"International DiDi" Uber: Will the strong Q1 report be the last highlight?

On May 3, before the US stock market opened, the "international version of Didi" Uber released its first quarterly report for 2023, with the following key points:

1. The crisis has not yet come: Although the trend of the weakening of the US economy is becoming more and more obvious, the growth of both Uber's ride-hailing and food delivery order amounts in this quarter is quite strong, with the growth rate even accelerating compared to the previous quarter. Specifically:

The Ride-hailing (Mobility) sector achieved an order amount of $15 billion in the first quarter, slightly higher than the market's expected $14.7 billion, and the year-on-year growth rate increased from 31% to nearly 40%. The Delivery business achieved an order amount of $15 billion, and the growth rate increased from 6.5% to 8.1%, reversing the trend of slowing growth for 7 consecutive quarters.

It can be seen that from the perspective of expectation difference and the trend of growth acceleration, the company's performance growth is still quite strong. The signs of the US economic recession have not yet been reflected in the company's performance, and the resilience of the company's ride-hailing business is still significantly stronger than that of its food delivery business.

2. Increased monetization rate assists accelerated revenue growth: After excluding the impact of changes in business models in some regions, the comparable monetization rate of Uber's ride-hailing business in this quarter increased significantly from 19.7% in the previous quarter to 21.6%; the monetization rate of the delivery business also increased slightly by 0.5pct to 16.2% on a month-on-month basis.

Due to the magnifying effect of the monetization rate, the revenue of the ride-hailing business this quarter was $4.33 billion, higher than the expected $4 billion. After excluding the impact of model changes, it increased by 39% year-on-year and accelerated by 9 percentage points on a month-on-month basis. The revenue growth rate of the delivery business also increased slightly from 21% to 23%. The monetization rate and revenue growth of both businesses are improving, and the ride-hailing business is still stronger than the food delivery business.

3. Asia is the greatest contributor to strong growth: Although both the ride-hailing and delivery businesses have had strong growth, due to the weak revenue from the freight business, revenue declined by 23% year-on-year. Uber's total revenue this quarter was $8.82 billion, which is basically in line with market expectations.

Looking at different regions, the revenue growth rate in North America in this quarter was significantly slowed to 13%, indicating that the demand in the US is indeed weakening, while Asia and South America have shown better growth momentum. Among them, due to the lifting of epidemic prevention measures, the revenue growth in Asian countries has accelerated significantly to 41%, making it the fastest-growing market of all Uber markets and the actual hero behind the strong performance of the company this quarter.

4. Strong growth but bloated expenses, loss expands again?: Although both the ride-hailing and delivery businesses have had strong growth, and the monetization rate continues to increase, the gross margin has also improved, achieving a gross profit of $3.56 billion, higher than the expected $3.45 billion.

However, the cost side has not been able to continue its previous trend of continuous shrinkage, but has expanded somewhat. Among them, the expansion of management expenses is the most obvious, and the expense ratio (as a proportion of gross profit) has increased by 3 percentage points on a month-on-month basis to 26%, and the sales expense ratio has also increased from 34% to 35%. Therefore, operating losses have expanded from $140 million to $260 million on a month-on-month basis. However, if the adjusted EBITDA profit disclosed by the company this season reached 760 million yuan, an increase from the previous quarter's 660 million yuan.

5. Will revenue and profit continue to be strong in Q2?: For Q2 performance, the company predicts that the total order amount will reach 33.5 billion yuan, setting a new historical high, slightly higher than the expected 33.3 billion yuan. The guidance for adjusted EBITDA reached 830 million yuan, far higher than the market's expected 760 million yuan. The company's guidance shows a considerable improvement in profits for next quarter.

Long Bridge Dolphin Viewpoint: However, from the performance of this quarter's financial report, the growth of the core ride-hailing and food delivery businesses has been more robust than previously expected by Dolphin, with growth rates not only not continuing to decline, but also accelerating across all revenue indicators.

