Renowned Analyst at Bank of America: Unprecedented Market Performance in US History!

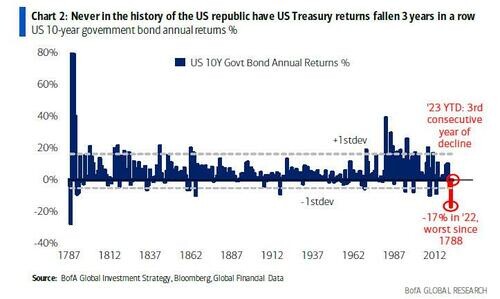

Renowned strategy analyst Michael Hartnett of Bank of America pointed out that the 10-year US Treasury bond is likely to experience an annual decline for the third consecutive year, which has never happened in US history. Inflation is bound to be stickier than the expectations of the Federal Reserve. The Fed has already completed this round of interest rate hikes and should sell stocks. Compared to the 2010s, the returns on stocks and bonds in the 2020s will be lower.

In his latest report, renowned strategy analyst Michael Hartnett points out that the US 10-year Treasury yield is likely to record an annual decline for the third consecutive year, with a 3.9% drop in 2021, a 17% drop in 2022, and a continued decline in 2023, which has never happened in US history.

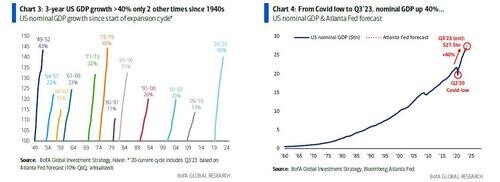

The unusually weak performance of the US bond market is related to the unexpectedly strong performance of the country's economy. Since the low point in the second quarter of 2020 during the COVID-19 pandemic, the US nominal GDP (which includes economic growth and inflation) has grown by an astonishing 40%. This nominal GDP growth rate ranks third in US history, with the top two being 44% from 1975 to 1979 and 43% from 1949 to 1952.

Corresponding to the economic growth is the performance of the US stock market. The S&P 500 index rose by 136% from 1949 to 1952, by 97% from 1975 to 1978, and has risen by 113% since the low point in March 2020.

However, unlike the previous two market reactions, value stocks outperformed growth stocks by 45 and 105 percentage points, respectively. In the past three years, this trend has completely reversed, with a negative difference of 27 percentage points. The breadth of the global market has fallen to a 20-year low, as only a few stocks are leading the entire market higher.

Hartnett also points out that commodities have risen by 11% in the third quarter to date, becoming the best-performing asset class of the season. There are signs of a comeback in high inflation during 2021-2022, reminiscent of the ghost of Arthur Burns. (Note: Burns served as Chairman of the Federal Reserve during the high inflation period in the United States from 1970 to 1978)

Hartnett believes that inflation is inevitably stickier than the Federal Reserve's expectations, and this is related to wages, especially the growing influence of labor unions. After truck drivers recently reached an agreement with UPS, wages for both part-time and full-time workers have increased significantly. Strikes are occurring in large numbers, and unions are actively negotiating double-digit wage increases. Currently, 44% of Americans support labor unions, the highest level since 1972. Policies such as excessive fiscal spending, redistribution, and protectionism have helped the share of labor in GDP rebound from its long-term low in the 2010s. However, as artificial intelligence is about to replace hundreds of millions of jobs, this could be a very costly victory. Hartnett's conclusion is that if robots replace humans on a large scale, artificial intelligence will mean universal basic income (UBI).

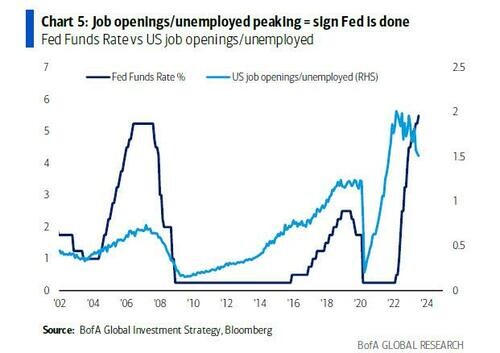

Hartnett also analyzed the U.S. job market, noting signs of disintegration after two years of strong growth. For example, the ratio of job vacancies to unemployment has dropped to its lowest level since September 2021. Although the U.S. non-farm payroll report for August was still decent, it is expected that in September and October, sectors such as high-yield bonds and home builders will signal a "hard landing" rather than the previous "soft landing," indicating that the Federal Reserve has completed this round of interest rate hikes.

Hartnett has long believed that stocks should be sold during the Federal Reserve's final interest rate hike. Based on the experience of the 1970s and 1980s, Hartnett has repeatedly pointed out that during those two decades, U.S. stocks fell within three months after the end of each interest rate hike cycle.

Hartnett predicts that the macro data and asset returns in the 2010s and 2020s will differ significantly. He expects that compared to the 2010s, the overall situation in the 2020s will see lower returns on stocks and bonds, taking into account political, geopolitical, social, and economic trends.

It should be noted that Hartnett's predictions for the U.S. stock market last year were quite accurate, earning him the title of "Wall Street's most accurate analyst." However, his judgment this year has not been accurate. He remains pessimistic about the stock market this year, but in fact, the U.S. stock market experienced a significant rebound in the first half of the year. Nevertheless, Hartnett's views continue to be highly regarded by the market.