Is weak U.S. imports and a data vacuum from China's Spring Festival a short-term headwind for copper prices?

Morgan Stanley believes that copper prices are supported by expectations of interest rate cuts and an extreme supply shortage (with a projected deficit of 600,000 tons in 2026), placing them on a long-term bullish track. However, in the short term, U.S. import momentum has weakened due to adjustments in tariff expectations, coupled with a demand vacuum period before the Chinese New Year and seasonal inventory accumulation, leading to micro-adjustment pressures in the market. Although supply constraints are helping to establish a price floor, short-term volatility risks still exist

Copper prices, supported by macroeconomic benefits, are facing challenges at the micro level. Despite expectations of interest rate cuts, tight supply, and ongoing themes of emerging demand providing support, weakening import momentum in the U.S. and a demand vacuum before the Chinese New Year are putting short-term pressure on the market.

According to news from the Chase Wind Trading Desk, Morgan Stanley's Amy Gower team released a research report on the 22nd, stating that the narrowing COMEX-LME price spread is changing the flow of copper. After the import arbitrage window opened wide in the fourth quarter of 2025, U.S. refined copper imports surged in December last year and early January this year. However, as market expectations for copper tariffs under Section 232 in 2027 cooled, the narrowing price spread eliminated the economic incentive for further imports. This week, LME warehouses in the U.S. even saw the first copper inflow in nearly a year, following a brief premium in LME spot prices.

Morgan Stanley noted that in December last year, China's apparent copper demand remained flat, with strong refined copper exports and a seasonal accumulation of inventory. As the Lunar New Year approaches in mid-February, the market will enter a data vacuum period, with further information on demand conditions not expected until mid-March.

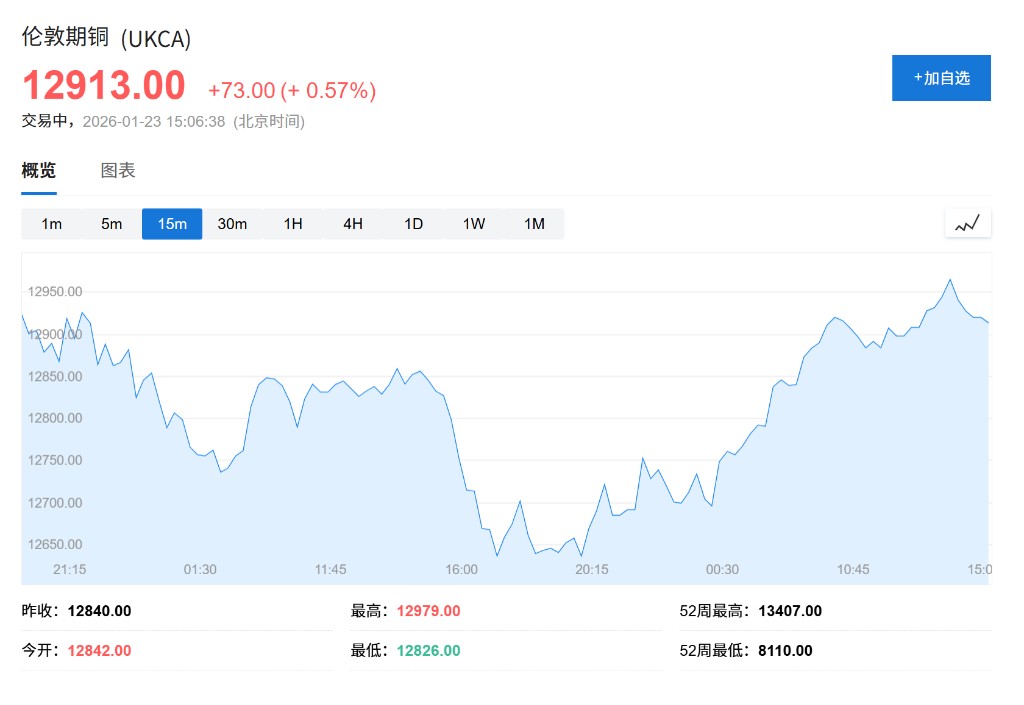

However, the extreme constraints on the supply side will provide bottom support for copper prices. Morgan Stanley expects copper mine supply growth to be only 0.2% in 2026, leading to a market deficit of about 600,000 tons. The Mantoverde mine under Capstone in Chile is shut down due to strikes (with an annual capacity of 106,000 tons), and several supply disruptions in 2025 will continue to affect this year. Analysts believe that under tight supply and a strong macro backdrop, prices will receive good support, but short-term fluctuations are unavoidable. As of the time of writing, London copper prices rose 0.57% to $12,913.

