Interpretation of New Stocks in the US Market | Continuous losses combined with high debt, is Beisiman's "burden" making its prospects in the US unclear?

Beisman Precision Instruments Co., Ltd. is facing continuous losses and high debt, with an unclear prospect for going public. The company has updated its IPO filing eight times, postponing the timeline to 2025. Beisman was established in 2001 and primarily produces medical devices for domestic and international sales, covering multiple medical fields. Despite having a certain sales network in domestic and international markets, its path to going public remains challenging, urgently needing to resolve funding issues through an IPO

Continuous losses and the eighth update of the IPO listing documents have pushed the timeline into 2025, yet the path to listing for the medical device manufacturer Bestman Precision Instruments Co., Ltd. (BSME.US, hereinafter referred to as "Bestman") still seems far from sight.

According to Zhito Finance APP, Bestman Precision Instruments, as a domestic medical equipment manufacturer and retailer, has a history dating back to 2001, primarily producing medical devices for sale both domestically and internationally. It has been nearly three years since Bestman secretly submitted its application to the U.S. SEC on February 28, 2022. After several years, will there be any new changes for Bestman?

Difficulties in Losses, Urgently Needing to "Supplement Blood" through Listing

According to the prospectus, Bestman Precision Instruments operates in China through two entities, Shenzhen Bestman and Nanjing Yonglei. Among them, Shenzhen Bestman mainly produces medical devices and sells them domestically and internationally; Nanjing Yongle primarily exports medical devices, selling those produced by Shenzhen Bestman.

For over 20 years, Shenzhen Bestman has provided more than 567,000 Class I and Class II medical device products to hospitals, pharmacies, medical equipment companies, and individual customers. Its main products include ultrasound Doppler blood flow detectors, ultrasound Doppler fetal heart monitors, infusion and blood warming devices, fetal/maternal monitors, syringe destroyers, enteral nutrition pumps, insulin coolers, vein finders, breast self-examination devices, medical infrared thermometers, ultrasound beauty devices, and intelligent disinfection vehicles.

In addition to the domestic market, the company's products are exported to 98 countries and regions, including Europe, America, Oceania, Africa, the Middle East, and Southeast Asia, through cooperation with 1,646 export distributors, with the overseas market accounting for a significant portion of Bestman's revenue.

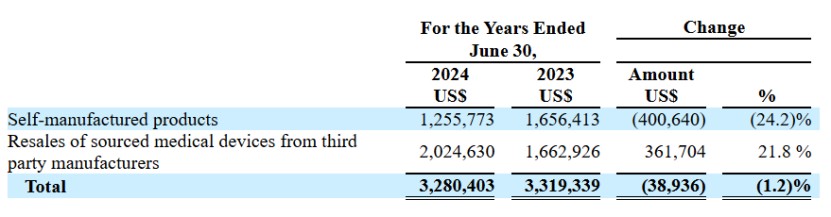

The prospectus shows that in the past fiscal years 2023 and 2024 (ending June 30 each year), Bestman's revenues were $3.3193 million and $3.2804 million, respectively, with corresponding net losses of $704,900 and $1,043,400. As revenue declined, net losses also expanded simultaneously. Among them, Bestman's domestic sales accounted for 40% and 27%, respectively, while international sales accounted for 60% and 73% of its total net income, indicating that "going overseas" does not seem to have brought a dividend effect for Bestman.

It is noteworthy that Bestman not only manufactures and sells medical devices under its own brand but also resells medical devices procured from other manufacturers, with sales of its own brand significantly lower than those of resold brands. Sales revenue from its own brand decreased by 24.2% in fiscal year 2024, while sales of resold procured medical devices increased by 21.8% compared to previous periods.

However, from a profitability perspective, Beisiman's gross margin rapidly declined from 46.0% in the fiscal year 2023 to 33.1% in the fiscal year 2024, mainly due to the increased resale volume of medical devices sourced from third-party manufacturers, which typically have lower profit margins, negatively impacting the company's overall gross margin; as well as a decrease in sales of ultrasound Doppler equipment, where reduced procurement demand from hospitals affected profit margins.

However, from a profitability perspective, Beisiman's gross margin rapidly declined from 46.0% in the fiscal year 2023 to 33.1% in the fiscal year 2024, mainly due to the increased resale volume of medical devices sourced from third-party manufacturers, which typically have lower profit margins, negatively impacting the company's overall gross margin; as well as a decrease in sales of ultrasound Doppler equipment, where reduced procurement demand from hospitals affected profit margins.

From the perspective of the three expenses, in the fiscal year 2024, the company's management expenses decreased from USD 1.2542 million to USD 1.1295 million compared to the same period last year, a year-on-year decrease of 9.9%. The decline in sales and marketing expenses was even more pronounced, dropping from USD 554,500 to USD 485,200, a decrease of 12.5%, while research and development expenses saw a slight increase of 2.6% year-on-year to USD 424,600.

