Wall Street in-depth interpretation "Trump's IEEPA tariffs rejected": tariffs may be reduced in the second half of the year, tax rebates may become comprehensive stimulus, potential industry benefits

华尔街分析认为,尽管政府迅速启动替代关税,但有效税率小幅下降,且 7 月后政策趋向温和。裁决的核心变量在于高达 1800 亿美元的潜在退税,其中约 1200 亿美元或转化为中期选举前的中产阶级刺激款项。由于通胀传导已基本完成,该裁决对经济增长和物价的直接冲击有限,但可能通过财政扩张支撑经济,并因关税工具受限而导致美元中期走势偏弱。

美国最高法院推翻特朗普基于紧急经济权力法实施的关税后,华尔街主要投行认为这一裁决对经济和市场的实际冲击有限,但为下半年关税政策转向温和创造了空间,同时可能催生规模高达 1200 亿美元的选民退税计划。高盛和摩根士丹利的分析显示,有效关税率仅小幅下降约 1 个百分点,通胀传导已基本完成,而 7 月后关税到期将迫使政府采取更多豁免措施。

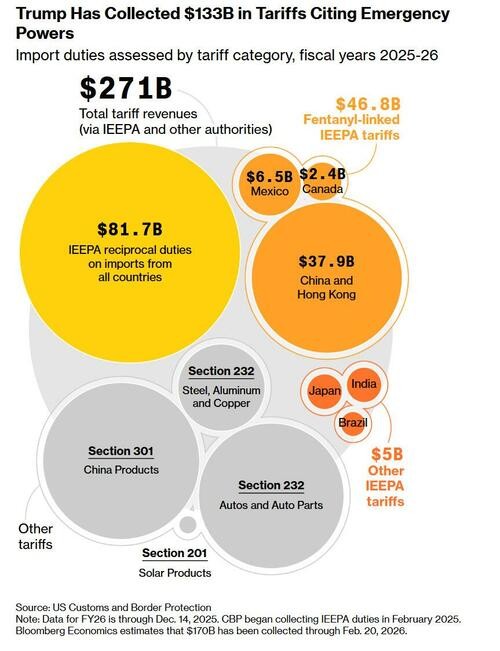

据央视新闻,美国最高法院 20 日裁决美国政府征收大规模关税政策 “越权”。最高法院以 6-3 的投票结果裁定特朗普政府根据《国际紧急经济权力法》(IEEPA) 实施的关税违宪。据央视报道,21 日,特朗普又宣布,把这项新征收的 “全球进口关税” 税率由 10% 提升至 15%。这些关税将持续至 7 月 24 日,之后可能通过第 301 条款实施更持久的关税措施。

据高盛测算,政策调整后,自 2025 年初以来的有效关税率增幅将从略高于 10 个百分点降至约 9 个百分点,基本符合市场此前预期。摩根士丹利指出,假设现有关税结构将转移至不同法律授权并基本维持原状,且退税规模有限 (以 850 亿美元为中点估计),企业支出或招聘意愿不会出现重大变化。

退税问题仍存在重大不确定性。最高法院未就政府是否必须退还关税以及具体时间框架作出规定。高盛估计 IEEPA 关税已征收约 1800 亿美元,其中大部分将在未来一年左右分批退还。由于美国消费者承担了约 90% 的关税负担,这实际上为特朗普在中期选举前向中产阶级直接发放最多 1200 亿美元刺激款项提供了机会。

关税率实际降幅有限,通胀压力已过高峰

尽管最高法院推翻了 IEEPA 关税,但华尔街认为对通胀和经济增长的影响将极为有限。高盛的分析显示,关税成本向消费者价格的传导已基本完成。

高盛估计,截至 1 月,关税传导使核心个人消费支出价格指数 (PCE) 上涨约 0.7%,2026 年剩余时间仅将额外推高价格 0.1%。对于实施时间已达 10 个月的商品,关税传导率已超过 60%,而首五个月之后的增量传导幅度不大,表明大部分价格传导在最高法院裁决前已经完成。高盛假设传导率将在 70% 见顶。

高盛首席政治经济学家 Alec Phillips 指出,尽管有效关税率小幅下降,但该行预计 2026 年剩余时间不会出现净通缩效应,因为企业降价以应对关税减免的速度远远慢于它们此前因关税上涨而提价的速度。不过,未来大多数面临关税减免商品的价格涨幅将小于往常水平。

在经济活动方面,最新变化将最直接影响美国进口。部分国家的关税率将大幅下降,这些国家在一季度和二季度的对美出口可能从低迷水平有所反弹。但高盛认为对 GDP 的影响应该会被库存积累增加、从其他转口贸易国家的进口减少以及关税上涨国家的进口小幅下降所抵消。

