How does Wall Street view the January CPI? Inflation concerns take a breather, and the probability of three rate cuts this year rises to fifty percent

Due to companies often raising prices at the beginning of the year, the CPI tends to rise in January, but this January, the core CPI growth rate hit a nearly five-year low. Although housing prices continue to rise and consumer goods such as clothing and computers show signs of tariff impacts, prices in politically sensitive categories like gasoline, beef, and eggs have fallen, with disinflationary pressures expected to dominate in the coming months. Goldman Sachs believes that the Federal Reserve's path to "normalizing" interest rate cuts depends on whether employment continues to improve, and still expects two rate cuts this year, the first in June. Traders expect the CPI to peak around mid-year and then decline, consistent with expectations for the first rate cut in June or July

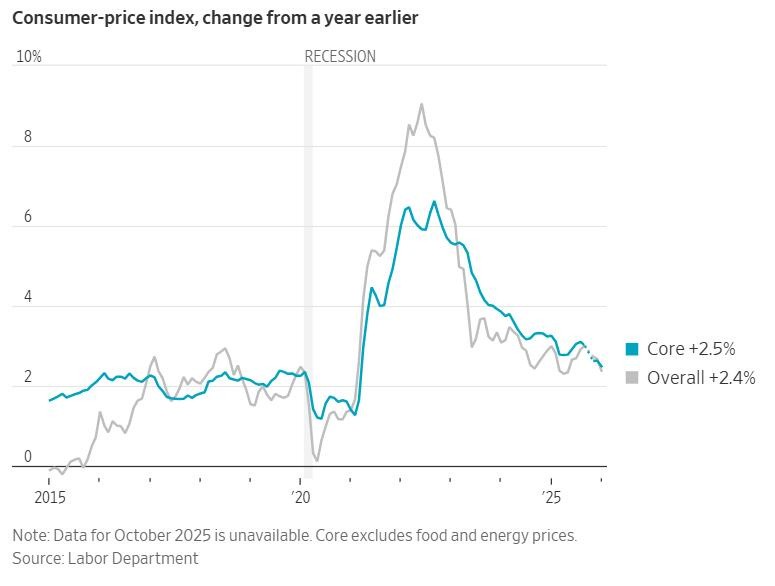

In the usual early-year period of rising inflation, the inflation data in the United States showed moderate growth, with the year-on-year growth rate of core CPI falling to nearly the lowest level in five years, indicating that price pressures continue to ease. This unexpectedly cooling inflation performance boosted market expectations for the Federal Reserve to cut interest rates this year, with bond market traders raising the probability of three rate cuts within the year to fifty percent. Although some service prices remain sticky, the overall data opens up space for the Federal Reserve's subsequent policy adjustments.

The U.S. Bureau of Labor Statistics (BLS) announced on Friday, the 13th, that the January CPI increased by 2.4% year-on-year, the lowest growth rate since May of last year, down from the December growth rate of 2.7% and below the market expectation of 2.5%; the January core CPI increased by 2.5% year-on-year, the lowest growth rate since March 2021. Nick Timiraos, a journalist known as the "new Federal Reserve correspondent," pointed out that the month-on-month increase in the January core CPI was slightly lower than some expectations, with the year-on-year growth rate continuing to slow.

After the CPI data was released, U.S. stock futures rose, U.S. Treasury prices turned up, yields erased gains and turned lower, and the dollar fell. The two-year U.S. Treasury yield, sensitive to interest rates, briefly dropped by 6 basis points to 3.40%, marking the lowest level in nearly two months since October 2025.

Following the CPI release, traders' expectations for the total rate cut this year rose from 58 basis points on Thursday to 63 basis points, equivalent to a 50% chance of three rate cuts before the end of the year. The market expects a 30% probability of a rate cut in April and over 80% in June.

Two days before this mild CPI inflation report was released, stronger-than-expected January non-farm payroll data had just come out, which is expected to support the Federal Reserve in maintaining its current wait-and-see stance. Media pointed out that the January CPI often rises due to price increases by companies at the beginning of the year, but this January was far below the levels of previous years, indicating that disinflationary forces are dominating.

