US stocks closed for the day, European stocks surged and then fell back, Novo Nordisk reached a new all-time high, and Brent crude oil hit a nine-month high again.

European stock indices were generally flat, with overall declines in stock indices across Europe. Weight loss drug Wegovy continued to rise, with a temporary increase of over 2%, maintaining its position as the highest-valued company in Europe, surpassing LVMH. The US dollar index saw two consecutive gains before halting. Offshore renminbi broke through 7.26 during intraday trading, rising by over 100 points before reversing its gains. Brent crude oil experienced its fifth consecutive increase, while European natural gas fell by nearly 6%. London copper fell from its four-week high, while London aluminum saw its fourth consecutive gain and London tin reached a three-week high with two consecutive increases. Gold experienced a decline during intraday trading.

This Monday was Labor Day in the United States, and the US stock and bond markets were closed for the day. European stocks traded lightly, with media reports indicating that trading volume in European stocks on Monday was nearly one-third lower than the thirty-day average.

China's stable real estate policies, such as recognizing houses but not loans, boosted market risk appetite. The US dollar fell, and the pan-European stock index rose in early trading on Monday, but the gains gradually faded and were gradually given up. The European Stoxx 600 index rose more than 0.8% in early trading, reaching a new intraday high in nearly four weeks, but fell in the final trading session, closing slightly lower. After a roughly 1.5% increase last week, the largest weekly gain since January 14, the upward trend could not be sustained.

Major European stock indexes continued to decline on Monday, with the French and Spanish stock markets falling for four consecutive days and the German stock market falling for three consecutive days. The British stock market, which rose alone on Friday, fell back, while the Italian stock market, which fell for two consecutive days, fell slightly and almost closed flat.

In individual stocks, after the British market officially injected its popular weight-loss drug Wegovy, Danish pharmaceutical company Novo Nordisk rose more than 2% in early trading and closed up more than 0.7%, reaching a new intraday and closing high. After surpassing LVMH in market value last Friday, it ranked first in market value among European listed companies for the second consecutive trading day. However, luxury goods giant LVMH, which fell 0.4%, partially limited the rise of European stocks.

Among the sectors of the Stoxx 600, 8 closed higher on Monday, with basic resources in the mining sector leading the gains, rising nearly 0.6% and rising nearly 2% at one point, benefiting from China's support for the real estate market policy pushing up iron ore prices. Tourism rose more than 0.5%, technology rose nearly 0.5%, and healthcare, where Novo Nordisk is located, rose slightly. Among the 11 sectors that closed lower, utilities and food, which fell against the market last Friday, fell nearly 0.8% and 0.5% respectively, insurance fell nearly 0.6%, and personal and household goods, where LVMH is located, fell slightly.

European bond prices continued to decline overall, and European bond yields continued to rise following the rise in US bond yields last Friday. At the end of the bond market on Monday, the yield on 10-year benchmark UK government bonds closed at 4.46%, up 3 basis points during the day; the yield on 2-year UK bonds closed at 5.17%, up 3 basis points during the day; the yield on 10-year benchmark German government bonds closed at 2.57%, up 3 basis points during the day; the yield on 2-year German bonds closed at 3.01%, up 3 basis points during the day.

Currently, market pricing shows that investors expect a 30% probability of a 25 basis point rate hike by the European Central Bank in September, and the probability of further rate hikes before the end of this year is almost evenly split. Commentators say that this is the first time in over a year that traders have found it difficult to judge whether the ECB will raise interest rates. However, current expectations may be influenced by public comments from ECB officials before the ECB meeting next week. The US Dollar Index (DXY), which tracks the exchange rates of the US dollar against six major currencies including the euro, reached a daily high of nearly 104.30 in the early Asian market on Monday. However, it turned downward during the Asian morning session and fell below 104.03 in the European stock market, marking a decrease of 0.2% for the day. It failed to approach the intraday high since June 1 that was surpassed on August 25 when it rose above 104.40.

By the time the US stock market closed, the US Dollar Index was above 104.10, experiencing a decrease of over 0.1% for the day. The Bloomberg Dollar Spot Index, which tracks the US dollar against ten other currencies, also slightly declined but remained close to the high point since May 31. Both indices halted their two-day consecutive gains.

During the Asian market session, the offshore Chinese yuan (CNH) against the US dollar reached a daily high of 7.2548, rising by 155 points for the day. However, it fell to a daily low of 7.2789 during the European stock market session and the usual US stock market midday session, marking a decrease of 86 points for the day. This was a departure from the intraday high since August 11 that was surpassed last Friday when it rose above 7.24. At 4:59 am Beijing time on September 5, the offshore Chinese yuan against the US dollar was reported at 7.2755 yuan, a decrease of 52 points from the New York closing price last Friday, ending the two-day consecutive upward trend.