高盛将 2026 年一季度 GDP 追踪预估设定为 3.4%,但其中包括 2025 年四季度政府停摆结束带来的 1.3 个百分点贡献,这意味着剔除该特殊因素后的潜在增长率为更温和的 2.1%。该行维持 2026 年四季度同比增长 2.5% 的预测,较 2025 年四季度同比 2.2% 的增速加快 0.3 个百分点,部分反映了关税拖累消退而减税提振的政策脉冲正向变化。

7 月后关税或趋于宽松,豁免范围料扩大

第 122 条款的法定限制为华尔街提供了关税政策可能转向温和的关键线索。该条款将关税上限设定为 15%,并限制实施期限为 150 天,"除非国会通过法案延长该期限"。特朗普 2 月 20 日签署的行政令明确当前税率将于 7 月 24 日到期。

摩根士丹利认为,尽管特朗普迅速宣布将第 122 条款关税提高至 15%,但预计总统将在台面下推行更温和的关税政策。这意味着更多例外、豁免、延期等措施,与政府过去几个月采取的近期举措一致。这可能为最终不在新的第 232 条款或第 301 条款调查范围内的国家和产品提供利好。

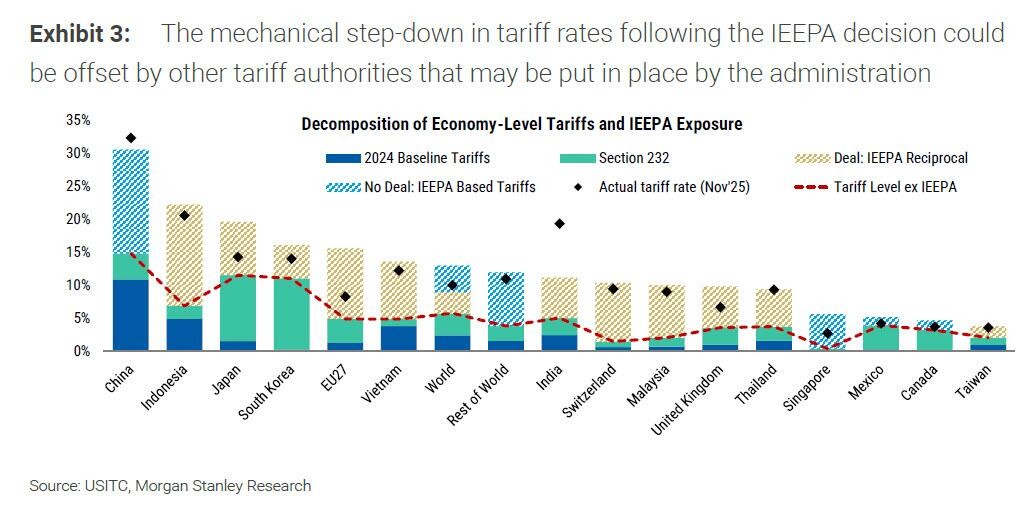

高盛详细分析了不同贸易伙伴面临的关税变化。一些规模较大的经济体,特别是欧盟、日本、瑞士,此前与特朗普政府达成协议,实施包括现有美国关税在内的最高 15% 税率 (现有税率通常在 0-2.5% 之间)。这些贸易伙伴现在可能面临增量关税增加,因为 15% 的税率现在将"叠加"在现有美国关税之上。

但另一方面,高盛预计占 2025 年美国进口总额略高于一半的几个其他贸易伙伴已与美国达成协议,不太可能被优先纳入第 301 条款调查。这包括阿根廷、澳大利亚、孟加拉国、柬埔寨、厄瓜多尔、萨尔瓦多、欧盟、危地马拉、印度、印度尼西亚、日本、韩国、马来西亚、瑞士、泰国、英国和越南。

高盛预计约占美国进口 10% 的国家面临近期第 301 条款调查的最大风险,包括巴西和南非。总体而言,高盛预期类似刚宣布的 15% 税率将持续到年底,豁免范围与 IEEPA 关税相同,但到 2027 年初,政府将利用第 301 条款和其他授权将关税率恢复到接近最高法院裁决前的水平。

摩根士丹利指出,风险在不同时间点指向不同方向。7 月之后风险倾向于更低关税,因为政府可能难以利用其他授权完全替代即将到期的第 122 条款关税。但在中期选举后以及到 2027 年初,风险则倾向于更高关税。

退税程序存疑,或成中期选举刺激工具

退税问题可能演变成 2026 年最大的财政政策变数。最高法院未就特朗普政府是否必须退还关税或在任何特定时间框架内退还作出规定。大法官 Kavanaugh 在异议意见中重申,退税程序"可能会是一团糟"。

尽管如此,关税征收可能立即停止。鉴于最高法院广泛推翻了 IEEPA 关税授权,继续征收将缺乏法律依据。这可能导致长期不确定性,因为退税问题将留给下级法院审议。

高盛估计,IEEPA 关税迄今已征收约 1800 亿美元,其中大部分将在未来一年左右分批退还。过去,退税最初仅限于通过海关与边境保护局 (CBP) 或财政部建立的程序主动提出投诉或诉讼的公司,这最终可能限制退税范围。

