2026: The Year of Reversal, A New Era of Lithium Ore Secondary Eruption

Lithium carbonate futures surged, marking a shift in the industry's pricing logic from "realistic easing" to "forward tightening." Dongfang Securities pointed out that against the backdrop of capital expenditure contraction leading to supply delays and the explosive demand for energy storage becoming the second engine, 2026 will see a turning point in supply and demand. The enhanced financial attributes amplify the slope of price fluctuations, indicating that the lithium price center will move up to the range of 120,000 to 200,000 yuan. Influenced by geopolitical factors and key mineral policies, the pricing of resource scarcity is being priced in advance

The rapid surge in lithium carbonate futures is pushing the lithium industry from a "realistic loose" trading framework towards a "forward tight" pricing logic. The contraction in capital expenditure on the supply side, combined with project delays and accelerated energy storage demand, has raised expectations for a higher price center for lithium, while the financial attributes dominated by futures have amplified the slope and volatility of this process.

On the 24th, the main contract for lithium carbonate on the Guangzhou Futures Exchange rose by 11%, closing at 164,900 yuan/ton, with concentrated pricing on the futures side becoming the most direct signal for the market.

From a price perspective, this level has entered the core area of the 120,000 to 200,000 yuan/ton operating range for lithium carbonate as projected by the team led by Jia Yi at Dongfang Securities in their research report dated February 22, reinforcing the market consensus that "2026 will be a turning point year."

Dongfang Securities emphasized in the report that the initiation sequence of the lithium market is typically "stocks → futures → spot," with expected turning points often leading fundamental turning points. The current jump in futures indicates that forward supply and demand, along with policy variables, are being priced in advance, which may further influence the pace of spot procurement and inventory decisions.

Futures Ignite First, Amplifying Lithium's Financial Attributes and Volatility

Dongfang Securities pointed out that since the launch of lithium carbonate futures in 2023, the financial attributes of the lithium industry have significantly strengthened. Price formation is no longer solely determined by spot supply and demand, but is more influenced by capital market expectations, risk preferences, and hedging behaviors.

This change has clear "infrastructure" support. The report shows that the delivery system for lithium carbonate futures has continued to expand, with a significant increase in the number of participants in hedging. The number of lithium battery listed companies disclosing hedging in lithium carbonate futures has risen from 23 in 2023 to 71 in the first half of 2025, and the holding rate of general corporate clients has increased from 18.50% to 49.63%. Within this framework, futures are more likely to become a concentrated outlet for changes in expectations and transmit through hedging and trade pricing to the spot market.

Supply: CAPEX Low Point Combined with Approval Delays, "Effective Increment" Limited

The core change on the supply side is the "secondary suppression" of capital expenditure due to price declines. Dongfang Securities believes that the decline in lithium prices over the past two years has significantly compressed global lithium resource capital expenditure, with core lithium companies' CAPEX having entered a cyclical low point. Their estimates show that the global lithium resource capacity growth rate will only be 17.1% from 2024 to 2025, and the effective capacity growth rate is expected to remain at 20%-25% from 2026 to 2027, with relatively limited increments available for release in the future, making the possibility of a sudden increase in supply pressure quite small.

At the same time, some existing and incremental projects both domestically and internationally are disturbed by policy and other factors, leading to prolonged approval and construction rhythms, resulting in a structural delay in the supply system. The report mentions that the new "Mineral Resources Law" will be implemented on July 1, 2025, and the tightening of mineral rights review in places like Jiangxi and Qinghai has increased the uncertainty of domestic supply realization.

At the same time, some existing and incremental projects both domestically and internationally are disturbed by policy and other factors, leading to prolonged approval and construction rhythms, resulting in a structural delay in the supply system. The report mentions that the new "Mineral Resources Law" will be implemented on July 1, 2025, and the tightening of mineral rights review in places like Jiangxi and Qinghai has increased the uncertainty of domestic supply realization.

