HP's Q1 revenue grew by 7%, exceeding expectations, but the rise in storage chip prices dragged down performance outlook, causing a nearly 7% drop in after-hours stock price | Earnings report insights

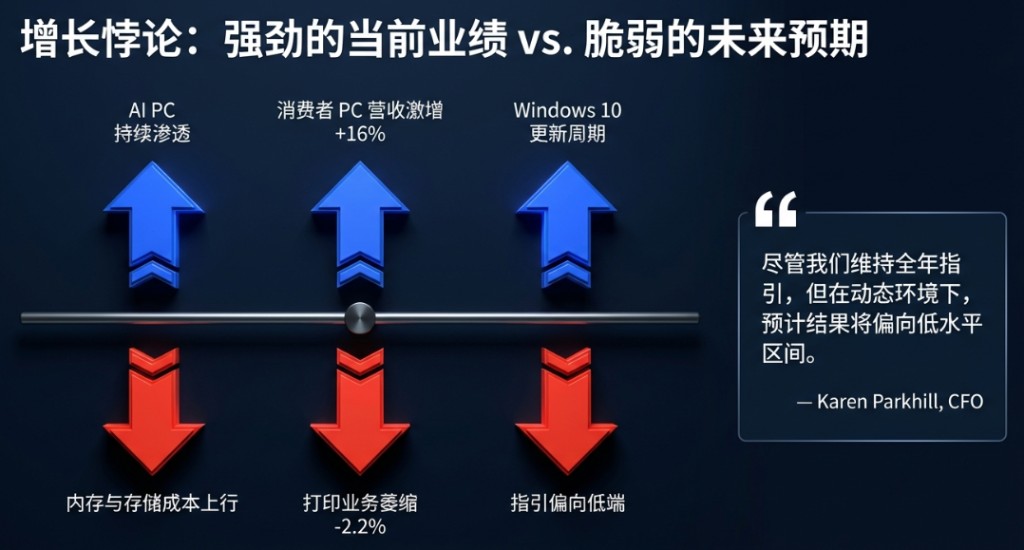

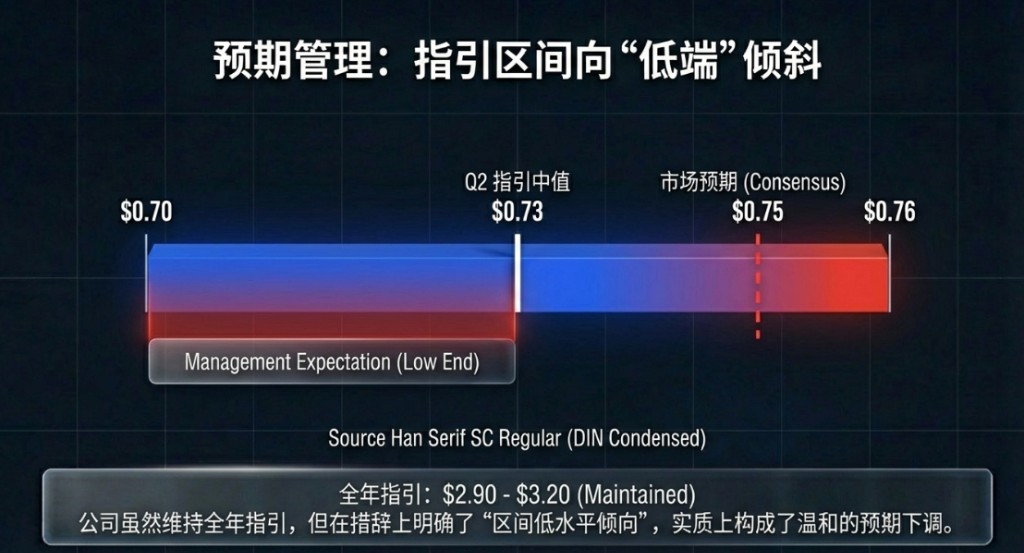

惠普 2026 财年第一财季净营收 144.4 亿美元,同比增长 6.9% 超分析师预期。然而公司预计第二财季非 GAAP 每股收益区间为 0.70 至 0.76 美元,中值 0.73 美元低于市场预期的 0.75 美元。CFO Karen Parkhill 直言,随着内存成本持续上行,公司虽维持全年指引,但预计实际结果” 将偏向低水平区间”。