但分析指出,由于各种政治化媒体计算出美国消费者承担了 90% 的关税影响,这实际上使特朗普能够在中期选举前向美国中产阶级发放刺激款项,在某个时点直接存入多达 1200 亿美元 (约 1330 亿美元 IEEPA 关税退税的 90%)。这可以称为"2026 年特朗普关税退税刺激计划"。

摩根士丹利认为,如果进口商将收到退税但又必须以额外未来进口关税的形式偿还该退税,那么这接近于现状结果。但如果政府选择让有效关税率在完成新的第 232 条款和第 301 条款调查期间下降 (最有可能发生在今年晚些时候或 2027 年),这将导致通胀暂时面临下行压力,并将企业支付新进口关税的时间推迟到 2027 年,从而对经济活动增长持更建设性的看法。

市场影响:美债承压短期,美元中期走弱

华尔街对裁决的市场影响看法出现分化,短期和中期逻辑存在显著差异。

在美国国债市场,摩根士丹利认为,鉴于政府将利用其他现有授权重新实施关税,投资者对财政赤字近期路径的预期不太可能改变。在退税方面,最高法院的裁决"今天对政府是否以及如何退还已从进口商那里征收的数十亿美元未作任何表示"(引自 Kavanaugh 大法官的异议意见)。

在投资者理解最高法院裁决的具体轮廓之前,他们可能认为风险偏向更高而非更低的国债收益率。正如预期,第一轮市场反应是投资者抛售国债,因为他们认为这将迫使财政部更快增加债券发行规模。

但摩根士丹利预计这种反应不会持续很久,因为大多数投资者最终会明白,这项裁决带来的潜在发行增量将由短期国库券构成。另一个重要考虑因素是,尽管财政部可能面临额外义务,但无需等到退税时间才开始建立财政部一般账户 (TGA) 余额。因此,摩根士丹利认为第二轮且更持久的反应是投资者"逢事实买入"并推动收益率走低,因为他们的关注点将回到通胀的下行风险。

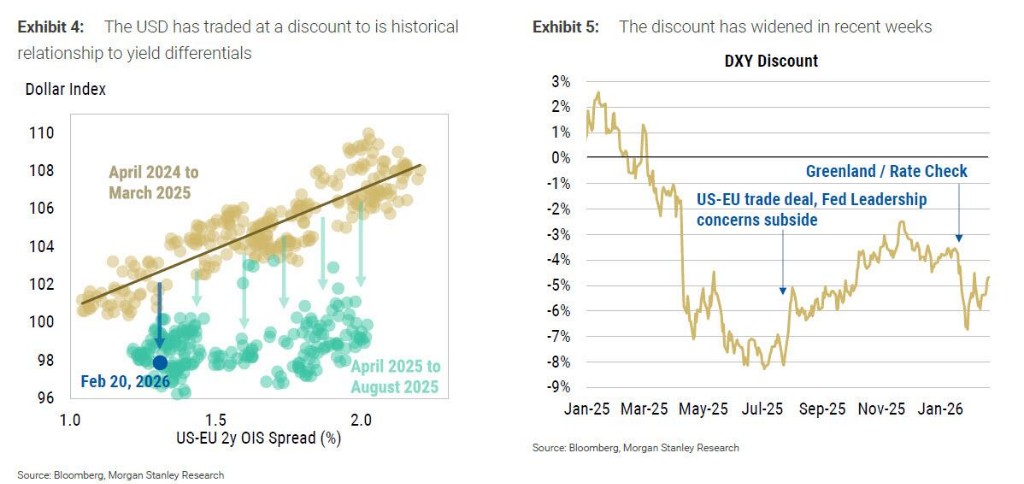

在美元市场,摩根士丹利预计美国政府使用即时关税授权作为外交政策工具的余地减少,可能在边际上降低与投资者对持有美元敞口保持谨慎相关的美元负面风险溢价。

但抵消因素可能维持 (甚至扩大) 这种美元负面风险溢价,包括地缘政治不确定性和围绕美国货币政策的疑问。此外,对全球增长的机械性正面影响 (因为使用不同授权的关税需要时间实施,且可能以较低水平实施) 可能提振全球增长预期,进一步拖累美元。因此摩根士丹利继续预期美元下跌。

高盛则强调,一些国家关税率将大幅下降,这些国家的对美进口在一、二季度可能从低迷水平反弹,尽管对 GDP 的影响应该会被其他因素抵消。这种贸易流向的变化也将对不同国家货币产生差异化影响。

整体而言,华尔街认为最高法院裁决虽然在法律层面具有重大意义,但在经济和市场影响方面相对温和。真正的不确定性在于 7 月之后的关税路径选择,以及退税如何转化为实际的财政刺激,这两个因素都可能在下半年为市场带来超预期的正面影响。