U.S. Import Momentum Shifts

The U.S. copper import boom is cooling down. Morgan Stanley data shows that although U.S. refined copper arrivals surged in December last year and early January this year, the narrowing COMEX-LME price spread has eliminated the financial incentive for continued large-scale imports. This change stems from adjustments in market expectations regarding the Section 232 refined copper tariffs, as the key mineral Section 232 investigation results announced on January 14 did not implement tariffs.

More notably, there is a change in the flow of copper. This week, LME warehouses in the U.S. saw the first copper inflow in nearly a year, as LME spot prices briefly traded at a premium. This is suppressing LME prices and inter-temporal spreads, and LME inventories in Asia are also beginning to accumulate.

Morgan Stanley believes that the likelihood of copper being exported from the U.S. is extremely low, but imports are expected to slow down. The decision on whether to impose tariffs on copper will be key to the outlook for the second half of 2026 and 2027. The biggest downside risk for copper prices is the complete exclusion of refined copper tariffs in the U.S., which would allow accumulated inventory to flow into a broader market.

According to bill of lading data, the current inventory in the U.S. is extremely high, mainly concentrated in the COMEX exchange. The implied accumulation of non-COMEX inventory indicates that a large amount of copper has flowed into the U.S. during the previous import boom

China's Demand Faces Seasonal Challenges

In December, China's apparent copper demand continued to show negative growth, while refined copper exports remained strong, and inventories rose seasonally. Additionally, the data vacuum period before the Spring Festival has increased market uncertainty. With the Lunar New Year approaching in mid-February, the market will only receive limited data on China's demand situation until mid-March. The Yangshan copper premium has fallen to -$22/ton, the lowest level since mid-2024.

Meanwhile, China's refined copper production remains strong. China's refined copper output is expected to grow by 10% in 2025, reaching a new high. Despite facing an extremely tight global copper concentrate market and negative processing fees (TC), China has added significant smelting and refining capacity. China successfully increased its copper concentrate imports by 8%, with Chile and Peru being the largest suppliers, and supply from Mongolia also increasing.

Scrap copper is also supporting the growth of refined copper. China's scrap copper imports are expected to grow by 4% in 2025, reaching a historical high in December, indicating that smelters may be using more scrap copper to boost refined copper output. Asia is the largest supply region for scrap copper to China, while flows of scrap copper from the United States have nearly approached zero. With domestic refined production strengthening and the proportion of imports in the supply mix declining, China has even begun exporting refined copper in recent months. If demand in the United States slows, the market may see more inventory accumulation.

Mine Supply Severely Limited

The tight supply situation will provide key support for copper prices. Morgan Stanley expects copper mine supply to grow by only 0.2% in 2026, as many mine supply disruptions from 2025 will extend into 2026. The Mantoverde mine under Capstone in Chile has halted production due to a strike (annual capacity of 106,000 tons), and Lundin Mining has also slightly lowered its guidance for 2026. This may limit the growth of refined copper supply (Morgan Stanley expects it to be 0.6%), and even considering more scrap copper usage, the overall market will remain tight.

However, there is some potential for recovery in the second half of 2026 and 2027. Freeport McMoRan has indicated that certain areas of its Grasberg mine are planned to be phased back into operation starting in the second quarter of 2026, and Ivanhoe's Kamoa Kakula project has some potential for recovery, while First Quantum's Cobre Panama mine may also restart.

According to Wood Mackenzie data, copper mine disruptions in 2025 could exceed 6% of supply, with cumulative disruptions exceeding 1.4 million tons. Historical data shows that the annual growth rate of copper mine supply fluctuated significantly from 2015 to 2024, while the growth rates for 2025 and 2026 are at historical lows.

Market Outlook

Morgan Stanley expects a deficit of about 600,000 tons in the copper market in 2026, as limited mine supply growth (expected at 0.2%) cannot match strong demand growth (expected at 1.8%), driven by new factors such as data centers and energy storage systems.

The macro backdrop continues to support metal prices. More interest rate cuts will support non-yielding assets and key end-use industries, and the institution's foreign exchange strategists also believe there is some room for the dollar to weaken. Concerns about supply security and new demand themes such as data centers are also driving demand for physical assets Copper holdings have steadily increased.

The institution had a positive outlook on metals, including copper, at the beginning of this year, but prices have exceeded its second-quarter forecast of USD 12,200 per ton. Analysts believe that supply tightness and a strong macro backdrop will provide good support for prices, but there may be fluctuations in the short term due to uncertainties in U.S. import trajectories