 billion in 2026 will inevitably have its flow, and beneficiaries with real fundamentals will stand out.

At the ETF level, demand for the equal-weight S&P 500 fund (RSP) remains strong. Garrett noted that many portfolios currently seek to maintain equity exposure while avoiding excessive concentration in the "seven giants." The assets under management of RSP have grown nearly 30% in the past three months, reaching approximately $90 billion, about twice the size of the Dow Jones Industrial Average ETF (DIA)