惠普发布 2026 财年第一财季业绩,净营收 144.4 亿美元,同比增长 6.9%,较分析师预期的 139 亿美元高出约 3.2%;非 GAAP 每股收益 0.81 美元,较上年同期的 0.74 美元增长 9.5%,亦超出市场共识预期 0.77 美元约 5.3%。

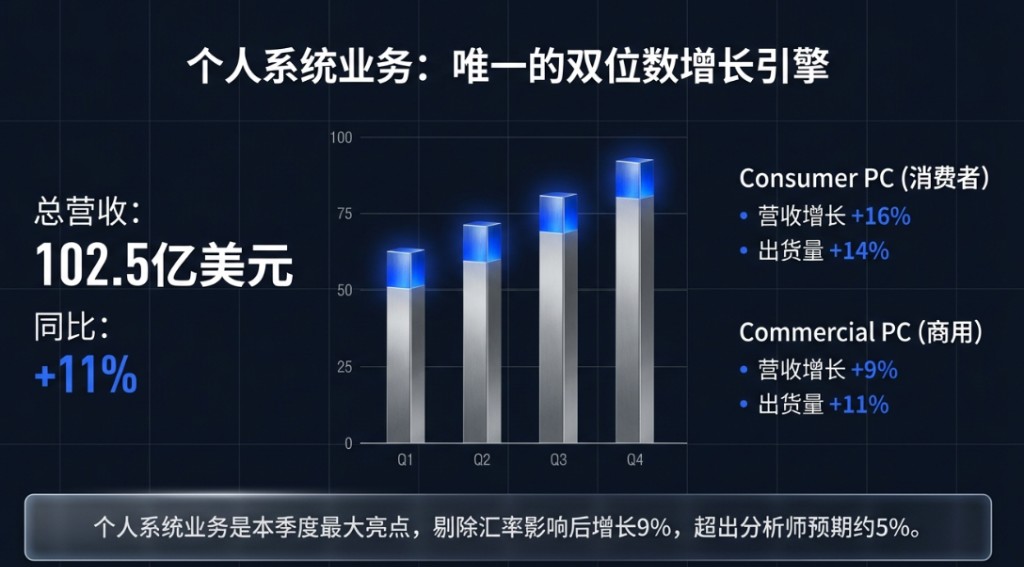

推动业绩超预期的核心引擎来自个人系统业务,PC 部门营收同比强劲增长 11% 至 102.5 亿美元,其中消费者 PC 更录得 16% 的高增速,AI PC 持续放量是重要驱动力。

然而,打印业务营收同比下滑 2.2% 至 41.9 亿美元,消费者打印更大幅萎缩 8%。更令投资者担忧的是前瞻指引。公司预计第二财季非 GAAP 每股收益区间为 0.70 至 0.76 美元,中值 0.73 美元低于市场预期的 0.75 美元。

CFO Karen Parkhill 直言,随着内存成本持续上行,公司虽维持全年指引,但预计实际结果"将偏向低水平区间"。临时 CEO Bruce Broussard 则以"正在应对行业层面的逆风"来定性当前处境。

财报公布后,惠普盘后股价快速下挫,跌幅逼近 7%。

前景展望:内存涨价是最大变量,指引中值低于预期

市场对本次财报最大的失望,集中在前瞻指引上。

第二财季非 GAAP 每股收益指引区间 0.70 至 0.76 美元,中值 0.73 美元低于市场预期的 0.75 美元;GAAP 每股收益指引区间 0.52 至 0.58 美元。

管理层明确将"内存成本上升"列为最重要的宏观逆风,CFO 表示公司虽然"擅长应对逆风",但在"动态环境"下,当前倾向于将全年结果定位在指引区间的低水平。

全年来看,公司维持 2026 财年非 GAAP 每股收益 2.90 至 3.20 美元的指引区间不变,中值 3.05 美元略高于市场预期的 3.00 美元,但"区间低水平倾向"的措辞实质上已构成一次温和的预期下调。全年 GAAP 每股收益指引为 2.47 至 2.77 美元。

分析师目前预计惠普未来 12 个月营收同比下滑 2.1%。在 AI PC 短期催化剂与内存成本中期压制之间,惠普的估值修复之路仍面临明显阻力。

个人系统:AI PC 拉动超预期增长,但结构性压力犹存

个人系统业务是本季度最大亮点,也是唯一实现两位数增长的核心板块。

季度营收 102.5 亿美元,同比增长 11%(剔除汇率影响后增长 9%),较分析师预期的 97.6 亿美元超出约 5%。

从细分来看,商用 PC 营收增长 9%,消费者 PC 增长 16%;出货量层面,总单位量同比增长 12%,消费者 PC 单位量增长 14%,商用 PC 增长 11%。