In terms of incremental calculations, Dongfang Securities expects a net increase of about 448,000 tons of LCE in supply by 2026, but the new supply will mainly come from the ramp-up of newly commissioned projects, with mining permits and ramp-up progress being key variables. It also notes that there is a time lag in supply elasticity, with about 35% of the supply expected to be released within approximately three months in 2026, while the rest relies more on the ramp-up of new projects, which has limited short-term relief on supply and demand.

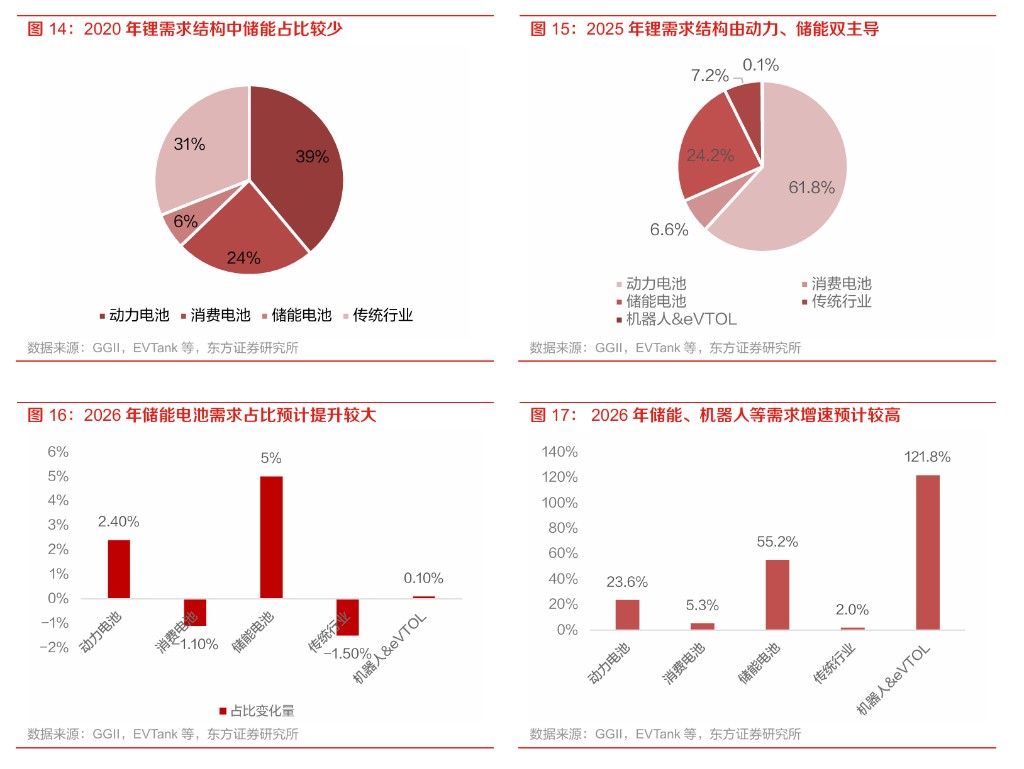

Demand: Energy Storage Becomes the Second Engine, Structural Upward Revision Dominates Expectations

The key variable on the demand side is energy storage. Dongfang Securities estimates that the global lithium industry's direct demand scale will be about 1.94 million tons of LCE by 2026, with energy storage demand entering an accelerated expansion phase, and the annual demand is expected to reach about 570,000 tons of LCE, with a year-on-year growth rate of about 55%, increasing its share to nearly 30%, and is expected to exceed 30% after 2026, becoming the core demand area second only to power batteries.

The driving force comes from the expansion of wind and solar installations, grid upgrades, and the increased reliance on electrochemical energy storage for AI-related infrastructure construction. The report also predicts that the global newly installed capacity for energy storage will reach about 900 GWh by 2026. In terms of power batteries, the lithium demand for power batteries is expected to reach 1.15 million tons of LCE in 2026, a year-on-year increase of 24%, with global sales of new energy vehicles expected to reach 25.58 million units.