Price Increases Slow Across the Board

The January CPI increased by only 0.2% month-on-month, the smallest increase since July of last year, and below the expected 0.3%. Energy prices were the main drag, with the overall energy index falling by 1.5% and gasoline prices dropping by 3.2%. The core CPI increased by 0.3% month-on-month, in line with expectations but higher than December's 0.2%.

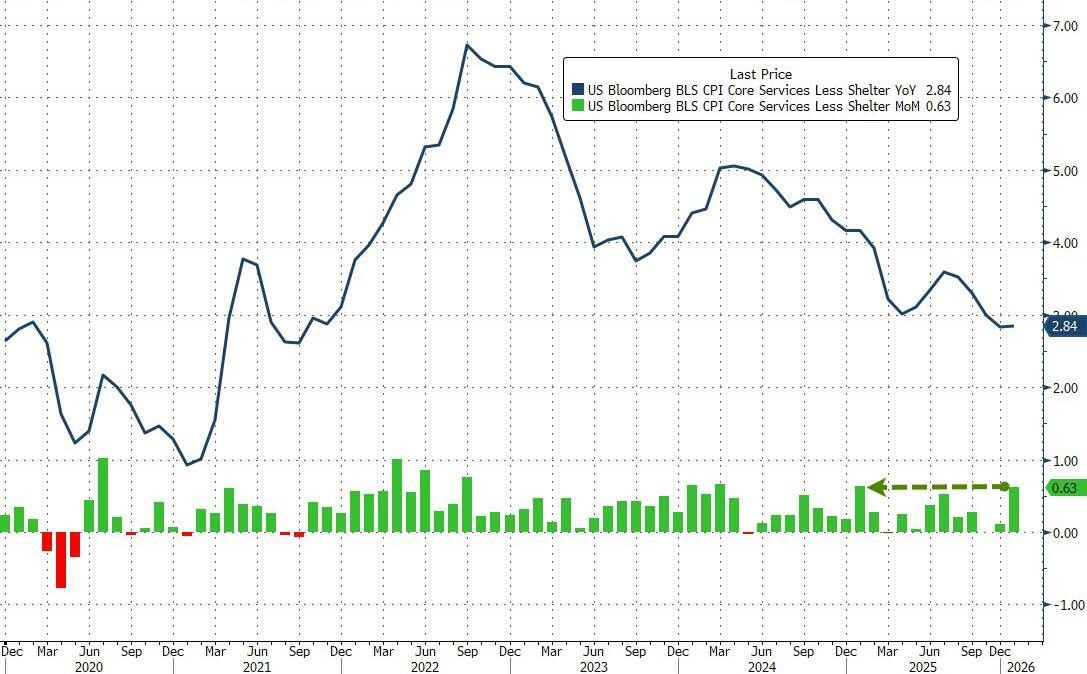

Excluding housing, the core service prices—super core CPI—grew by 0.56% month-on-month in January, the largest increase since January of last year, but the year-on-year growth rate slowed to 2.67%, the lowest growth rate since March 2021. This phenomenon may be related to "residual seasonal" factors, as the month-on-month increases in January 2024 and 2025 are expected to be the highest of the year.

Sub-item data shows that housing costs increased by only 0.2% month-on-month in January, the smallest increase since September of last year, with the year-on-year growth rate slowing to 3%. Prices for used cars and trucks fell by 1.8%, marking the largest decline in two years The increase in food prices is the smallest since July 2025, with beef and veal prices dropping by 0.4% and egg prices plummeting by 7%.

Some categories of goods show signs of tariff impacts. Clothing prices rose by 0.3%, video and audio products increased by 2.2%, computers and smart home assistants went up by 3.1%, and laundry equipment rose by 2.6%. Airfare prices surged by 6.5%, marking the largest increase since mid-2022.

Inflation Trend Consolidation

The Wall Street Journal believes that the January inflation cooling has alleviated market concerns that the high tariffs of the Trump administration would lead to broader and sustained inflation. Its report points out that the lower overall price increase is a positive signal for the economy, although rising prices for goods such as clothing, televisions, and airfare still indicate that inflation continues to pressure consumers.