With the steady increase in monetization rate, the level of gross profit margin has also improved quarter by quarter. Apart from the expansion of expenses in this quarter, resulting in a widened GAAP-caliber operating loss, the overall impression of this financial report is quite positive.

Meanwhile, the company's guidance for the second quarter is also very optimistic, continuing the trend of resilient growth in revenue and continuous improvement in profitability. With current and expected good performance, the market's interpretation of this financial report is also very positive, with the company's stock price rising by as much as 10%.

However, Dolphin needs to remind investors that the current valuation of the company is within the optimistic interval previously estimated by Dolphin. At the same time, although Dolphin cannot determine whether the company's future business will continue to exceed expectations, overseas, especially Asia, may continue to support the company's growth.

However, although the US economy was still relatively robust in the first quarter, the expectation of a recession is becoming increasingly apparent. When the company's business sentiment is still high and its valuation is optimistic, investors should still be aware of the possible black swan risk caused by a recession in the US economy in the future.

Long Bridge Dolphin Research focuses on cross-market interpretation of global core assets and grasping the deep value and investment opportunities of enterprises. Interested users can add the WeChat account "dolphinR123" to join the Dolphin Research Society and explore global asset investment perspectives together!

1. Ride-hailing & food delivery growth remains resilient, with a recession on the horizon?

First and foremost, Uber's first core business, the Mobility sector, realized an order amount of US$14.99 billion in Q1, slightly higher than the market's expected US$14.7 billion.

In terms of seasonality, over the past two years, Q1 order amounts have been lower than those in Q4 of the previous year, but this time there was a QoQ increase. The YoY growth rate was also 31% due to the low base, achieving almost 40% growth speed. From the financial data point of view, there was no sign of a decline in travel demand in at least Q1, and it can even be said to be thriving.

Similar to the ride-hailing sector, Uber's delivery business has also achieved strong growth and there are currently no signs of weakness. This quarter, it achieved a new high in delivery order amount at 15 billion yuan, slightly higher than market expectations. In terms of growth trends, the year-on-year growth rate has also increased to 8.1%, putting an end to the trend of declining growth rates in the previous 7 quarters.

Similar to the ride-hailing sector, Uber's delivery business has also achieved strong growth and there are currently no signs of weakness. This quarter, it achieved a new high in delivery order amount at 15 billion yuan, slightly higher than market expectations. In terms of growth trends, the year-on-year growth rate has also increased to 8.1%, putting an end to the trend of declining growth rates in the previous 7 quarters.

Adding up the delivery and ride-hailing businesses, the core order amount exceeded 30 billion US dollars this quarter. Due to the strong growth of both the ride-hailing and delivery sectors, the year-on-year growth rate of the core order amount rebounded from 18% to 22%.

Looking at the breakdown of price and quantity driving factors, last quarter's average order value of the core orders (including ride-hailing and delivery) was $14.1, although it decreased by 1.7% year-on-year due to a high base, it remains at a relatively high level and has not yet reflected any signs of decreasing demand.

However, considering that energy prices are returning to normal levels and the 2022 ASP base is also high, the average order value for the following quarters this year may continue to decline year-on-year, dragging down performance growth.

Although the average order value has shrunk year-on-year and dragged down growth, the good news is that there is strong growth in the core order quantity, with a growth rate rebounding to 24%. Although there are factors such as a low base from the same period last year, the unexpected strength in volume is the main reason for the total order amount to accelerate growth again this quarter.