Price: Switching from "Current Looseness" to "Future Tightness," Central Level Moves Up but Elasticity Increases

Dongfang Securities judges that the lithium industry has completed a phase of bottoming out by 2025 and has entered an upward turning point. Its essence is not merely a simple supply-demand rebalancing, but a shift in pricing logic from current transaction looseness to future transaction scarcity.

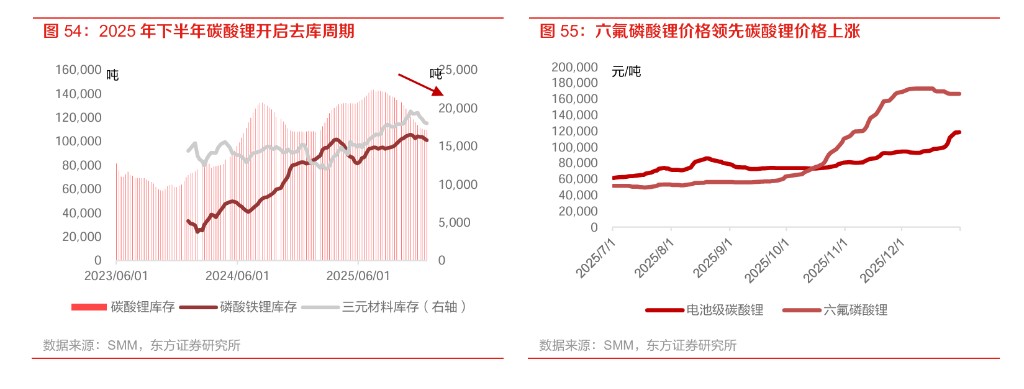

On the inventory front, the report shows that the inventory destocking inflection point will gradually appear in the second half of 2025, with lithium carbonate inventory decreasing from about 138,000 tons in mid-September to about 110,000 tons in late December, while the price of lithium hexafluorophosphate serves as a leading signal for the rise in lithium carbonate prices.

In terms of price outlook, Dongfang Securities expects the price range for lithium carbonate in 2026 to be between 120,000 and 200,000 yuan/ton, and notes that under the backdrop of tight supply and demand and phase-specific restocking, there is a possibility of rising to a higher range, but "the absolute height may be difficult to replicate" historical extreme market conditions. Its scenario analysis shows that a rise in lithium prices will trigger supply elasticity: in the scenario of 70,000-90,000 yuan/ton, the supply in 2026 will be 2.041 million tons of LCE, and the real demand (considering restocking) will be 2.091 million tons of LCE, indicating a shortage; when the price rises to 90,000-120,000 yuan/ton, the supply increases to 2.170 million tons of LCE, with supply and demand tending to balance and slightly easing Under the scenario of 120,000-150,000 yuan/ton, supply can reach 2.349 million tons of LCE, and the surplus expands.

According to a previous article by Jianwen, UBS has significantly raised its 2026 spodumene price forecast by 74% to $3,131/ton, and lithium carbonate to $26,000/ton. This move is based on electric vehicles achieving "triple price parity" and a surge in energy storage demand, with global demand expected to double to 3.4 million tons by 2030. UBS believes that the market has entered the third super cycle of lithium prices, and the ongoing supply-demand gap will support prices significantly above market consensus.

Geopolitics and Policy: The "Critical Mineral" Attribute Provides Additional "Options"

Dongfang Securities suggests that beyond the benchmark supply and demand, "options should be added," as lithium has been listed alongside nickel and cobalt in the critical mineral lists of China, the U.S., and Europe. Policy adjustments in resource countries, strategic reserve actions, and proactive inventory replenishment in the supply chain may amplify market pricing for scarcity.

The report lists several policies and geopolitical variables, including Chile's push for mineral nationalization, which may lead to a decrease in Tianqi Lithium's equity resource in SQM (estimated at about 37%), Mexico designating lithium as a strategic mineral and prohibiting the granting of concessions to private entities, and Canada strengthening investment reviews for critical minerals. In North America, Lithium Americas (LAC) stated that the U.S. Department of Energy (DOE) has acquired a 5% stake in the company and obtained a 5% interest in the Thacker Pass project, highlighting the proactive layout for critical mineral supply security