Among other non-US currencies, the US dollar against the Japanese yen experienced a similar intraday decline as last Friday. It quickly rose above 146.40 after the European stock market opened and surpassed 146.50 during the usual US stock market midday session, rising by approximately 0.2% for the day. This marked a departure from the low point since August 11 when it fell below 144.50. The euro against the US dollar fell below 1.0780 in the early Asian market, returning to the low point since August 25 that was reached last Friday. However, it rebounded after fluctuating and rose above 1.0800 in the early European stock market session. It even approached 1.0810, setting a daily high. The British pound against the US dollar also experienced an intraday rise. It fell below 1.2590 in the early Asian market but rose above 1.2640 during the European stock market session, marking an increase of over 0.4% for the day. However, it still has a distance to go to reach the high point since August 23 when it rose above 1.2740.

Bitcoin (BTC) briefly rose above $26,100 in the early Asian market but then continued to decline. It fell below $26,000 during the early Asian market session and even dropped below $25,800, setting a daily low during the final moments of the US stock market morning session. By the time the US stock market closed, it was above $25,800, experiencing a decrease of less than 1% in the past 24 hours. It has not yet approached the low point since August 17 when it fell below $25,400.

Brent crude oil has risen for five consecutive days and reached a new nine-month high for two consecutive days. Meanwhile, European natural gas has fallen by nearly 6%. Last Friday, the Russian Deputy Prime Minister stated that Russia and the OPEC+ agreement on production cuts have reached an agreement on the parameters for further reducing exports in October. The market expects that OPEC+ will continue to cut production, and Saudi Arabia will extend its voluntary production cut of 1 million barrels per day until October. International crude oil futures, which rose sharply last week, continued to rise overall on Monday, but experienced several intraday declines.

When European stocks hit a new daily low before the market opened, US WTI crude oil fell to $85.27, and Brent crude oil fell to $88.26, both down more than 0.3% intraday. European stocks experienced several short-term declines during the trading session, but completely reversed the downward trend during the midday session. After the European stock market closed, US oil rose above $86 to $86.14, up nearly 0.7% intraday, and Brent oil rose to $89.22, up nearly 0.8% intraday.

In the end, Brent November crude oil futures closed up $0.45, or 0.51%, at $89.00 per barrel, reaching a new high since November 17 last year, and closing higher for five consecutive trading days. It rose nearly 5.5% last week, marking the largest weekly gain since April 6.

The US market was closed on Monday, and there was no closing price for US oil. If the upward trend continues on Tuesday, US oil is expected to close higher for the eighth consecutive trading day and reach a new closing high since November last year for two consecutive trading days. As of last Friday, US oil had risen for seven consecutive days, with a cumulative increase of more than 8%, and a weekly increase of nearly 7.2% last week, the largest weekly gain since March 31.

European natural gas prices fell back after rebounding last Friday. UK natural gas futures fell by 6.35% to 81.25 pence/therm, reaching a closing low since August 1; TTF benchmark Dutch natural gas futures on the European continent fell by 5.74% to 33.571 euros/MWh, reaching a low since August 24.

As local demand in Europe declines, recent data from Gas Infrastructure Europe shows that European natural gas inventories have reached 93.1% of storage capacity. It is commented that the inventory level suppresses short-term gas prices, and the deviation between spot and futures gas prices implies potential tension and uncertainty in the market. The maintenance of Norwegian gas fields and possible disruptions to Australian liquefied natural gas (LNG) exports due to strikes have further complicated the supply chain situation.

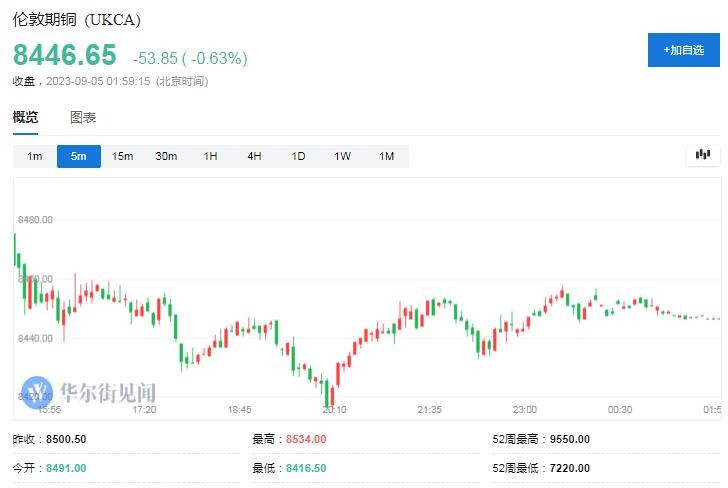

London base metal futures mostly closed lower on Monday, failing to continue the upward trend seen last Friday. London copper, nickel, and zinc, which rebounded last Friday, all fell back. London copper fell from a four-week high, while nickel and zinc bid farewell to their near four-week highs. London aluminum, which rose for four consecutive days, and London lead, which rose for two consecutive days, both retreated from their respective highs since August 1 and more than seven months ago. However, London tin rose for two consecutive days and closed above $26,300 for the first time in three weeks.

The New York gold futures hit a daily high of $1972.6 before the European stock market opened on Monday, rising nearly 0.3% intraday. However, it then retreated and European stocks turned negative in early trading. During midday trading, European stocks hit a daily low of $1962.6, with a decline of over 0.2% intraday. If the downward trend continues on Tuesday, the COMEX December gold futures, which did not have a closing price on Monday, will give back the small rebound from last Friday and fail to break the high near $1970 reached on August 4th.