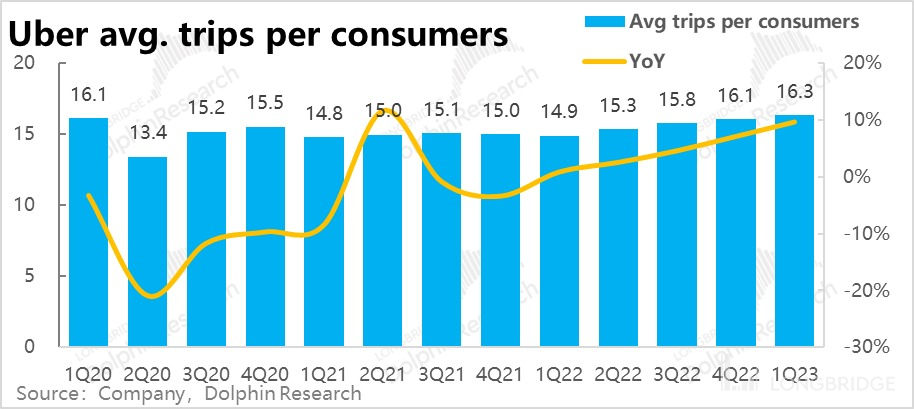

Looking at user numbers and order frequency, this quarter, Uber's platform has 130 million monthly active users, a decrease of 1 million from the previous quarter. Considering that Q4 is the peak season for tourism, the slight decrease in monthly activity from the previous quarter is understandable.

The average number of orders per person this quarter was 16.3 times, with the order frequency steadily increasing year-on-year by nearly 10%. Although the user base has slightly decreased, the continuously increasing order frequency of users has helped the company's core order volume to steadily increase.

{kind=link}

2. Monetization rate continues to increase, revenue growth accelerates

As Uber transformed from a platform-type to a self-employed model in regions such as the UK and Canada, part of the company's confirmed revenue changed from net commission to total payment amount, which led to revenue growth. Therefore, Dolphin mainly focuses on the performance after excluding the impact of accounting changes.

Specifically, the revenue of taxi business in this quarter was USD 4.33 billion, significantly higher than the market expectation of USD 4 billion. After excluding the impact of business model changes, the "true" revenue was about USD 3.2 billion, an increase of 39% year-on-year, and an acceleration of 9% compared to the previous quarter.

After excluding the impact of business model changes, the comparable monetization rate of the taxi business also significantly increased from 19.7% in the previous quarter to 21.6%. Dolphin believes that there is still room for improvement compared to the historical high point of monetization rate, which is naturally a positive for the company's business in the short to medium term. However, from the perspective of platform economy, excessive monetization will inevitably affect the activity of drivers and users and cannot be sustained in the long term.

Similar to the taxi business, the monetization rate of the delivery business also increased, but the magnitude was relatively small. Specifically, the real monetization rate of the delivery business this quarter was 16.2%, a slight increase of 0.5% compared to the previous quarter.

As the order volume of the delivery business this quarter increased by about 1.6% compared to the previous quarter, and the speed of monetization rate increase was limited, the final growth rate of the delivery business revenue this quarter also increased slightly from 21% to 23%, achieving a revenue of USD 3.09 billion. It can be seen that the demand growth of taxi business is significantly higher than that of the delivery business.

3. Asia is the foundation for revenue growth

In addition to the taxi and delivery businesses, Uber's freight business achieved a revenue of CNY 1.4 billion this quarter, a year-on-year decrease of 23%. As international trade, which was quite prosperous during the epidemic, started to weaken, demand for freight also began to decline. Meanwhile, Dolphin has always believed that the coordination effect between the B-to-B freight business and the core C-to-C business of the company is relatively low, and the profit margin of freight forwarder business is also thin, so it is not optimistic about the future of Uber Freight. Recently, the company has also claimed to have plans to divest from its freight business or go public separately. Dolphin agrees with this choice, as it can help the company focus more on its core business and reduce losses caused by the freight business.

After summing up all businesses, Uber's total revenue this quarter was $8.82 billion. Although taxi business exceeded expectations, total revenue was basically in line with market expectations due to the drag of the freight business.

Looking at revenues by region, North America contributed nearly 60% of the company's revenue and is still the company's main market. In addition, the market sizes of Europe and the Middle East (EMEA) are also growing rapidly, accounting for more than 24% of the total.