The report cites analysis indicating that the latest annual data benefits from the base effect of high inflation data exiting the statistical range in January 2025. In the final months of Jerome Powell's tenure as Federal Reserve Chair, the Fed faces a delicate task of carefully balancing between curbing inflation and protecting the labor market.

Bloomberg reports emphasize that a key indicator—the super core CPI's year-on-year growth rate is the slowest since March 2021. The report notes that prices for politically sensitive categories such as gasoline, beef, and eggs have fallen, but housing prices continue to rise, and airfare prices have surged. Consumer goods like clothing, computers, and smart home assistants show signs of tariff impacts.

Economists Anna Wong and Troy Durie from Bloomberg Economics state, "CPI often rises in January as businesses frequently raise prices at the beginning of the year. However, the core CPI in January this year is significantly lower than in previous years. While there are still some hot spots, there are strong disinflationary forces in automobiles, food, and energy. Overall, we believe disinflationary pressures will dominate in the coming months."

Wall Street Reassesses Rate Cut Path

Lindsay Rosner, head of fixed income investments across multiple departments at Goldman Sachs Asset Management, stated, "The path for the Fed to 'normalize' rate cuts now looks clearer, and concerns about rising January data are a thing of the past. However, the length of this path will depend on whether employment continues to show signs of improvement. We continue to expect two rate cuts this year, with the next action in June."

PIMCO economist Tiffany Wilding noted that the inflation report is "quite encouraging beneath the surface." She pointed out two positive developments: the housing inflation that has remained stable since the pandemic is genuinely slowing down; and the impacts related to tariffs are essentially fading. "As this impact fades, the Fed should feel more comfortable cutting rates. It seems reasonable for us to expect a few more rate cuts this year."

Christopher Hodge from Natixis described the data as "a peculiar mix," but indicated it ultimately points in one direction: "In the coming months, we expect inflation to remain above ideal levels but not accelerate, which will allow the Fed to cut rates in response to weak labor data."

Seema Shah, Chief Global Strategist at Principal Asset Management, stated, "Inflation is in line with expectations, but the market breathed a sigh of relief because, despite very strong labor market data earlier this week and the risk of further tariff transmission, price pressures remain contained But for the Federal Reserve, this is still not enough to justify a recent rate cut. The continued strength in the labor market provides cover for policymakers to maintain the status quo."

Eric Winograd, Senior U.S. Economist at AllianceBernstein, stated: "The real point is that the inflation trend remains unchanged before the government shutdown. Inflation is still sticky. The Fed feels comfortable maintaining rates. It is reasonable to expect that they will resume rate cuts later this year once there is clearer evidence that inflation is cooling."

Bond Market Bets on Accelerated Rate Cuts

Ira Jersey, Chief U.S. Interest Rate Strategist at Bloomberg Intelligence (BI), commented: "The strong immediate bullish steepening in the bond market reflects the comfort of CPI not rising. At the 2.4% level, considering the gap between CPI and the PCE deflator, it suggests that the Fed's 2% target is getting closer. The market may not price in an earlier rate cut, but pricing in a slightly lower terminal rate seems reasonable."

Jersey further pointed out: "The main reason for the movement in short-term Treasury yields is the repricing of the Fed's rate cut endpoint, rather than the timing of additional cuts. Over the past two days, the terminal rate has fallen by more than 10 basis points, indicating a high likelihood of another rate cut before March 2027. If the next set of data is similar to recent data, we believe the market will start pricing in a federal funds rate below 3%."

Ali Jaffery from CIBC Capital Markets noted that the year-on-year CPI growth data of 2.4% and 2.5% is "essentially consistent" with the Fed's preferred inflation measure—the PCE price index running at the policymakers' expected 2% rate. Historically, CPI has averaged about half a percentage point higher than PCE.

The inflation swap market shows that traders expect CPI to peak mid-year and then decline, which aligns with market expectations that the Fed will begin rate cuts around June or July. The initial reaction in Treasuries has weakened as the focus shifts to the broader impact of this week's data releases. As of 9 AM Eastern Time, yields across maturities fell by 1 to 2 basis points.

Aroop Chatterjee, Managing Director at Wells Fargo Securities, stated: "The lack of substantial surprises may keep the Fed focused on the labor market. The market may be overestimating the likelihood of Fed rate cuts this year."