The Japanese stock market frenzy cannot hide the turmoil in bonds and currencies. Is "high market trading" an opportunity or a trap?

日本股市在 “高市交易” 推动下创历史新高(日经 225 本周涨 5%),但债市与汇市平静背后暗藏 “高市陷阱”:若高市早苗大幅支出以兑现承诺,可能削弱日元、加剧通胀,最终反噬股市。尽管她承诺减税不涉及新债,但分析师质疑兑现能力。

随着高市早苗在上周日的选举中取得胜利,日本股市本周接连创下历史新高,日经 225 指数累计上涨 5%。然而,在这场被市场称为 “高市交易” 的狂欢背后,部分投资者开始担忧这是否正在演变成一个陷阱,甚至有交易员警告目前的市场平静可能只是 “暴风雨的前奏”。

尽管股市欢腾,但日本债券和外汇市场却表现出与选举前截然不同的相对平静。此前,市场曾因担忧高市早苗激进的财政支出计划而大幅波动。目前这种股债市场的脱节表明,部分投资者似乎相信新任首相虽然获得了更大的权力,但在落实其财政计划时将会表现出克制。

然而,核心风险依然存在。分析人士警告称,日本市场面临着潜在的 “高市陷阱”:如果新首相为了兑现解决生活成本问题的承诺而大幅增加公共支出,可能会进一步削弱日元,进而通过推高能源等进口成本加剧通胀,最终反噬股市表现。

目前,高市早苗正试图安抚市场,声称其在竞选期间关于日元的言论被 “误解”,并承诺削减消费税的计划不会涉及发行新债。但华尔街策略师对此持怀疑态度,质疑其在拥有如此巨大民意授权的情况下,如何在不扰乱市场的前提下兑现财政承诺。

暴风雨前的宁静

据媒体报道,尽管日经 225 指数本周上涨了 5%,但一位东京交易员指出,日本国债和日元市场的反应比选前预期的要平静得多。该交易员警告称:“我们可能应该将其视为一种暂时现象,因为问题的核心在于她如何为此买单。这不是蜜月期,更像是暴风雨前的宁静。”

自去年 11 月高市早苗公布一项价值 1350 亿美元的财政支出计划以来,她与债券和货币市场的关系一直处于紧张状态。为了在选举中利用其人气,她此前承诺暂停征收食品消费税两年,预计这项措施将耗资 5 万亿日元(约合 320 亿美元)。在这一预期下,日本 40 年期国债收益率一度突破 4%,日元也随之走弱。