In terms of year-over-year growth rate (due to the effect of changes in business models and acquisitions, the absolute value of growth rate is overly amplified, so the trend of growth rate changes is mainly observed), the previously leading North American revenue growth rate slowed significantly to 13%, indicating that demand in the United States is relatively weak and overseas has contributed greatly to the company's overall performance. Although the absolute growth rate in the European region is high due to the impact of the change to self-employment in the UK, the trend is also slowing down.

The growth momentum in Asia and South America is better. Among them, as predicted by Dolphin, as the epidemic prevention measures in Asian countries were lifted, Uber's revenue growth in Asia accelerated to 41%, which is the fastest growing market for Uber and also a contributor to the company's overall steady growth.

4. Expenses have also inflated, and increased revenue did not lead to increased profits?

Due to the continued increase in realization rate of the company's taxi and delivery businesses, the gross profit margin has also been steadily increasing, achieving a gross profit of $3.56 billion, higher than the market expected $3.45 billion.

In terms of a more stable and comparable angle of gross profit/total order amount, we observe the gross profit margin changes. Gross profit margin (as a proportion of the order amount) reached 11.3%, an increase of 0.5pct from the previous quarter.

However, in terms of expenses, it can be seen that while the company's revenue growth exceeded expectations, its expenses are also expanding. Among them, the management and marketing expenses have expanded significantly compared to the previous period.

However, in terms of expenses, it can be seen that while the company's revenue growth exceeded expectations, its expenses are also expanding. Among them, the management and marketing expenses have expanded significantly compared to the previous period.

Therefore, although the company's revenue growth and gross profit growth for this quarter are quite strong and slightly exceed market expectations, the expenses did not continue the previous trend of continuous contraction, instead expanding. Therefore, the overall operating loss of the company this quarter has expanded to 260 million.

At the same time, this quarter's equity incentive and other adjusted expenses are similar to the previous quarter, and the adjusted operating profit is 310 million, which is a decrease from the previous quarter's 440 million.

Fifth, the profitability of the takeaway business exceeded expectations and improved.

Since the company has not disclosed the operating profit of each sector, only EBITDA caliber is available. Specifically, the company's overall adj. EBITDA reached 760 million U.S. dollars, exceeding the market expectation of 680 million. Looking at each business unit, the main source of exceeding expectations is still the takeaway business:

-

The adj.EBITDA of the ride-hailing business is 1.06 billion U.S. dollars, slightly higher than the market expectation of 1.01 billion.

-

The takeaway business achieved an adj.EBITDA of 290 million, which is significantly higher than the market expectation of 257 million, and the adj EBITDA profit margin is 8.2%, far higher than the market expectation of 6.6%.

-

As for the Freight business, due to a significant year-on-year decline in revenue this quarter, its adj.EBITDA loss was 23 million, and the loss has expanded compared to the previous quarter.

Completion Dolphin Research [Uber] Study:

February 9, 2023 telephone conference "Can Uber continue to grow while reducing expenses" On February 8, 2023, comments on the financial report: "Didi in the United States: Small and Beautiful, "Completely Defeated" by the Strong and Large?"

On November 2, 2022, telephone conference: "Uber believes that travel demand is still strong, and the future focus is on improving user stickiness and habits (3Q22 telephone conference summary)"

On November 2, 2022, comments on the financial report: "Uber, which can make money without growth, is also favored by the market?"

On November 21, 2022: "After experiencing the "hard and happy" of the epidemic, where is Uber's future?"

On October 14, 2022: "Crossing the epidemic and inflation, the killer behind Uber's luck"

Risk disclosure and statement of this article: [Dolphin Investment Research Disclaimer and General Disclosure] (https://support.longbridge.global/topics/misc/dolphin-disclaimer)

The copyright of this article belongs to the original author/organization.

The views expressed herein are solely those of the author and do not reflect the stance of the platform. The content is intended for investment reference purposes only and shall not be considered as investment advice. Please contact us if you have any questions or suggestions regarding the content services provided by the platform.