AI PC 的持续渗透是驱动本季度个人系统超预期的关键。惠普管理层在财报中多次强调"AI PC 的持续动能",将其定性为"未来工作战略"的核心执行抓手。

从行业背景来看,企业客户的 PC 换机周期正在加速,叠加 Windows 10 支持终止在即所带来的更新需求,短期内为商用 PC 市场提供了较为扎实的需求基础。

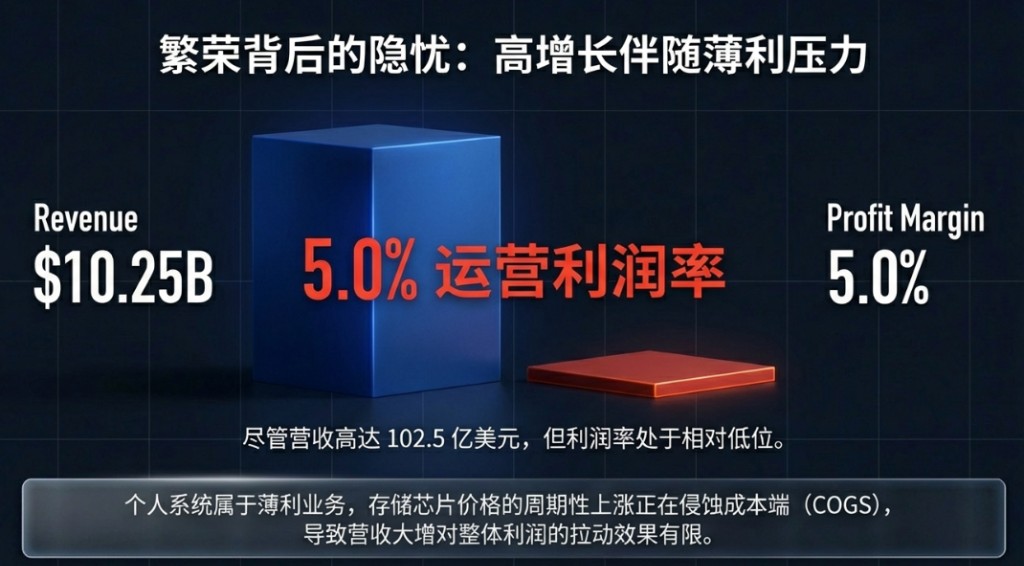

不过,从盈利质量看,个人系统业务的运营利润率仅为 5.0%,属于相对薄利的业务形态,大幅增长对整体利润的拉动效果有限。

此外,存储芯片价格的周期性上涨正在侵蚀该业务的成本端,这也是管理层将全年预期下调至低端的直接原因之一。

打印业务:高利润率难掩持续萎缩之困

打印业务贡献了本季度 18.3% 的高运营利润率,是整体盈利能力的重要稳定器,但营收层面的颓势已难以回避。

季度打印营收 41.9 亿美元,同比下滑 2%(固定汇率下降 3%),其中消费者打印跌幅达 8%,商用打印亦下滑 3%,核心耗材收入同比微降 1%,总硬件出货量下滑 6%。

从更长周期来看,惠普商业打印业务过去两年平均同比下滑 3.3%,显示出该业务面临的结构性收缩压力。

数字化办公的加速普及、企业打印需求的长期萎缩,使打印这一曾经的"印钞机"业务逐渐失去成长动能。尽管高利润率仍能为集团贡献可观的利润池,但其对营收增长的拖累效应正在逐步显现。

现金流与资本配置:自由现金流偏低,回购力度仍持续

本季度惠普经营活动产生现金 3.83 亿美元,自由现金流 1.75 亿美元,相较于逾 144 亿美元的营收,自由现金流转化率仅约 1.2%,与去年同期持平。

尽管现金造血能力有限,惠普仍保持了积极的资本回报节奏。

本季共回购 1330 万股、耗资 3.25 亿美元,同时支付每股 0.30 美元的现金股息,合计约 2.77 亿美元,季内向股东返还资本合计约 6 亿美元。季末持有现金及现金等价物 32 亿美元。

展望全年,公司预计全年自由现金流在 28 亿至 30 亿美元之间,但已明确表示将偏向区间低端。这一表态叠加存储成本上行预期,意味着下半年现金流压力值得持续跟踪。