如今,她在下议院获得的绝对多数席位,为她落实这些支出承诺提供了坚实的政治基础,但这恰恰是市场焦虑的根源。

汇率陷阱与央行困境

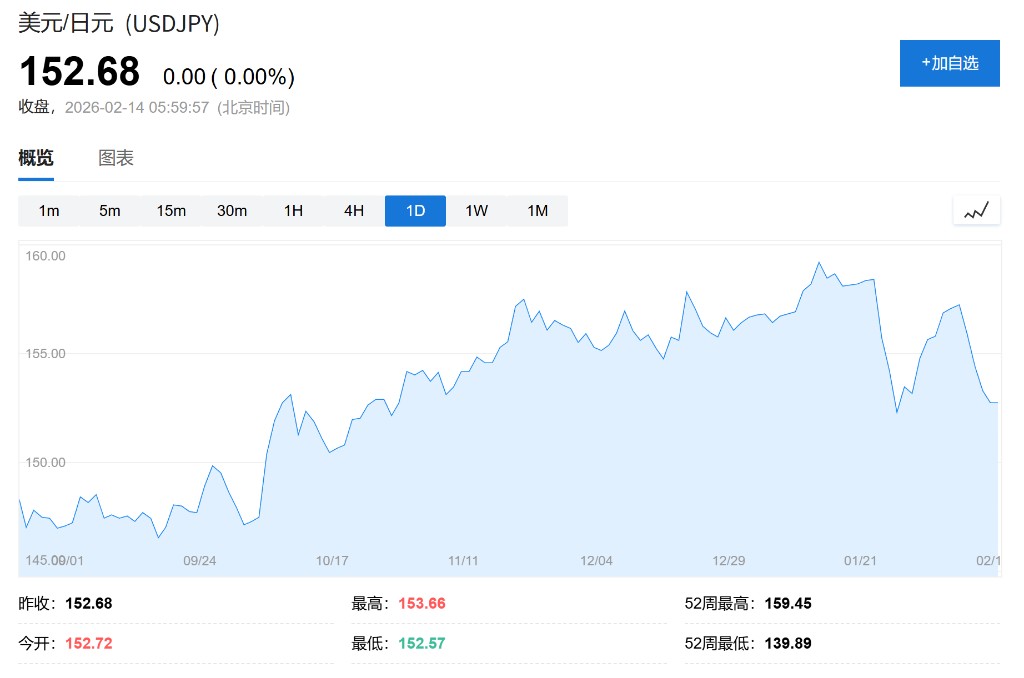

BMI 亚太区国家风险主管 Darren Tay 指出,日元目前正面临 “高市陷阱” 的风险。政府支出越高,货币贬值的风险就越大。目前日元兑美元汇率在 153 附近徘徊,高市早苗一直依靠其财政大臣片山皋月来安抚市场,官员们也发出口头警告,暗示可能进行干预。

花旗外汇策略师 Osamu Takashima 表示,如果日元汇率反弹至 160,政府将干预市场。这就使得日本央行陷入了两难境地。尽管市场预期日本央行将在 2026 年至少加息两次,但一些交易员担心,央行可能面临推迟加息的压力,以便为高市早苗提供更多的财政行动空间。

如果央行维持宽松而财务省进行干预,一位交易员直言,这种情况下任何干预都将等同于 “对卖空者的临时补贴”。

财政承诺的可行性存疑

为了缓解与金融市场的紧张关系,高市早苗在选后的首次新闻发布会上表示,她的消费税削减计划不会涉及发行新债。然而,分析师对此表示怀疑。

摩根大通高级经济学家 Benjamin Shatil 指出:“鉴于她获得的授权规模,她怎么可能现实地撤回这样的承诺?与其他首相不同,她不能以议会阻力为借口。”

此外,美银日本外汇及利率策略主管 Shusuke Yamada 认为,选举并未改变日元疲软的结构性驱动因素。他指出,企业和投资者将继续在老龄化、增长缓慢的日本之外寻找回报,日元套利交易不太可能在短期内逆转。他强调:“他们需要看到确凿的证据表明日本是一个更好的长期投资地……这需要数年时间。”

债务隐忧与市场分歧

市场对日本财政状况的担忧根源在于其庞大的公共债务。据国际货币基金组织(IMF)数据,日本公共债务总额占 GDP 的 237%。

对于这一风险,市场存在显著分歧。CLSA 分析师 Nicholas Smith 认为,这种担忧主要反映了外国投资者的观点,他们仅持有 6.6% 的日本国债,却占据了 71% 的期货交易量。Smith 表示,外国投资者 “没有切身利益,种种迹象表明他们并不真正了解这个市场”,并指出日本的净债务状况明显低于总债务,且预计未来几年将继续下降。

然而,其他人则认为政府应更加警惕。BMI 的 Darren Tay 警告称,市场可能低估了高市早苗释放的民粹主义压力,认为日本债务主要由国内持有的观点可能给政府带来一种 “危险的绝缘感”,使其忽视全球债券市场的警戒信号。

野村研究所经济学家 Takahide Kiuchi 也表示,虽然债务水平本身未必是问题,但他 “从未经历过像选前那样长期收益率急剧上升的情况”。他警告称,日本政府应对这些警告信号做出反应,否则日本可能面临危机。