Even though the intention of "cost reduction and efficiency improvement" is evident, it seems difficult to resolve the funding dilemma that Beisiman currently faces: as of June 30, 2024, the company's cash and cash equivalents were approximately USD 222,900, with net cash from operating activities at USD 864,700, which is insufficient to support the company's annual loss of one million dollars.

In addition, as of June 30, 2024, Beisiman's accounts receivable balance was USD 1.4948 million, compared to approximately USD 1.2302 million in the same period last year. Meanwhile, in the fiscal year 2024, the company's total assets were approximately USD 3.44 million, but its total current liabilities reached as high as USD 3.4438 million, and total liabilities soared to USD 8.462 million. In such a "liabilities exceeding assets" situation, it is not difficult to see that the company may face liquidity risks.

Intense Market Competition, Uncertain "Going Global" Prospects

Considering the industry's development potential and competitive landscape, it is clear that for Beisiman, there are both "opportunities and challenges."

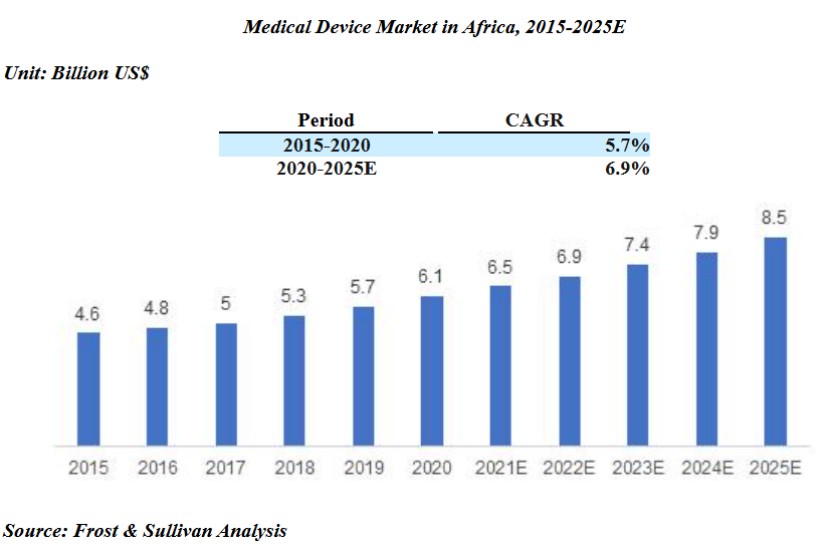

From a regional sales perspective, Beisiman has opened up overseas markets, primarily focusing on the African market. The medical device market in Africa still has considerable growth potential. Africa's medical devices heavily rely on imports, which account for about 90% of the entire medical device market. According to a Frost & Sullivan report, the African medical device market gradually grew from USD 4.6 billion in 2015 to USD 6.1 billion in 2020, with a compound annual growth rate of 5.7%. It is expected that by 2025, this market will reach USD 8.5 billion. With the increase in health spending in Africa and the expansion of national insurance programs, more African people may gain access to medical services.

In addition, there is an increasing demand for ultrasound equipment from hospitals and health examination centers at all levels in China. Meanwhile, favorable industry policies such as national medical reforms, the gradual transition of ultrasound diagnosis from ultrasound departments to clinical departments, and continuous technological innovations in product types are driving the rapid development of the domestic ultrasound equipment market and continuously expanding application boundaries, opening up new market spaces For Besman, the company has occupied a certain market share in the ultrasound vascular Doppler detector and infusion blood warming device markets. With the continuous growth of the Chinese and African markets, it is expected to drive the company's business further expansion in the future.

However, considering the competitive landscape of the industry and the company's competitive strength, it is evident that Besman also faces "challenges" in its ongoing development.

On one hand, the current medical device industry is highly competitive, with many medical device companies creating new companies with greater market influence through mergers. As the medical device industry consolidates, competition in providing goods and services to industry participants will become more intense. At the same time, as more and more medical device companies seek to outsource more product design, prototyping, and manufacturing, Besman will also face competitive pressure from new entrants and established companies with more resources.

On the other hand, in negotiations with downstream customers, Besman does not seem to have a significant advantage. In the prospectus, Besman mentioned that the company relies on a few major customers without long-term contracts. In the fiscal year 2024, the top three customers accounted for 24%, 17%, and 10%, respectively. Since the company has not signed long-term agreements with its customers, transactions are only recorded through short orders, and any loss or reduction in orders from major customers will adversely affect the company's performance.

In summary, from a fundamental perspective, how Besman can "turn losses into profits" is the primary issue it needs to address before going public. Additionally, its characteristics of being relatively small, highly leveraged, and having high receivables make it difficult to see a "turnaround" in business aside from seeking financing in the U.S. At the same time, compounded by significant competitive pressure and high customer concentration, Besman clearly has a long way to go to truly attract investors' interest